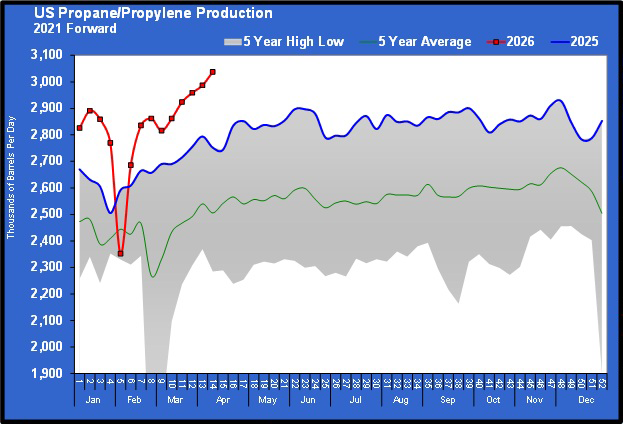

US propane production reaches over 3 million bpd

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, examines the impact of record-high U.S. propane production numbers.

Catch up on last week’s Trader’s Corner here: Crude production declines; prices surge

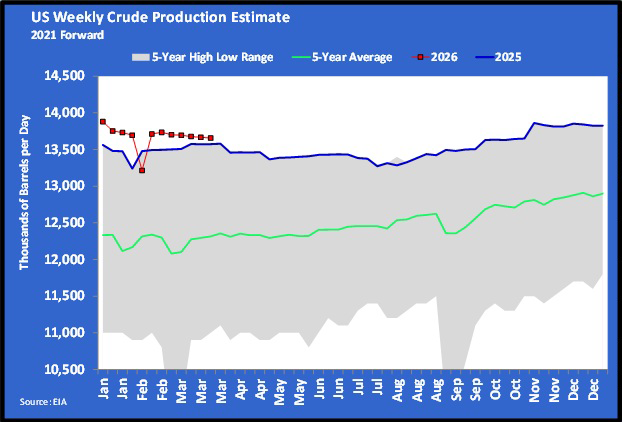

The Energy Information Administration (EIA) recently released its Weekly Petroleum Status Report for the week ending April 3. It showed U.S. propane production up 51,000 barrels per day (bpd) to 3.038 million bpd. It was the first time ever that U.S. propane production averaged more than 3 million bpd during a week.

U.S. domestic demand has not been growing, and unfortunately, this winter turned out to be very mild after the winter storm at the start of the new year. Heating degree-days are now slightly behind last year. For several years in a row, heating degree-days have been below the long-term average.

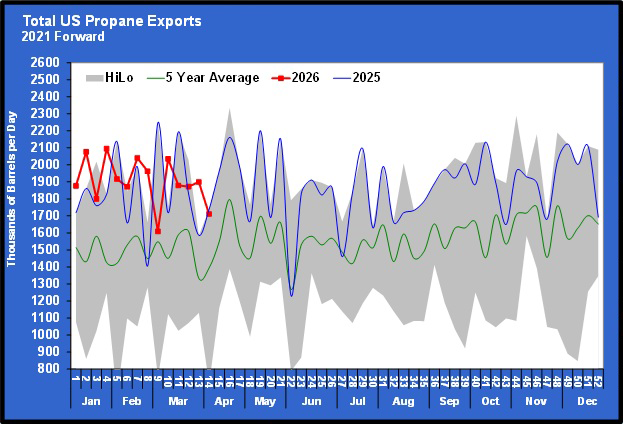

With this kind of production and stagnant domestic demand, propane exports are the only way to offset the high production and balance supply and demand. However, export capacity is limited. The highest average weekly exports reported by the EIA were 2.248 million bpd, which occurred in March of last year. But it has been impossible to keep that kind of export rate going for extended periods.

For all of 2025, the export rate averaged 1.862 million bpd, and during the first 14 weeks of the year, it averaged 1.834 million bpd. During the first 14 weeks of this year, exports averaged 1.903 million bpd, up 69,000 bpd.

Meanwhile, propane production has been 167,000 bpd higher than last year over the first 14 weeks. U.S. propane demand averaged right at 1 million bpd last year, and during the first 14 weeks of this year, it has averaged 1.325 million bpd. That was 62,000 bpd less than the same period last year.

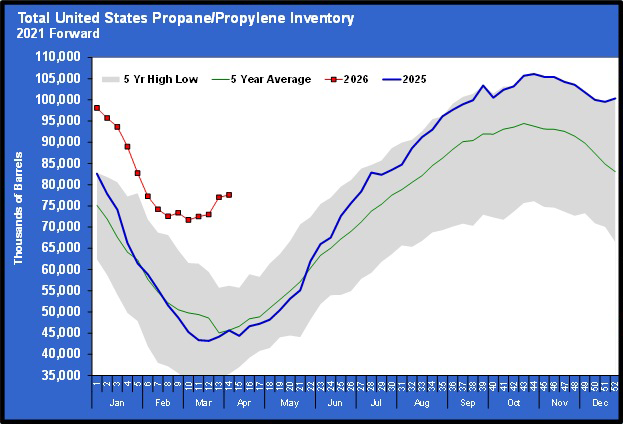

With that kind of supply/demand imbalance, it is not surprising that propane inventories are at record highs.

