Geopolitics send crude and propane prices higher

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, explains how the renewed hostilities in the Strait of Hormuz have impacted crude and propane prices.

Catch up on last week’s Trader’s Corner here: Jones Act waiver opens new possibilities for propane

Two weeks ago, we wrote that crude was not out of the woods yet, even though crude prices had already fallen below the $75-per-barrel level that we figured would be the anchor price for crude until commercial crude inventories around the world were replenished. Crude prices had fallen because a 60-day ceasefire between the United States and Iran had been announced to give the two combatants a chance to negotiate a long-term peace deal. A key component of that ceasefire agreement was that Iran would not threaten commercial shipping on the Strait of Hormuz.

As a backlog of crude began to move out of the Persian Gulf, through the Strait of Hormuz toward much-relieved buyers desperate for supply, crude prices started falling. Persian Gulf producers were very aggressive in selling their pent-up production, given that they badly needed revenue and had doubts about how long the Strait of Hormuz would remain open. Doubts that turned out to be well founded.

The memorandum of understanding (MoU) between Iran and the United States that began the 60-day ceasefire and period of negotiations was signed on June 17. WTI crude had reached $108.66 before hope of a peace agreement started to emerge. By the time the MoU was signed, WTI was at $76.69 and the U.S. benchmark crude hit $68.55 per barrel by June 6.

But the downtrend ended, and prices turned higher after Iran’s Revolutionary Guard decided it would be a good idea to attack three commercial ships as they traversed the Strait of Hormuz. This prompted the United States to conduct strikes on Iranian military targets around the strait. In response, Iran attacked U.S. bases in the region. As a result, WTI crude is over $72 per barrel as we write.

The fact is that not all the leadership in Iran wants peace with the United States. In fact, we believe it is possible that those wanting a negotiated peace are in the minority, thus there doesn’t appear to be centralized control inside Iran. It creates a situation where a Revolutionary Guard commander with a hatred for the United States and access to missiles and drones could attack commercial shipping even as other leadership elements in Iran negotiate a long-term peace agreement.

It appeared President Donald Trump had reached his frustration limit with the situation, saying that Iran’s leadership was scum and that he did not want to negotiate with them any longer. He said Iran could not be trusted to adhere to any deal, so what was the point of negotiations? Yet, technical talks between the United States and some elements of Iranian leadership continued, trying to hammer out details of a long-term peace agreement even as missiles were flying.

Until there is a strong enough element inside Iran to gain full control of all military assets, uncertainty about crude supply from the Persian Gulf is likely to continue. When we argued two weeks ago that crude prices would likely move back to the $75 range, it did not even consider a failure of peace talks and the Strait of Hormuz becoming closed again. Unfortunately, the recent developments have caused shipping activity on the Strait of Hormuz that was steadily ramping up to slow again. Some reports are that ship traffic is nearly at a standstill.

Fortunately, both crude and propane markets have remained reasonably under control despite these unfortunate developments. It appears that there has been enough mixed messaging about the peace talks that traders have decided to take a wait-and-see approach for a few days. After the initial jump in crude prices following Iran’s attacks on shipping, they fell yesterday (July 9) and are mostly flat to lower this morning.

Mont Belvieu ETR propane had dropped to 69.75 cents before the resumption of fighting. The price jumped to 76.875 cents in just two days, but has thankfully given back much of the gain over the last two days. MB ETR propane opened at 71.75 cents as we write on the morning of July 10.

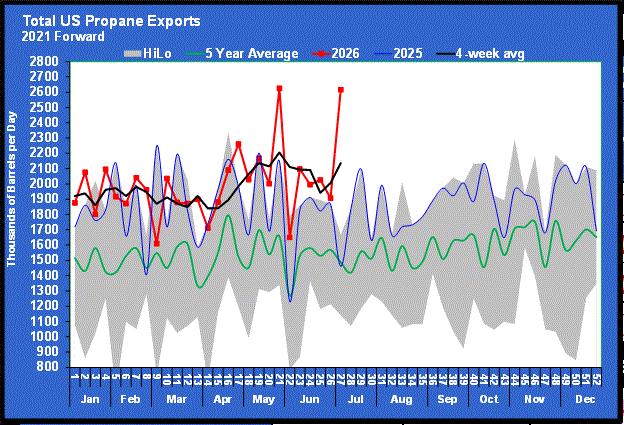

The lack of sustainability in propane’s price rally was made even more remarkable in that propane got strong fundamental support when the latest data from the Energy Information Administration (EIA) was released on July 8. The EIA showed U.S. propane inventories making a surprise drop of 845,000 barrels.

It is a time of year when we would expect propane inventories to steadily increase. But this year has been anything but normal, and foreign buyers that typically source supplies from the Middle East have come to U.S. shores as their normal supply sources became unavailable.

In fact, the surprise draw on propane inventories was a result of propane exports surging back to near record highs at 2.616 million barrels per day.

We don’t think an export rate that high is even possible. The unusually high export rates we believe are the result of reporting issues to the EIA. So, we focus on the four-week average, which is the black line. Even so, the four-week average shows exports are running very hot.

We were confident that propane export rates would remain high, even during the 60-day ceasefire, with commitments already made and as buyers replenished inventories. And, even with the ceasefire, as recent events have shown, supply from the Middle East was far from certain.

At this point, we are not too out of sorts about crude and propane prices rebounding to where they are currently, since we expected them to be even higher than they are now once the initial surge of crude supplies from the Middle East was gone. We are pleasantly surprised that the renewed fighting between the United States and Iran has not pushed prices even higher.

Unfortunately, while we remained confident that crude would settle in at around $75 per barrel until commercial crude supplies were replenished, recent events have greatly increased the risk of crude’s price moving higher than that mark. It is an unfortunate situation for all propane buyers because the uncertainty in the Middle East is going to make hedging even more challenging than usual. Had the peace agreement held and a long-term peace deal between the United States and Iran been signed, we believe propane prices would have been settled enough heading into winter to take a lot of the uncertainty of supply planning out of the equation. In other words, prices were likely to have been low enough to take a lot of the downside price risk out for hedgers.

But as of now, a military end to the U.S.-Iran conflict is as likely as a diplomatic end, and a military end will almost certainly take longer than 60 days, which will take us into the winter period. We will continue to hope for peace, but we do not believe the political situation in Iran is settled enough to allow that to happen. Frankly, it is hard to imagine what chain of events would have to occur inside Iran that would allow a faction in favor of peace with the United States to gain enough control to make that a reality.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Crude still not out of the woods

Jun 29, 2026 -

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.