Opportunities in propane prices

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, looks ahead at propane prices in the new year and beyond, and explains the relationship between propane and crude oil.

Catch up on last week’s Trader’s Corner here: Top 10: The best of Trader’s Corner 2024

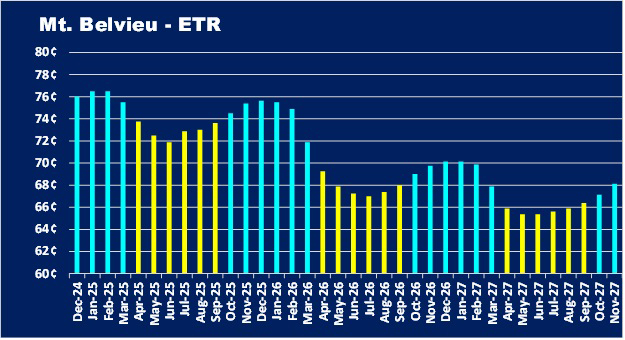

The primary purpose of this Trader’s Corner is to let propane buyers know that the best value for propane is further into the future. The chart below shows the price of propane for the current month and 35 months out. Any propane buyer can lock in these future prices using swaps.

The winter months are blue, so it’s easy to see where the value resides. Mont Belvieu ETR propane buyers can lock in swaps to cover the months of October 2026 through March 2027 at an average of around 69.75 cents and the start of the following winter at 68.125 cents. That price is about 9 to 10 cents better than what the winter months have averaged over the last 10 years. Ultimately, we won’t know if propane price protection acquired at those prices for that time period will be a good buy until those months have come and gone. However, we do know that buying so much below the long-term average greatly increases the chances that it will be a good price.

OK, that’s what we wanted to share, so Merry Christmas and Happy New Year and see you next time.

Ah, heck, we like hanging out with you guys, so let’s go another round, shall we?

Let’s have some fun, do lots of imagining and get into the details of why that opportunity above exists.

First, imagine that propane is crude oil’s little brother. Little brother admires big brother and likes to do what big brother does. If you plot the movements of the two brothers, you will find that little brother follows the movements of big brother closely most of the time.

Little brother has averaged 43 percent of the value of big brother this year. Occasionally other things get the attention of little brother, and he wanders off from big brother. Little brother’s value has ranged from 31 percent to 54 percent of big brother’s value this year. But establishing the median value of little brother shows he doesn’t wander off for too long. The median has been 42 percent.

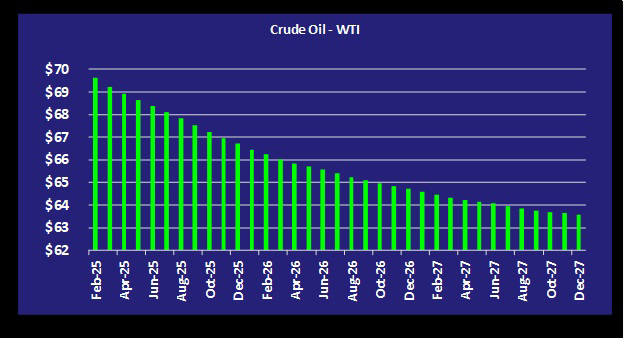

Now that you are absolutely convinced of this strong bond between propane and crude, let’s look at crude’s forward price curve.

Little brother has a short attention span, so what makes him wander off from big brother are bright, attention-getting things right in front of him, like weather or big inventory draws. So, any separation between the brothers is generally in the nearby months. So, the further out we go, the more crude influences the price of propane. Thus, propane prices well into the future are more closely reflecting the crude values plotted above, giving propane buyers the best values.

OK, we are on a roll, so the next round is on me. Let’s do some more imagining to understand how the crude prices above get established. Imagine you are a refinery … I know, I know, but work with me here. You go down to the crude restaurant owned by the crude producer. When you walk in, you note that all the tables are full of other U.S. and foreign refiners. You walk to the counter and ask the producer if he has crude and he says, “Yes, we’re well stocked. What will you have?” You are very hungry and ask for 10,000 barrels of crude. He says it will be $70 per barrel. You gladly pay the man because you’re starving.

Being the wily old salesman, the crude producer knows it might not be as busy next month. He knows he has plenty of crude on the way and offers you a gift card if you want to lock in your price for next month. You ask how much, and he says $70, of course. You say you will wait since you are mostly interested in what you need today. He says, “I tell you what, I will give a discount on the gift card – 10,000 barrels at $69.50.” You agree.

The producer realizes you aren’t really interested in the crude you will need further out, but has established that you have a hard time passing up a bargain, so he offers a gift card for the next month at $69 and so on and so forth. You walk out with a pocket full of gift cards with each one giving you 10,000 barrels of crude at a slightly lower price. Those gift cards are the equivalent of a swap.

You are happy, and the producer is happy because he can make plenty of profit even at the discounted price of the gift cards. You and the crude producer have just created a backwardated price curve like the one above for the crude you will buy. In a normally supplied market, this is what the price curve for crude most often resembles. And that is why, typically, there are good values for propane further out as well.

Now, let’s say you use all of your gift cards and return to the restaurant. You note that most of the tables are empty. You mention it to the restaurant owner, and he agrees it is slow and says he has an all-you-can-get deal for $65 per barrel. You agree to 11,000 barrels at that price. You like a good deal, so you offer to buy next month’s crude at $65 per barrel. The producer says he thinks it will be busier that month. You are not sure, but you like the price, and you offer $65.50 per barrel and the producer (who really isn’t sure it will be busier) agrees. You follow the same pattern and leave with a pocket full of gift cards, each with a slightly higher price than the preceding month. But you feel even the highest price you paid is a good bargain.

In this case, the price structure you have established for your crude is the opposite of the chart above. The price structure where the price is higher with each subsequent month is called a contango price structure. This can happen when the market is oversupplied. However, the assumption is generally going to be that whatever is causing the oversupply will be resolved in the future.

Currently, crude inventories are on the lower side. The inventories are not low enough to cause a run-up in prices since crude production is high and there is a lot of spare production capacity. Also, there is an expectation that crude will remain oversupplied in 2025, and inventories will build. The current tightness in inventories is why the value for the winter of 2025-26 is not as good as the further-out winters.

To be successful, propane buyers need to understand the relationship between crude and propane and understand the impact of the crude forward price curve on propane’s price. They also need to understand what factors impact crude’s future price and lead to the different pricing structures we have discussed. They need to monitor the impact these factors have on crude’s forward curve because that will ultimately be reflected in propane prices.

All right, bottoms up, then. Hope it’s been a great year and the next will be even better.

All charts courtesy of Cost Management Solutions

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Faces & Places: July 2026

Jul 24, 2026 -

Aaron Huizenga on the power of self-awareness

Jul 19, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.