Global LPG supply flows change dramatically

Trader’s Corner, a weekly partnership with Cost Management Solutions (CMS), analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, covers the U.S.-Iran war’s impacts on the flows of liquefied petroleum gas.

Catch up on last week’s Trader’s Corner here: Much-needed propane inventory build

The last few Trader’s Corners have been focused on the impact of the U.S.-Iran war on U.S. propane. The United States is oversupplied with propane. Before the war began, U.S. propane inventories were at record highs coming out of a winter period. Exports were not particularly strong. Given the starting point for the inventory build period, it was almost certain that propane inventories would eclipse the record high of 106 million barrels from last year by the time this coming winter begins.

That prospect had propane priced extremely low in an attempt to encourage more exports. With crude prices dropping below $60 per barrel and propane oversupplied, U.S. retailers and consumers were enjoying very low propane prices. Crude started moving up in the lead-up to the war. Two weeks before the war started, WTI traded at $62.89. MB ETR propane was at 63.125 cents per gallon and Conway at 60 cents per gallon. Keep in mind, this was in the middle of February, not far removed from a major winter storm. On the same date the year before, propane was at 92 cents.

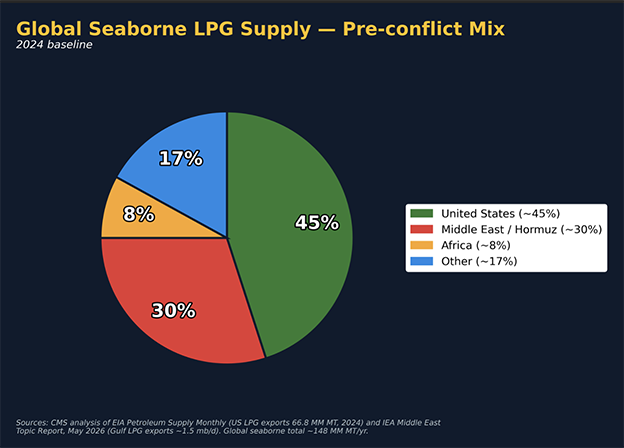

It took a while for the world to react to the upset of normal energy supply flows. But now they have, and ships in greater numbers are showing up on U.S. shores to load with U.S. propane, butane and ethane at an increased rate. The chart shows the liquefied petroleum gas (LPG) export share by country of origin before the war began. LPG is a combination of propane and butane, with a ratio of 80 percent propane to 20 percent butane.

As you can see from the 2024 data, the United States shipped 45 percent of the seaborne LPG supply globally. The Middle East provided 30 percent.

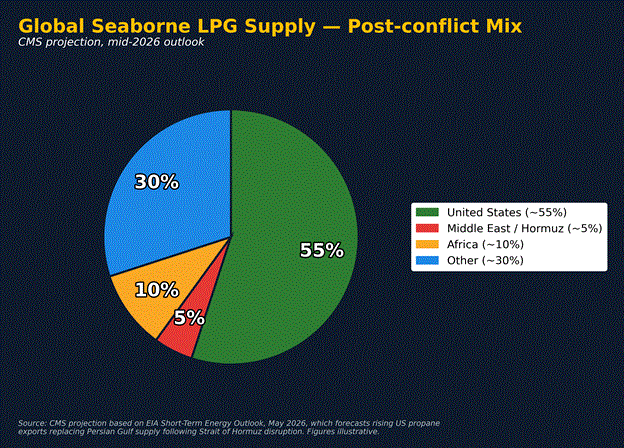

Chart 2 uses some estimates to adjust flows based on developments since the war.

With the Strait of Hormuz closed and few alternatives for moving LPG out of the Middle East, its portion of global seaborne exports is likely down to just 5 percent. All other areas have taken up some of the slack, but a good portion of what was lost from the Middle East is now being supplied by the United States.

The loss of supply from Qatar has been particularly hard to offset. Its exports represented about 8 percent of the global supply. What is more, its facilities that process the LPG have been attacked during the war. Even when the Strait of Hormuz reopens, Qatar’s LPG exports will remain below normal.

As we said at the start, it took the world a while to react to the realities of the war on the global LPG movement, but now that it has, the impact on U.S. supply and demand is significant.

The Energy Information Administration (EIA) data has been all over the place in recent weeks, with large draws on inventory for a couple of weeks, amounting to a draw on inventories of 2.5 million barrels and then a build of nearly 3.6 million barrels for the week ending May 8. We think the data just released for the week ending May 15 is likely a reasonable reflection of how the supply/demand balance might average out over the summer. The EIA reported an inventory build of 421,000 for the week, or about 60,000 barrels per day (bpd).

Obviously, that pace of inventory build would leave them well below last year’s 106 million start-of-winter level. Our original estimate was for a start-of-winter inventory position of around 92 million barrels. Inventories would be even less if last week’s numbers were to hold true.

What was even more concerning was the commentary from a trader last week regarding a change that could significantly increase export rates. The comments were that owners of flex exporting facilities were going to start exporting propane. Flex export facilities are ones that can export propane, butane and ethane. Industry reports had indicated that flex facilities were booked long term to export ethane. Therefore, we did not include their capacity for export estimates.

We had only included 216,000 bpd of more propane export capacity online in the second half of this year. Just that capacity addition will make it hard for inventories to build once available. One of the flex facilities is already online. We are not sure how much propane it could export, but it would appear to be about 200,000 bpd. Another flex unit of about the same size is scheduled to come online later this year.

If that much additional capacity is dedicated to propane, the domestic supply situation could change dramatically. While U.S. propane production could increase to offset some of that increased export capacity, we doubt it could fully do so in the short term.

Obviously, this is a very fluid situation. The best case is for the war to end and the Strait of Hormuz to reopen to take some of the global demand for U.S. propane off the table. Either way, we are likely going to face a much tighter propane supply/demand situation in the United States than we could have even dreamed before the war began at the end of February.

So far, propane prices have not skyrocketed like crude and refined fuels prices have. But increased upward price pressure could certainly be on the horizon if the geopolitical situation does not change soon.

What makes this situation particularly difficult for propane buyers is that it is event driven. If the war between the United States and Iran ends, the supply situation would suddenly change, taking price pressure off propane and crude. That adds a lot of risk to any hedge position that a buyer might take. It makes taking long-term positions particularly risky since what has prices higher can quickly go away, so buyers should probably be focused on mitigating the risk of high prices for shorter durations.

At the same time, making any sales without the supply locked in to support it will be extremely risky as well. It is just not an environment to take on that kind of risk. If supplies remain disrupted moving into winter, the chances of a significant increase in both crude and propane prices are present.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Crude still not out of the woods

Jun 29, 2026 -

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.