The US, Iran and propane: A retrospective

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, looks back on his recent analyses and predictions about the U.S.-Iran war.

Catch up on last week’s Trader’s Corner here: Iran peace deal’s impact on propane markets

In our May 5 Trader’s Corner, we noted that foreign buyers had finally turned to the United States for propane supply and provided an outlook on what that would mean for propane inventories as long as the war lasted. Now that the Strait of Hormuz is open again, we thought we would go back and see how our outlook compared to reality. It would be helpful if you could look at the Trader’s Corner where we made those predictions in order to get a better feel for our rationale.

Keep in mind that exports had just jumped 170,000 barrels per day (bpd) that week to 2.260 million, which at the time was a record high. We noted how much more that was than the 1.812 million barrels that propane had averaged in 2025 and questioned if that rate was sustainable. We then pointed out that new export capacity was coming online.

We went on to predict that propane exports would average 2 million bpd until the Strait of Hormuz reopened.

Including that week’s export demand, the average export rate was 2.103 million bpd, so we were 103,000 bpd short on our prediction for exports. One of the reasons is that the new export capacity that we were predicting would not be fully impactful until later in the year came online sooner than we expected. We had noted that the timing of that capacity coming online would influence the actual outcome.

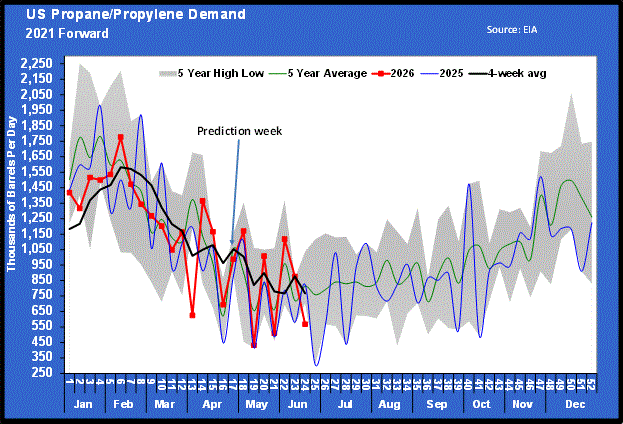

We also noted that U.S. demand for propane had been running high, but we expected it to gravitate toward the norm in the coming weeks. We predicted a domestic demand rate of 800,000 bpd.

Though extremely volatile, domestic demand has averaged 33,000 bpd higher than we predicted at 833,000 bpd.

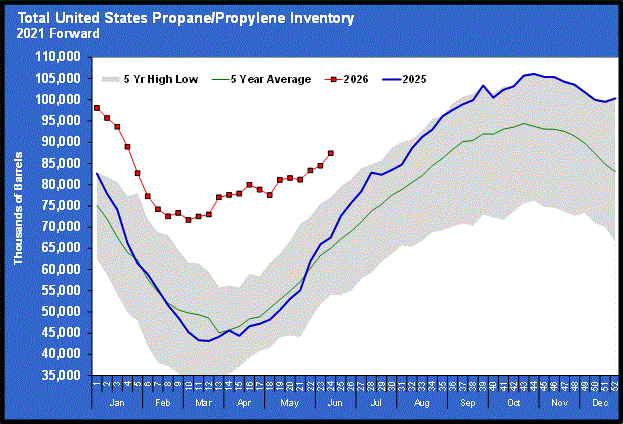

We went on to predict that U.S. propane inventories would average an increase of around 94,000 bpd, based on our demand forecasts.

Despite the demand rate being higher than we predicted, propane inventories increased by more than 94,000 bpd. The actual rate was 141,000 bpd.

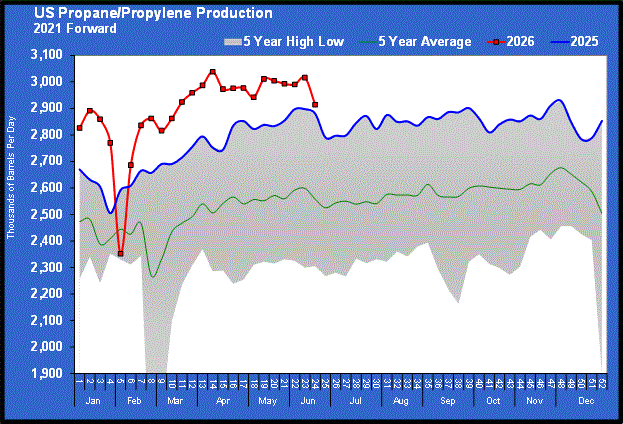

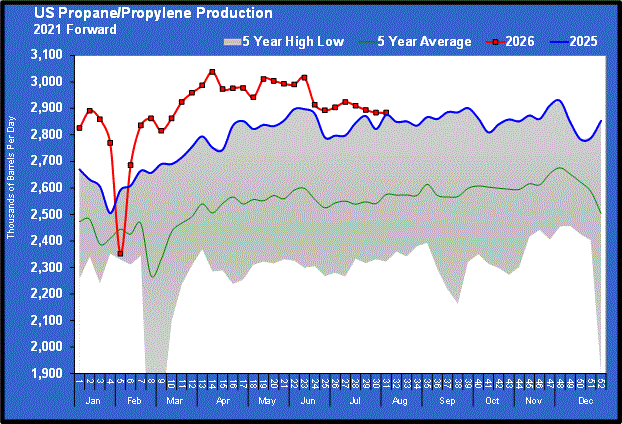

We had pointed out that propane production had averaged 2.928 million bpd that week since the winter storm in February and that fractionators would likely respond to the increased demand. Specifically, we said, “But as we contemplate this possibility (94,000 bpd increase to inventories), we must consider that propane production has the best chance of averaging above the numbers we used above.”

Even with a surprisingly large drop last week, propane production averaged 2.981 million bpd, which was a 39,000-bpd average increase.

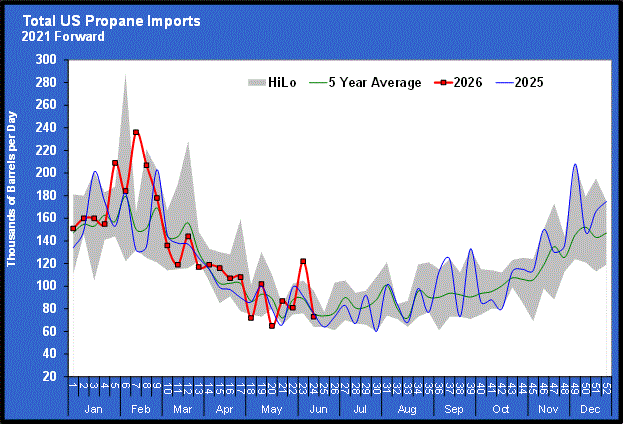

Propane imports held up well enough, averaging about 86,000 bpd during the period.

Overall, though our prediction on demand was slightly low, fractionators did respond as we expected, which allowed inventories to build at a rate that kept panic out of the market.

However, as we pointed out last week, we expect propane exports to remain elevated for a couple of more months as foreign buyers replenish inventories. Because of that, we predicted last week that propane prices would not fall far, even though the Strait of Hormuz is open.

As we stated last week, we expect $75 per barrel to become the anchor price for WTI crude, while global crude commercial inventories are replenished. If that holds true, we predicted MB ETR propane in the 73-84 cents range to start winter. Crude is currently at $74.90, and MB ETR is at 73.875 cents.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Propane retains good value as demand declines

Aug 10, 2026 -

Unexpected rise in US propane inventories

Aug 3, 2026 -

Distillate prices becoming brutal

Jul 27, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.