Crude production declines; prices surge

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, continues his analysis of the U.S.-Iran war’s impacts on crude, focusing on crude production.

Catch up on last week’s Trader’s Corner here: US crude position in the second month of the US-Iran war

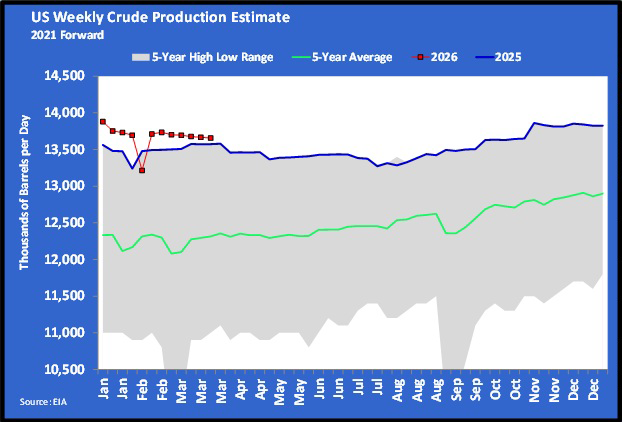

U.S. crude production has been declining recently despite high prices. Capital outlays for drilling are long-term decisions, so the decline is reflecting the relatively low price for crude before the U.S.-Iran war.

Crude production is now only slightly above this time last year. U.S. producers are employing 414 drilling rigs to drill crude wells. That is 72 fewer than this time last year. There is an inventory of 5,000 drilled but uncompleted wells that can be completed to add production rather quickly, even without additional drilling. The number of drilled but uncompleted wells has been decreasing, meaning the completion rate is increasing relative to the drilling rate.

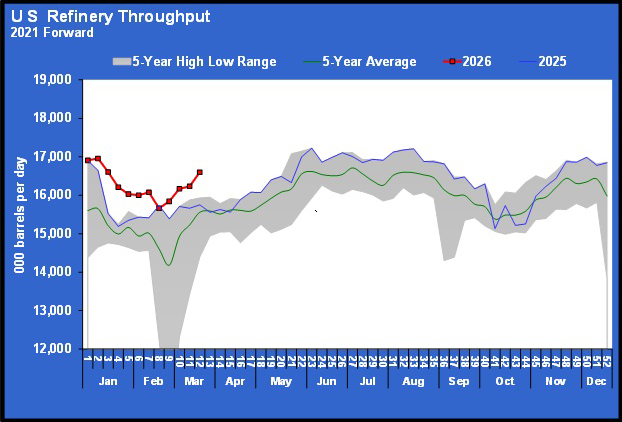

U.S. refinery throughput has been running high, which makes the increase in U.S. commercial crude inventories even more remarkable.

Two weeks ago, nearly 93 percent of U.S. refinery capacity was being used. That is high and may not be sustainable long term. Recently, there have been accidents at refineries in the United States. That could increase as throughput remains high and maintenance is delayed.

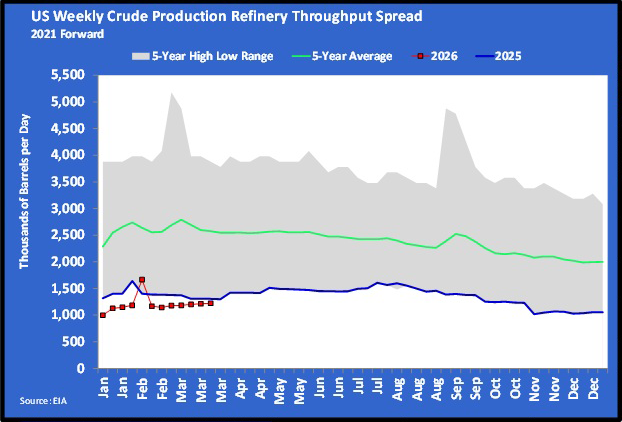

We put Chart 3 together for this analysis, which shows the difference between U.S. domestic crude production and refinery throughput. The difference is how much crude the United States needs from foreign sources. This figure is important given the global disruption to crude supplies.

Fortunately, the United States has been lowering the imbalance between refinery throughput and domestic production, making it less dependent on foreign sources. U.S. domestic supply is only about 1 to 1.5 million barrels per day (bpd) below what it needs for its refineries.

However, most U.S. production is now light sweet crude. We need more heavy sour crude than we produce, so our net crude import rate is higher than the number above.

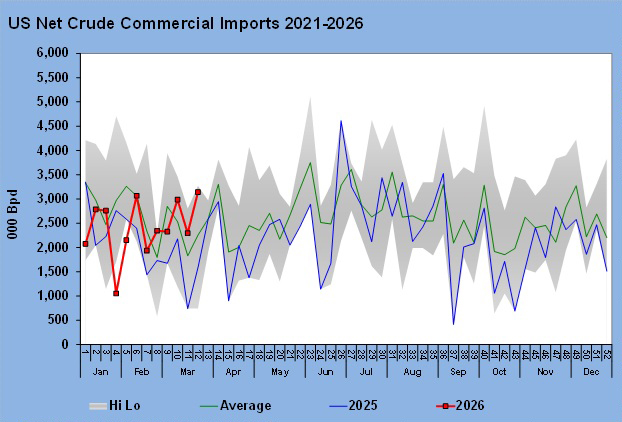

It varies widely each week, but the U.S. net import rate has averaged 2.411 million bpd this year. Imports were about 6.509 million bpd compared to exports of 4.099 million bpd at this point in 2026. The United States is selling its excess of light sweet crude and buying heavy sour crude in addition to importing the million or so bpd it is short of domestic production.

The good news is that Canada and Venezuela are the key suppliers of heavy sour crude to the United States, making the supply relatively stable. There are estimates that only about 2 percent of U.S. crude supplies are sourced from the Middle East.

That makes the recent developments in Venezuela and the increased crude trade between it and the United States very important. In fact, it could safely be implied that those developments made the decision to deal with the situation in Iran much easier for the U.S. administration. We think those developments made the 2 percent of supply from the Middle East unnecessary.

The development of alternative energy sources is important in the long term. Every nation on the planet needs to do what it can to reduce its dependence on fossil fuels. They are finite, and we consume over 100 million bpd of them. Whether one believes that burning fossil fuels contributes to higher global temperatures or not, finding replacements for fossil fuels is essential.

For our money, we believe that thermal energy will ultimately be what replaces hydrocarbon energy. Largely, the same technology we have perfected for producing hydrocarbon energy can be used to harness thermal energy. Wind energy appears to have a lot of environmental negatives, and solar energy has costly storage issues. Nonetheless, it is likely to be an all-of-the-above approach to making inroads into our hydrocarbon dependency.

But whatever the future holds for energy, a nation cannot go there before it is ready. In other words, you cannot dismiss hydrocarbon production before you have its replacement in hand. A nation can stop producing it and import it if it makes it feel better. But if a nation does that without actually eliminating the need for hydrocarbon energy, it makes the world less safe. There are always players on the global stage that will inevitably use a nation’s dependency against it. That can force a dependent nation to make morally bad decisions.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Geopolitics send crude and propane prices higher

Jul 13, 2026 -

Crude still not out of the woods

Jun 29, 2026 -

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.