Overseas markets lift US propane prices

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, compares U.S. and overseas crude benchmarks and their impacts on propane prices.

Catch up on last week’s Trader’s Corner here: Closing of Strait of Hormuz impacts energy exports

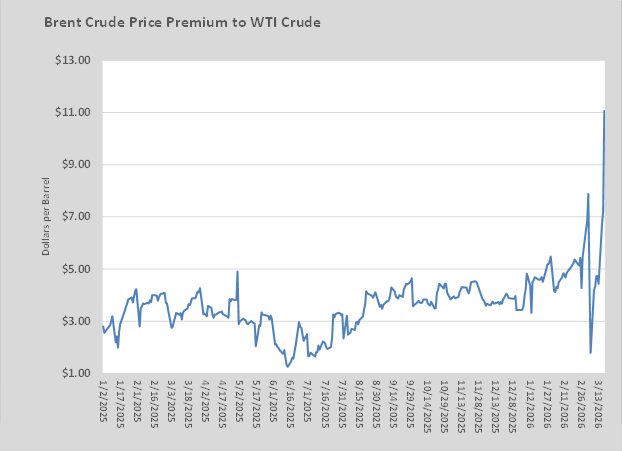

West Texas Intermediate (WTI) crude is the U.S. benchmark crude. Other U.S. crude grades, due to composition or location, are most often priced at a premium or a discount compared to WTI.

Brent crude, which is based on production from the North Sea fields, is considered a global benchmark. Many crudes around the world are priced relative to Brent.

Brent is usually priced higher than WTI, but their prices tend to move together. Many days, the price change of the two benchmark crudes is within pennies per barrel.

Over the last 10 years, Brent has averaged a $4.28 premium to WTI. There have been times when the premium has become very wide. For example, during the COVID-19 pandemic and in the months after Russia invaded Ukraine, the spread hit double digits.

During most of last year, the spread was running below the long-term average. The average in 2025 was $3.36. The closing of the Strait of Hormuz due to the United States-Iran war has caused another separation in pricing for the benchmark crudes.

As we write on Friday, March 20, the spread is $11.68. At one point in the week before, the intraday highs for Brent and WTI were nearly $20 different.

In this case, the focus on more domestic production is helping the United States. Europe has been focused on expanding its use of renewable energy instead of increasing domestic hydrocarbon production. The conversion to renewable energy may be a worthy cause, but it’s a slow process. The fact is, Europe and Asia are highly dependent on crude from the Middle East since producing hydrocarbons in Europe has become taboo and Asia lacks the reserves.

Frankly, Europe’s dependency on Russia for its energy opened the door for Russia to invade Ukraine. Now, Europe’s and Asia’s dependency on Middle East crude is allowing the regime in Iran to hold the world captive and is giving its current regime leverage to stay in power. Russia has all the hydrocarbon energy it needs; China imports a lot of hydrocarbon energy but has been building its reserves. The United States has been increasing hydrocarbon production, reducing dependency on other nations. Due to policy decisions, Europe lacks the energy leverage of those countries. Perhaps one day, Europe’s focus on renewable energy will give it the last laugh, but for now, it makes it vulnerable.

