Reassessing after a surprising draw on propane inventories

Trader’s Corner, a weekly partnership with Cost Management Solutions (CMS), analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, examines the state of U.S. propane inventories after recent draws.

Catch up on last week’s Trader’s Corner here: Global demand increases for US propane exports

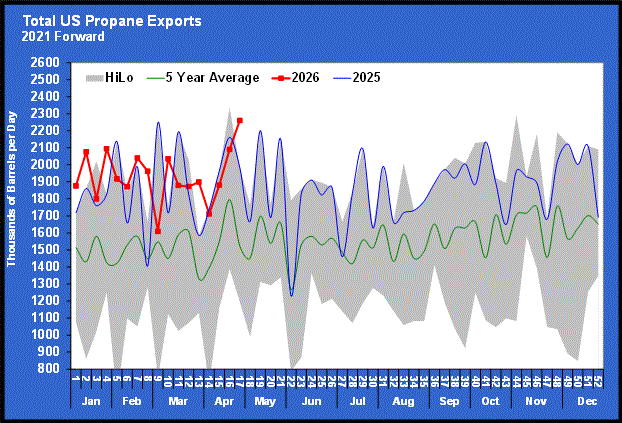

In the previous Trader’s Corner, we focused on U.S. propane exports, since they appeared to be increasing with the possibility of changing the trajectory of propane inventory accumulation. We noted that propane exports had gone above 2 million barrels per day (bpd) for the week ending April 17, which was the first time that had happened since the U.S.-Iran war had started.

Soon after the war started, we made predictions in Trader’s Corners that exports would increase, so each week we were surprised when they did not. It took the global market a little longer than we expected to respond to the supply disruptions from the Middle East.

We expected that an increase in propane exports would slow the buildup in propane inventories. Though we still expected a high inventory position to start next winter, we imagined a slower build, which would cause upward pressure on propane prices. After all, propane was being valued very low against other energy sources, so there was room for prices to move up, even with the slightest change in the fundamental picture.

What we did not expect, even with an increase in exports, was a draw on U.S. propane inventories this time of year. However, the Energy Information Administration, in its Weekly Petroleum Status Report for the week ending April 24, reported a draw on inventory. At 1.144 million barrels, the weekly inventory drop was not negligible. Weekly inventory drops in that range from now until the start of winter would be an absolute game-changer for propane prices.

The propane supply side (production and imports) was practically unchanged from the previous week. The key to the inventory draw was what happened on the demand side. U.S. propane exports increased 170,000 bpd to 2.260 million bpd.

Chart 1 shows that sustaining that level of exports over an extended period is unlikely, but until proven otherwise, we can’t completely discount the possibility. Propane export economics suggests the incentive to export as much as possible is present. U.S. propane exports averaged 1.812 million bpd in 2025, so to sustain an export rate anywhere near last week’s amount is going to require a rather substantial departure from normal. It is going to require the U.S. export facilities to operate extremely efficiently. Even at that, we are not sure it is possible to sustain that rate.

More export capacity is coming online that can export propane, butane or ethane. But most of that “flex” capacity is already dedicated to ethane. Some capacity additions can be used for just propane and butane exporting. There is 300,000 bpd of new LPG (propane/butane) capacity coming online in the second half of the year. If we assume a 90 percent capacity utilization rate, with about 80 percent of that being used for propane exports, that would be about 216,000 bpd.

With that kind of increase in propane export capacity, we could assume last week’s 2.260 million bpd export total would be sustainable starting in the second half of the year.

U.S. domestic demand was up 294,000 bpd to 988,000 bpd for the week ending April 24.

Domestic demand in the United States is on a relatively flat growth trajectory, so we should expect it to gravitate toward the norm. Last year, domestic demand from the first of May until the end of September was 753,000 bpd, and the five-year average for that period is 833,000 bpd. Somewhere in the range of those two points is what we should expect. Higher propane prices would push toward the lower end of the range, and lower prices would push toward the upper end. Since crude prices are on the high side, let’s assume that propane prices will be high, which will cause summer demand to be below the five-year average. A summer domestic demand rate of 800,000 bpd is probably a good assumption. That would be 188,000 bpd less than last week’s rate.

The timing of the new export capacity being fully employed is hard to determine. If we assume that capacity is fully employed by Aug. 1, that would be two months when a rate of 2.3 million bpd could be sustained. For the remaining three months, let’s assume a rate higher than last year’s average of 1.812 million bpd, since strong export demand will keep export rates closer to capacity. We like somewhere around 1.9 to be the average over the next three months, but we will err on the conservative side at 2 million bpd. That would make the average export rate 2.12 million bpd over the next five months.

Combined with 800,000 bpd of domestic demand, that would be a total demand of 2.92 million bpd. U.S. propane production has averaged 2.858 million bpd this year. But that includes a sizable hit during the winter storm. That won’t happen this summer. The average since the impacts of the winter storm were behind the market has been 2.928 million bpd. We think production can be sustained at that level, barring any fractionator issues.

That puts demand and U.S. production near equal. When propane imports are added, we could expect an average build in U.S. propane inventory of about 94,000 bpd. That would be 672,000 barrels per week for 20 weeks or 13.44 million barrels by the start of winter.

Combined with current inventory, that would be 92 million barrels at the start of winter. A far cry from the 106 million barrels available at the beginning of last winter. If that turns out to be the case and the war between the United States and Iran continues, then propane prices will be elevated.

We could expect propane to be valued at 50 percent of WTI or higher under those conditions. If WTI were at $100 this fall, that would result in propane valued at $1.19 per gallon.

But as we contemplate this possibility, we must consider that propane production has the best chance of averaging above the numbers we used above. Foreign buyers are not only racing to U.S. shores for propane, but they are also seeking out crude. U.S. crude exports jumped 1.640 million bpd last week to 6.438 million bpd. That was 2.317 million bpd more than the same week last year. More export demand and high crude prices are going to encourage more U.S. crude production, which will increase propane production.

We should also expect the demand for liquefied natural gas (LNG) exports to be near capacity, which should help with propane supply as well. Consequently, we would not be surprised by a higher inventory level to start winter and less price pressure than current conditions suggest.

But the most important thing to consider is this: The tightness that everyone is now talking about is being caused by an event, the closing of the Strait of Hormuz, resulting from the U.S.-Iran war. It is hard to imagine that the waterway will still be closed when winter starts.

So, buyers must guard against being too pessimistic about propane prices and over-hedging at elevated prices. At this point, however, buyers should not count on enjoying the low propane values from before the war anytime soon. And that includes the scenario where the Strait of Hormuz opens sooner rather than later. Even if the strait opens later today, it is going to take a while for the price of crude to come down to the $60-per-barrel, pre-war price level.

We will know soon enough whether our assumptions about export rates and domestic consumption for the next five months are off. If several weeks are strung together at last week’s rates and propane production does not increase, then buyers might be forced into a more defensive position.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Unexpected rise in US propane inventories

Aug 3, 2026 -

Propane Personality: Lisa Gerwitz

Jul 29, 2026 -

Distillate prices becoming brutal

Jul 27, 2026

About the Author: Chris Markham

Chris Markham is the managing editor of LP Gas Magazine. Contact him at cmarkham@northcoastmedia.net or 216-363-7920.

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.