Much-needed propane inventory build

Trader’s Corner, a weekly partnership with Cost Management Solutions (CMS), analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, provides a welcome update on the state of U.S. propane inventories.

Catch up on last week’s Trader’s Corner here: Propane prices remain stable, relatively cheap

In the last two Trader’s Corners, we looked at the cause of the unusual draws in U.S. propane inventories and tried to reassure that the odds did not favor the draws continuing. The draws that amounted to 2.5 million barrels were concerning and occurred due to an increase in export demand coupled with doggedly high domestic demand.

In fact, it was the unseasonably high domestic demand that was largely responsible for the last inventory draw. Domestic demand was 1.170 million barrels per day (bpd) for the week ending May 1. In our most recent article, we said we remained confident that the domestic demand rate would not persist. In our forecast where we argued that inventory builds would resume, we used an average domestic demand rate of around 800,000 bpd.

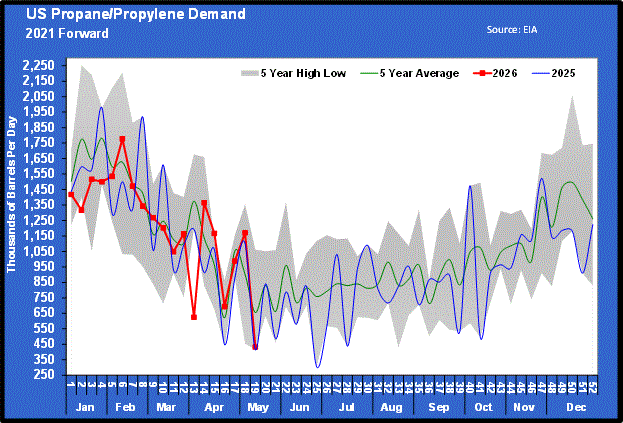

We were reasonably confident in that demand rate because of historical demand patterns and the fact that U.S. domestic demand is not growing. A drop back to normal on the domestic demand side would allow U.S. production and imports to keep up with increased export demand and allow inventories to once again build, albeit likely at a slower rate than before the U.S.-Iran war. The war caused ships to stop using the Strait of Hormuz, disrupting about 15 to 20 million bpd of crude supplies. For the week ending May 8, we got a much larger drop in domestic demand than we imagined. The Energy Information Administration (EIA) reported that U.S. propane domestic demand dropped by 738,000 bpd to just 432,000 bpd.

Chart 1 not only shows the drop, but it also shows the recent extreme volatility in domestic demand. In general, the domestic demand number is volatile. Remember, domestic demand is a calculated number. The EIA gets information on propane exports, imports, production and inventory changes, and then calculates U.S. domestic demand based on those other inputs. If any of the other four inputs are off, it can skew that domestic demand number such that it isn’t really a reflection of what happened each week.

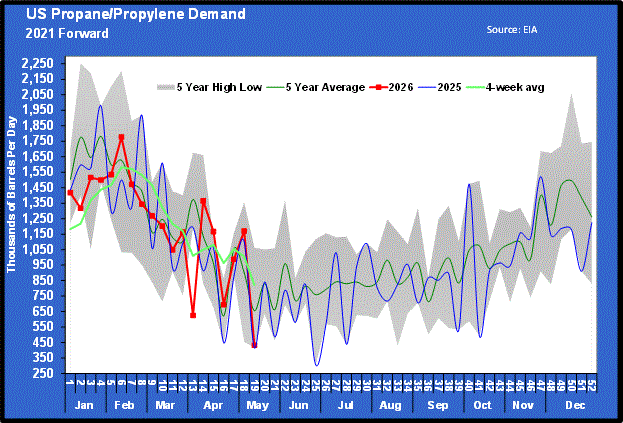

Sometimes it is best to look at a longer period to take out the weekly volatility. In chart 2, we are adding the four-week average.

Based on the four-week average, domestic demand was 821,000 bpd. That is much closer to the 800,000-bpd average we are predicting through the end of September, when we argued that inventory builds would resume. There may still be weekly volatility, but we still have high hopes that domestic demand will run around 800,000 bpd over the course of the summer, allowing inventories to build.

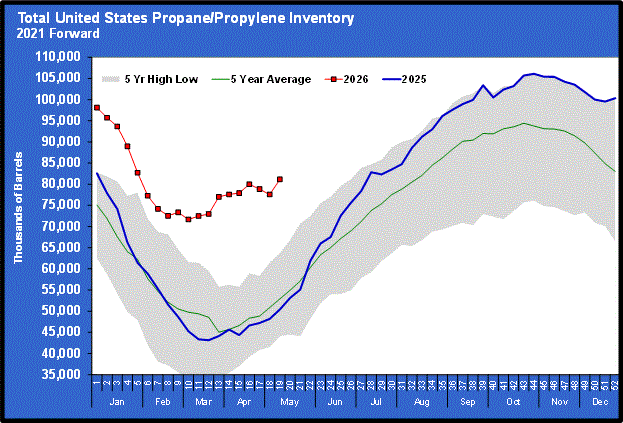

The massive drop in domestic demand this past week, along with an uptick in propane production and imports, allowed total U.S. propane inventories to increase 3.590 million barrels.

The build offset the draws over the last two weeks and got the inventory build trendline back to a more normal trajectory. That was a great relief.

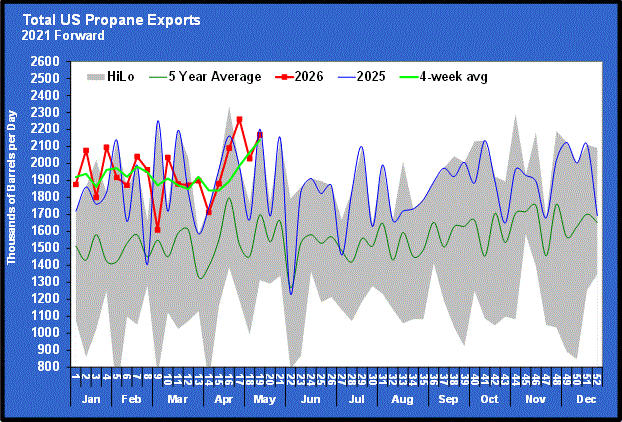

However, we need to be prepared for the build trendline to be shallower than last year, as long as export demand remains high due to the closure of the Strait of Hormuz.

We added the four-week average line to the export chart as well. It highlights that buyers took a while to respond to the Strait of Hormuz being closed, but now they are pulling hard from the United States, which is going to limit inventory gains going forward.

Currently, U.S. propane inventories are at 81.146 million barrels. That puts them 30.722 million barrels – or 60.9 percent – above last year, and 53.52 percent above the five-year average. But don’t be surprised if that excess above last year is given up as the summer progresses.

In fact, if the war continues, watch for this year’s inventories to eventually slip below last year’s and be closer to the five-year average by the start of winter. While that would still be plenty of inventory to meet the increase in demand this winter, it will no doubt result in a firmer pricing environment for propane that would be necessary to back off exports.

Buyers of all energy are certainly hoping for an end to the war and for energy supplies to return to normal. Even if that happens soon, it is going to take a while to replenish crude inventories globally. That is going to keep crude prices elevated and above where they were before the war started – probably well into 2027.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Industry leaders reflect on America’s 250th

Jul 3, 2026 -

Crude still not out of the woods

Jun 29, 2026

About the Author: Chris Markham

Chris Markham is the managing editor of LP Gas Magazine. Contact him at cmarkham@northcoastmedia.net or 216-363-7920.

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.