How the US-Iran war draws on propane inventory

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, shares how ongoing supply disruptions tied to the U.S.-Iran conflict are tightening inventories and reshaping global pricing dynamics.

Catch up on last week’s Trader’s Corner here: US propane production reaches over 3 million bpd

In today’s Trader’s Corner, we are going to look at the state of U.S. crude with the draws on inventory related to the war between the U.S. and Iran. Before we go there, it is worth a short follow-up to our article of last week. The foundation of that article was the record-high propane export rate of 2.625 million barrels per day (bpd). A rate that was 290,000 bpd higher than the previous record. One that we hoped was not sustainable.

We pointed out the weekly volatility in propane export and domestic demand rates and suggested we need to be focused on the four-week averages for both, and the total demand rate rather than exports or domestic demand specifically.

This past week was another case in point with U.S. exports tumbling 976,000 barrels from that record high, but U.S. demand surging 608,000 bpd. Neither likely occurred. The bottom line was that total demand was down 368,000 bpd, allowing the 55,000 bpd call on inventories for the week ending May 22 to flip to a 304,000 bpd build in inventories for the week ending May 29.

Now on to the state of U.S. crude.

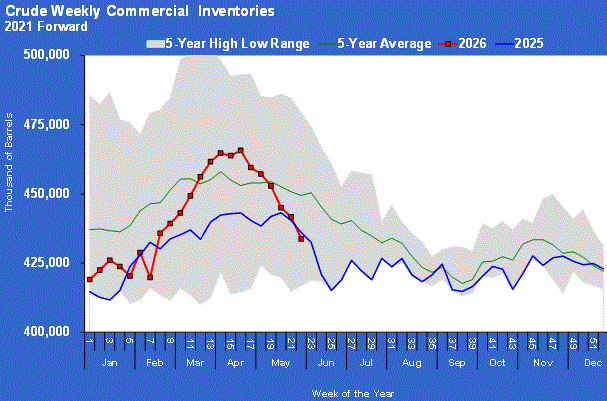

This past week the Energy Information Administration reported another draw on U.S. crude inventory, which has been the consistent pattern.

The 7.974-million-barrel draw took inventory below last year, eliminating the last vestige of the year-over-year surplus. Both years were well below the five-year average.

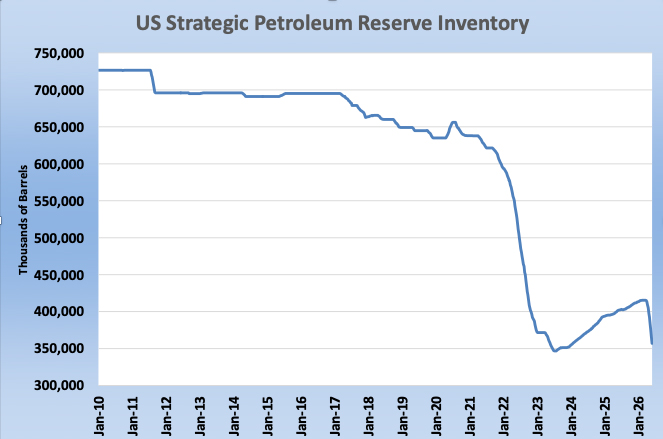

Crude held in the Strategic Petroleum Reserve (SPR) has been dropping rapidly as well. The level tumbled during the Biden administration as inventories were used to try and hold energy cost down following the start of the Russia-Ukraine war. They had begun to recover the last couple of years as the Trump administration tried to rebuild them.

But, with the start of the U.S.-Iran war disrupting about 20 percent of global crude supply, the U.S. agreed to participate in a coordinated release of strategic reserves with other members of the International Energy Agency. The total release planned is 400 million barrels, with the U.S. committing to release 172 million barrels of that total. The SPR is down 58.323 million barrels since March 20 with much more potentially to be drawn from the reserve in the coming months as global crude supplies remain disrupted.