Propane prices have been up recently, but it has nothing to do with propane fundamentals. Fundamentally, the path of least resistance for propane is lower.

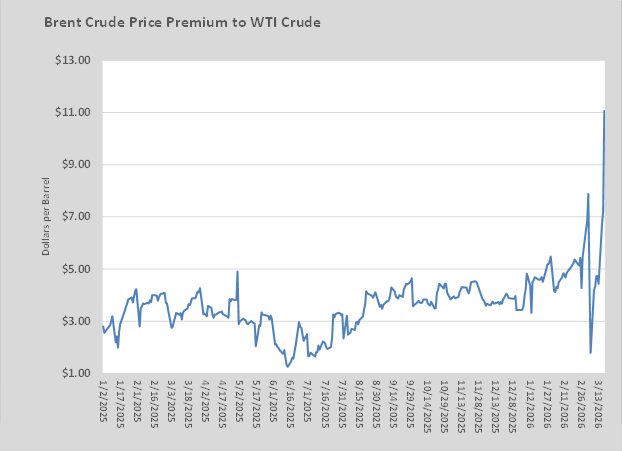

The gain in propane prices has been a function of higher crude prices related to geopolitical events. But the oversupply in propane has limited its upside, causing its price to significantly lag the upswing in crude’s price.

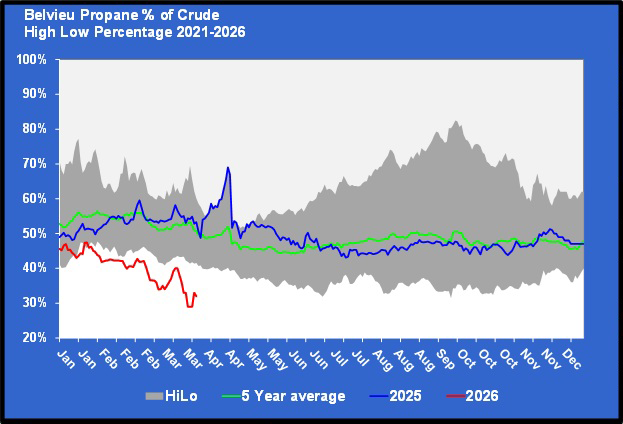

As a result, propane is trading at a very low value relative to the value of WTI crude.

Mont Belvieu Energy Transfer (ETR) propane is running at about 32 percent of the value of WTI crude. MB Enterprise (ENT), MB Targa (TAR) and Conway are all valued at a lower relative value to crude than ETR.

Meanwhile, refined fuel prices that have not had the luxury of strong fundamentals like propane have become much more painful for consumers. Even with a major drop in prices on April 7 when the ceasefire between the United States and Iran was announced, distillates, including heating oil, are valued at 163 percent of the value of WTI crude or the Btu equivalent of $2.53 per gallon of propane. Gasoline is only slightly better at 129 percent of WTI and the equivalent of $2.21 per gallon of propane.

The greatest threat contributing to higher propane prices is the higher price of energy overall, which puts upward pressure on propane prices despite the strong fundamental conditions. Even though propane trades at a low percentage of crude, its price is still rising with the overall market.

It is our conviction that something must give on the price of crude in a relatively short time frame. The global economy is showing the strains of high energy prices already, and it won’t be long before that strain turns into a global economic recession, which will hurt demand. Lower demand will result in lower crude prices at some point.

The more likely outcome is that the world will find a way to force the Strait of Hormuz open despite Iran’s attempts to keep it closed. Or the world will succumb to Iran’s demands and pay it to use the Strait of Hormuz. Some countries have already paid, but many say it is unacceptable for one country to restrict freedom of navigation in this way.

Either way, whether you crush demand or you force supply to flow again, crude prices will have to come down sooner rather than later.

If that is a wrong statement and crude prices remain up, it will only contribute to higher propane supplies. Some U.S. crude producers have already committed to increasing capital spending for crude drilling in the second half of this year, and others are considering it.

That will increase propane production that is associated with the higher rate of crude production. They are already completing more of the wells that they had drilled but chose not to immediately complete.

The closing of the Strait of Hormuz is limiting global LNG supplies as well. Somewhere around 18 percent of the global LNG supply is impacted. If that continues, there will be enough demand for U.S. LNG to max U.S. export capacity. At least that will keep natural gas production at or slightly above where it is currently running. And as we saw above, that is already enough to put U.S. propane production at an all-time high.

Governments, militaries and markets are eventually going to sort out this energy mess, but whatever path they take, U.S. propane should remain oversupplied with prices moving in the favor of buyers when not overwhelmed by geopolitics.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Crude production declines; prices surge

Apr 6, 2026 -

Overseas markets lift US propane prices

Mar 23, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.