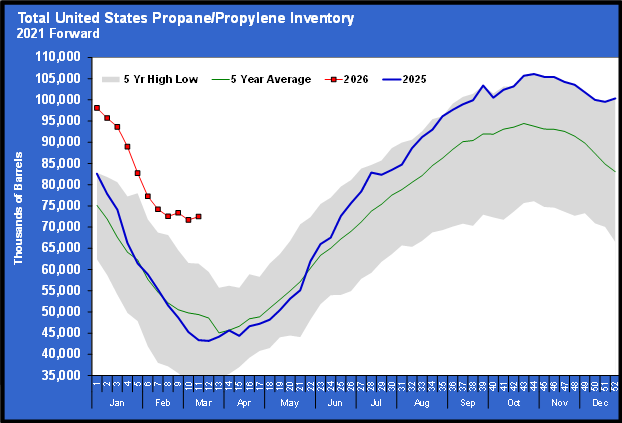

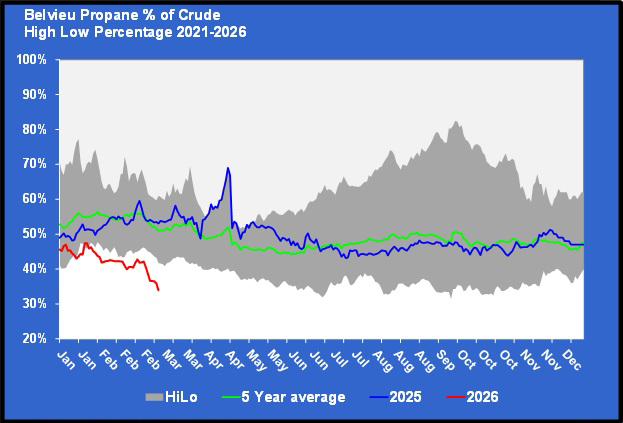

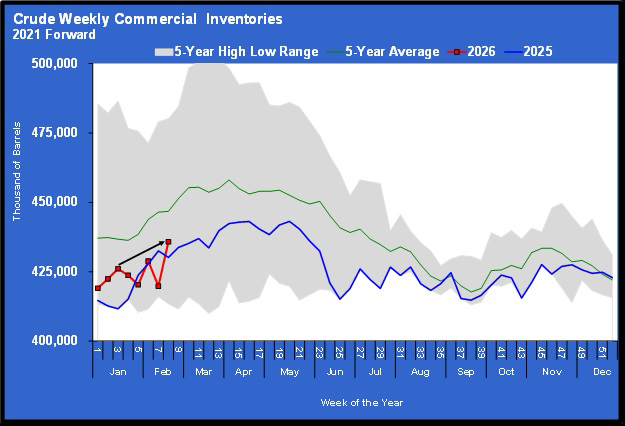

The difference in crude prices is carried over to propane. U.S. propane fundamentals are in great shape and do not warrant higher prices. In fact, last week, the Energy Information Administration (EIA) reported a build in U.S. propane inventory. It was the second build in the past three weeks.

U.S. propane inventory is 29.136 million barrels higher than it was at this time last year, and the post-winter builds in inventory have begun early. Inventory is 67.2 percent higher than this time last year and 58.5 percent higher than the five-year average for this time of year.

And yet, the robust propane inventory has not prevented supply disruptions elsewhere or the pricing disparity between crude benchmarks from lifting U.S. propane prices. The morning we wrote this piece, U.S. propane prices had jumped nearly 4 cents.

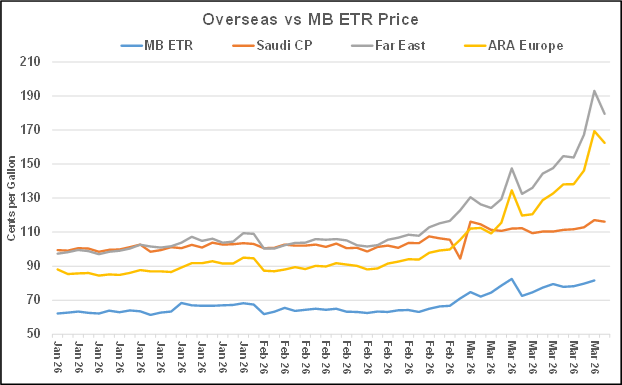

We started comparing prices in the United States and overseas markets and watching the spreads in 2014. Overseas prices are the highest they have been in that 12-year period.

In our Trader’s Corner a couple of weeks ago, we stressed how fortunate we have been in the U.S. propane industry, with our fundamentals so strong that they have largely insulated us from what has happened globally.

But we warned that the disruption of supply elsewhere and the resulting rise in global prices would mean that the cost of a Btu of propane was going to go up as the world turned to the United States for supply.

Chart 3 compares the price of MB ETR propane and overseas markets. The Saudi CP price is a supply point price just like the MB ETR. The price there is not as high as might be expected given the threats to supply in the Middle East.

The demand markets of Europe and Asia that are so dependent on supply from the Middle East are surging due to both supply issues and the rise in Brent crude’s price. Unfortunately, this is lifting the price of propane in the United States as well.

We were surprised this past week when the EIA reported a 156,000-barrel-per-day (bpd) decrease in U.S. propane exports, bringing them below 2 million bpd. With the world looking to the United States for supply, we did not expect that to happen. We expected exports to be over 2 million bpd, closer to capacity, for as long as the war in the Middle East continues.

We think the upward pressure on U.S. propane prices that has been developing over the last few days suggests the call for U.S. propane exports is there. We will once again be surprised if the EIA’s next update does not reflect an export rate north of 2 million bpd.

Collectively, the global energy market is holding its breath until the Strait of Hormuz reopens and the energy the world needs starts flowing again. When that happens, the U.S. propane market should quickly return to its favorable pricing environment for retailers and consumers.

Until then, the U.S. market is going to have to endure pricing that is higher than its own fundamental conditions would warrant.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Closing of Strait of Hormuz impacts energy exports

Mar 16, 2026 -

Impacts of US-Iran conflict on propane market

Mar 9, 2026 -

Making sense of volatile crude inventories

Mar 2, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.