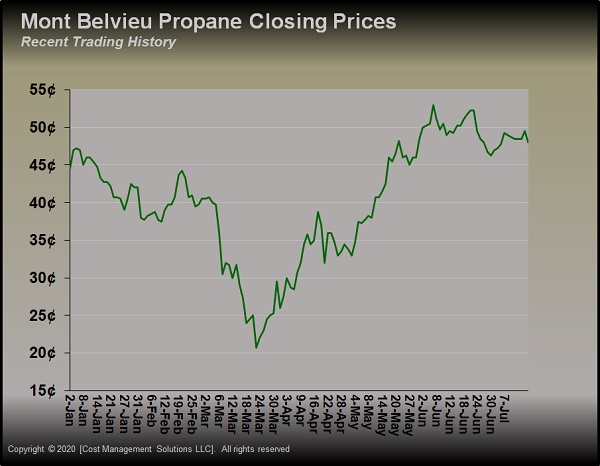

Propane trends near 50 cents per gallon, 50 percent of WTI crude value

In last week’s Trader’s Corner, we discussed how any upside in propane is likely going to be driven by its own fundamentals becoming more supportive. We discounted the prospect that rising crude prices would pull propane prices higher as our strong bias is that West Texas Intermediate (WTI) crude will stay around the $40-per-barrel price level for the foreseeable future. That theory got support last week when the crude-producing nations that make up the Organization of the Petroleum Exporting Countries plus their producer allies led by Russia (OPEC+) said they would raise production by 2 million barrels per day (bpd) beginning in August and running through December.

This was part of the original plan when OPEC+ cut 9.7 million bpd from its benchmark production rates starting May 1. OPEC+ announced last week it was sticking with its plan to raise production in August despite the fact that rapidly rising cases of COVID-19 are causing some governments to once again restrict travel and economic activity. This fits our narrative that OPEC+ would err on the side of caution in making sure that WTI crude does not move much above the $40-per-barrel mark for fear higher prices would cause a resumption in U.S. drilling activity.

Right now, OPEC+ is getting exactly what it wants. U.S. crude production is 2 million bpd less than its peak, and drilling activity is at record lows. For the week ending June 10, the United States had just 181 rigs actively drilling crude wells, down 603 from the same week last year. OPEC+ knows that the depletion rate on wells drilled into shale formations is extremely fast compared to conventional wells. Thus, low rates of drilling activity could make the reductions in U.S. production last longer.

COVID-19 has done for OPEC+ what it had not been able to do on its own, which is to significantly damage the U.S. oil and gas industry and possibly relegate it to the world’s swing production. OPEC+ would rather bring its own production on too quickly and drive prices lower in the short run than allow prices to go too far above the $40-per-barrel mark. That is a significant price level since it is the break-even point for much of the production coming from U.S. shale formations.

While $40 could be enough for producers to reopen shut production, it will not be enough to justify more drilling. If OPEC+ were to allow crude prices to venture too far above $40 per barrel, even for a little while, U.S. producers would likely be quick to hedge their future production and open the door for more drilling. There is every incentive for OPEC+ to hold prices at the $40 mark so U.S. shale producers slowly watch their revenues decline, deepening their financial troubles and pushing more of them into insolvency.

All of this background on crude backs up the idea that any movement in propane prices in the short term is likely dependent on propane’s own supply/demand fundamentals.

As crude prices have stalled, U.S. propane fundamentals have also become less supportive of higher prices. At the moment, that has propane stuck at two 50s. Its nominal price is staying around 50 cents per gallon, and its value relationship to WTI crude is holding around 50 percent.

Chart: Cost Management Solutions. Click to enlarge.

As the first chart shows, propane prices rallied from March through May on rising crude and supportive fundamentals. Since the first of June, the price leveled out around the 50-cents-per-gallon mark.

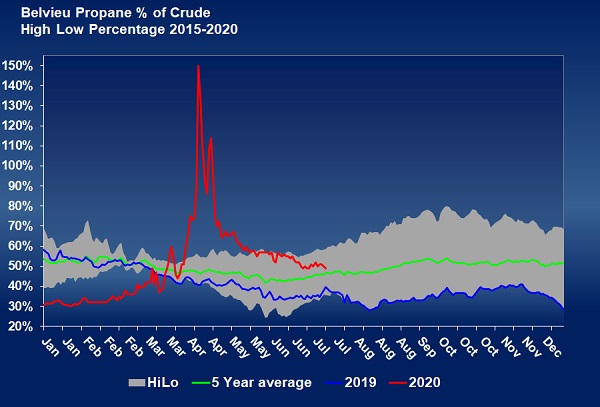

Meanwhile, the second chart shows that propane’s value relative to crude has leveled off at around 50 percent. That simply means the market is valuing propane at half the value of crude.

Chart: Cost Management Solutions. Click to enlarge.

For propane to break out of these 50/50 flat lines into upward trending lines, a change in propane fundamentals will have to occur. The latest data suggests that is not yet happening. In last week’s Trader’s Corner, we posed some questions after a drop in U.S propane production and rise in propane exports: Will production fall more or at least level out? Will exports become robust like they were at the beginning of the year and last week, or will they go back into the doldrums seen between mid-April and mid-June? With Canadian inventories building, could imports from Canada improve? They jumped last week after being subdued most of the year. As propane buyers stand at a crossroads, these are the questions we should be asking.

For the week ending July 10, the Energy Information Administration (EIA) reported U.S. propane production bounced 71,000 bpd to 2.260 million bpd. Propane exports tumbled 432,000 bpd to 901,000 bpd. Those data points helped lead to an above-average, 3.525-million-barrel build in U.S. propane inventory. Those were all very bearish fundamental numbers for propane. Though propane imports did drop 51,000 bpd, it was not enough to offset the bearish numbers elsewhere. It was certainly not enough to break propane above 50 cents per gallon or above 50 percent of the value of WTI crude. In fact, since that data release, propane is trending below the 50/50 lines. U.S. propane inventory that was even with 2019 in June is now 7.195 million barrels higher than last year at this time.

Propane prices dipped to around 20 cents per gallon and 37 percent of WTI in March. Propane inventory had started 2020 more than 19 million barrels above where it started 2019. But the fundamentals changed, causing the inventory overhang to be eliminated and pushing propane to the 50/50 marks. At the beginning of this transition, the fundamentals and eventually the upswing in crude prices pointed strongly at the need for price protection. The fundamentals were flashing buy, go, be aggressive. But now the fundamentals are flashing caution, be careful, be patient.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

The US, Iran and propane: A retrospective

Jun 22, 2026 -

Iran peace deal’s impact on propane markets

Jun 15, 2026 -

How the US-Iran war draws on propane inventory

Jun 8, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.