Price movements along the supply & demand balance

A big change in the U.S. propane supply demand balance between 2018 and 2019 has driven prices sharply lower. On Friday August 2, 2019, MB LST propane traded at 44.625 cents per gallon. On August 2, 2018, the price was 94.250 cents per gallon. That is a 49.625 cent, or 53 percent, per gallon decline in just 12 months. West Texas Intermediate crude was down $13.30 per barrel, or 19 percent, over that time. We could reasonably attribute 19 percent of propane’s 53 percent decline in value over the last 12 months to weaker crude, but at least the remaining 34 percent of decline must be attributed to weaker fundamentals for propane itself.

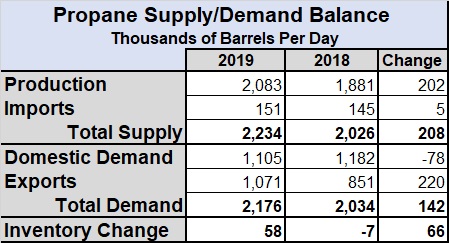

The supply and demand balance sheet below shows the change in fundamentals for propane that has led to the largest portion of its lower value.

From January 1 through August 2 of this year, U.S. propane inventory increased 58,000 barrels per day (BPD) or 12.650 million barrels compared to falling over 7,000 bpd, 1.596 million barrels over the same timeframe in 2018.

Supply has simply outpaced demand, resulting in the inventory gain. U.S. propane production surged 202,000 bpd year-over-year and imports gained 5,000 bpd yielding a net supply gain of 208,000 bpd.

Meanwhile, domestic demand is down 78,000 bpd, exports are up 220,000 bpd yielding a net gain of 142,000 in total demand. The difference in inventory build is 66,000 bpd.

The question is if there are prospects for fundamentals to change such that the price pendulum swings upward.

Let’s take it a line item at a time:

Production: Propane production is likely to continue to grow as the Energy Information Administration (EIA) projects continued growth in natural gas production, which is the key driver in propane supply growth. However, growth rate in natural gas supply is likely too slow. Natural gas production increased from 82.07 billion cubic feet per day in 2018 to an expected 91.03 billion cubic feet per day this year. The projection is natural gas production will rise to 92.5 billion cubic feet per in 2020, a significantly lower rate of growth.

Imports: Canadian producers are trying to find better netbacks than they are getting from the U.S. by exploring other countries to sell their propane. Starting in 2017, Canadians began moving propane directly to Mexico and those volumes continue to grow. In May, a new waterborne export facility opened will provide a passageway for propane to move directly from western Canada to Asia. It is yet to be determined if this facility will result in lower exports to the U.S., but it certainly opens the possibility. The new facility could export 15 million barrels annually, which is equal to 27 percent of Canada’s propane exports last year.

Domestic demand: Domestic demand has been laggard this year. Petrochemicals favor ethane as a feedstock because of its low price. However, propane and butane valuations reached a point of encouragement for more consumption by petrochemicals. Petrochemicals were consuming 252,000 bpd in March but are on pace to consume 349,000 bpd in July of this year. On the retail side, winter demand is always difficult to predict. Most don’t have a positive outlook for crop drying demand this fall. Most crops have to be dried because of late planting, but the overall yield is not looking good.

Exports: Exports actually grew enough year-over-year to keep up with production growth, but exports facilities appear to have reached their real capacity as we have seen little increase in recent exports. Enterprise will add more export capacity by the end of this quarter. The capacity will be 175,000 bpd, which will be split between butane and propane. Targa will also complete part of an export capacity expansion this quarter. The entire project would add more than 100,000 bpd of export capacity. How much will be available when phase one is complete is not completely known to us, but we think the second phase is mostly aimed at butane, so propane capacity could increase near 100,000 bpd in this first phase.

Even by the most conservative estimate on new capacity, it is easy to see there will be enough to offset the 66,000 bpd in inventory build difference between 2018 and 2019 which so dramatically changed the pricing environment. More practically there should be enough capacity, along with slower growth in supply, to see more balanced supply and demand at the least in late 2019-20. The potential for inventory reduction after the export expansions are complete this quarter is legitimate.

You May Also Like

Inventory build resets market

Apr 22, 2024

Develop your leadership skills

Apr 18, 2024

Q&A with Liquid Gas Europe’s general manager

Apr 16, 2024

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.