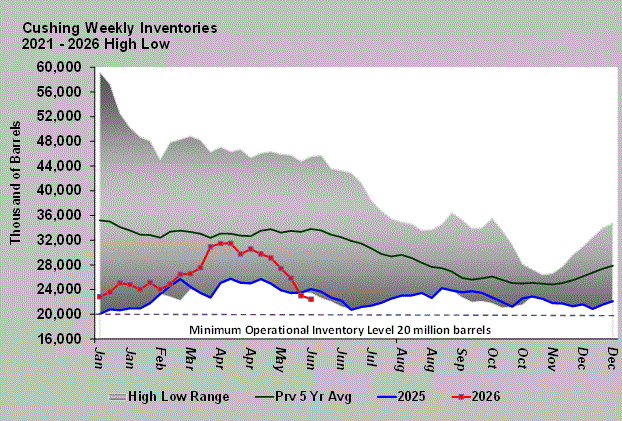

Another concerning data point is the amount of crude stored at the U.S. crude trading hub of Cushing, Oklahoma. Inventory there is now below last year and approaching the 20-million-barrel level that is said to be necessary for the facility to operate as it should. The low inventory level at Cushing has an outsized impact on U.S. crude prices.

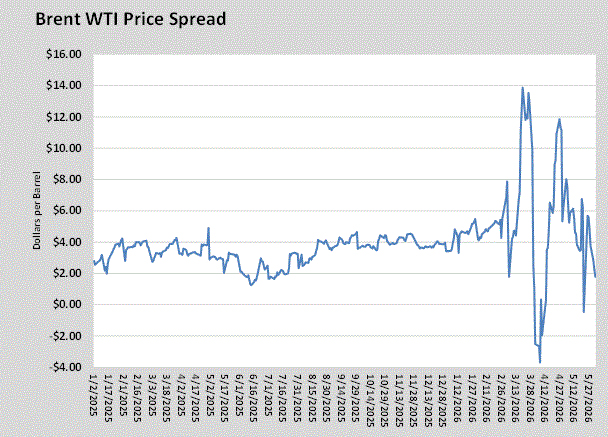

The chart below shows the spread between WTI crude and Brent crude.

It illustrates the havoc that the war has had on the global crude pricing relationships. Brent had been holding about a $4 premium to WTI before the war. The closing of the Strait of Hormuz initially caused Brent’s price to surge in relationship to WTI, but as the world turned to the U.S. for more supply, WTI briefly held a premium to Brent. Now Brent is holding a $1.79 premium to WTI as the stress on U.S. crude inventories is starting to match the stress on global inventories.

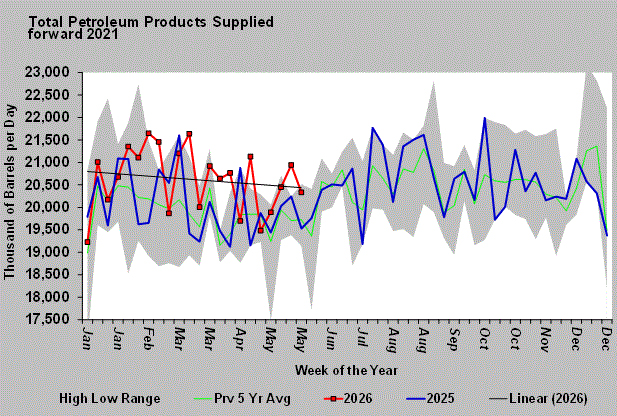

Despite high crude prices since the war began at the end of February, U.S. demand for total petroleum products (TPPS), which is essentially everything made from crude, is running higher than last year. Last week, TPPS was at 20.333 million barrels, which was about 800,000 bpd higher than the same week last year. Year-to-date TPPS has averaged 20.619 million bpd, which is 654,000 bpd higher than the same period last year.

The trend is down, but that is a seasonal pattern. The highest demand times for TPPS are still ahead for this year.

At some point something must give. High demand and rapidly falling inventories cannot exist for long without a major impact on prices. If the global crude supply picture does not change soon prices will go higher, likely dramatically higher, to crush demand.

Propane prices will be caught up in the whirlwind of rising energy prices. Also, propane has remained undervalued relative to crude even with builds in propane inventories this summer slowing down dramatically. Unfortunately, that could mean propane prices will no longer be trailing crude’s rise and could in fact outpace it.

If the Strait of Hormuz were to open soon the worst of such a scenario might still be avoided, but it remains closed and the world of pricing insanity is getting very large in the window.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Aaron Huizenga on the power of self-awareness

Jul 19, 2026 -

Geopolitics send crude and propane prices higher

Jul 13, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.