Crude still not out of the woods

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, reexamines the state of crude oil pricing.

Catch up on last week’s Trader’s Corner here: The US, Iran and propane: A retrospective

In the June 2 Trader’s Corner, we looked at the state of U.S. crude supply. At that time, the Strait of Hormuz remained closed, and U.S. and global crude inventories were dropping fast. Things were getting critical before a memorandum of understanding between the United States and Iran – beginning a 60-day period in which the details of a long-term peace agreement could be negotiated – was implemented. The sides agreed that the Strait of Hormuz would reopen during this 60-day period. That development did not come a moment too soon.

We recently predicted that WTI crude’s price would level out at around $75 per barrel. Our logic for choosing that price as an anchor point is simple. Governments tend to get aggressive in filling strategic reserves below $70 per barrel. Commercial inventories that were depleted during the war need to be replenished first. By keeping WTI at around $75 per barrel, commercial inventories will be replenished without too much competition from governments, at which point, another leg lower to $70 will occur when the governments step up their buying.

Once commercial and strategic reserves are replenished, normal supply/demand balances will drive crude’s price, assuming geopolitical events do not complicate the matter again. But as we write, WTI crude just fell below $70 per barrel, well below our anticipated first anchor price of $75 per barrel.

This is a great development as the global economy could use a period of low energy prices to get back on its feet. Inflationary pressure continued to rise during the war, driven by the high price of energy. High energy prices were hurting economic activity, and that was starting to show up in weaker job numbers.

Why did the fall in WTI crude not stop at the $75 mark? Market exuberance, perhaps. It is not unusual for market momentum to carry prices beyond where they will likely settle over a longer period. Those who were long on crude must sell crude to close their positions. Geopolitical developments are driving those traders who are long crude to trim positions. However, we still believe this overshoot is a time to enjoy but not get used to for long.

Another factor is the sudden surge in supply that is occurring. We must remember that producer storage was full and tankers were filled and ready to move as soon as the Strait of Hormuz opened. We must also consider that many sellers are hurting for revenue and are being aggressive in selling their barrels in a market that is temporarily oversupplied. But this situation will not last for long.

In its place will be a negative factor of the war on supply that will be longer in nature. Many crude wells around the world were shut during the war, and some of those wells will never return to production or will return with a lower rate of production.

When a crude well is flowing, it can have water and sand from the formation moving up thousands of feet of vertical production pipe with it to the surface. Once the flow stops, the water and sand begin to settle in the production pipe. This creates a lot of weight that the pressure in the formation may not be able to overcome to get the mass moving again. In the oil industry, these wells are termed sanded or watered up. Some may be able to be restored to production, but the process can take some time and is, of course, expensive. Wells that were near the end of their life may be abandoned for economic reasons. Drilling new wells to replace them will take time and money.

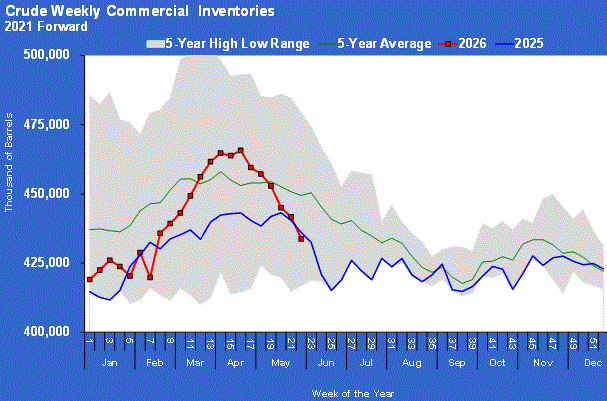

At some point, traders are going to start looking at the realities of crude inventories and reserves as the exuberance of the war’s end fades. When they do, they are going to find some ugly situations. The state of crude inventories at the U.S. trading hub of Cushing, Oklahoma, is an excellent case in point.

Crude inventories at Cushing have now fallen below what is widely said to be their minimal operational level. What that means is that the hub may not be able to perform properly. There are numerous negatives to this development, which have the potential to put upward pressure on WTI crude’s price.

There is a lot of sludge at the bottom of crude tanks, so much of what may be left in the storage tanks at current levels may not be movable or marketable. Cushing is at a point where it may not be able to deliver crude to refineries that depend on it for supply. So, the situation at Cushing is a great example of why commercial inventories must be restored before strategic reserves and why commercial players will bid up crude’s price to get what they need to operate.

We must also consider that there is fuel for a rally in crude’s price waiting in the wings. When the U.S.-Iran war drove crude prices to $100 per barrel, there were traders who took short positions. In other words, they committed to delivering crude in the future that they did not yet own. They were gambling that prices would fall and they would be able to secure the crude they needed to fulfill their obligations at a much lower price, thus making a large profit.

In the last few weeks, prices have gone in the direction of those short crude. To close their short positions, they must buy crude. With the gains that are already present for those short crude, given the recent pullback in prices, the pressure to take profits is very high. It won’t take much to trigger a round of short covering that will drive crude prices up, especially given the tightness in commercial supplies that the situation at Cushing represents.

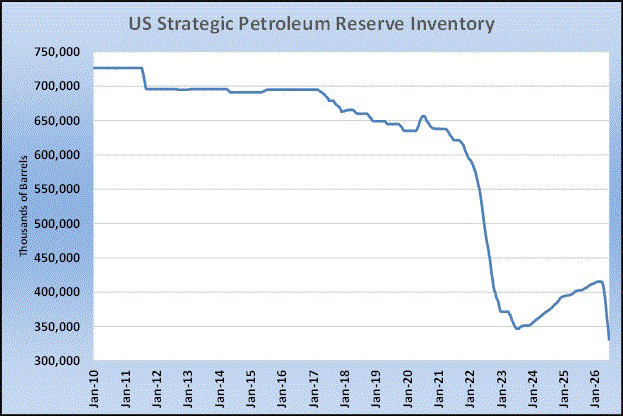

Once the commercial supply situation is restored and functional, only half the battle will have been won. The situation with U.S. strategic reserves has only gotten worse since we reported on them at the first of the month.

U.S. strategic reserves have fallen by another 25.928 million barrels this month. All the gains in restoring the reserve in the early part of the Trump administration have now been given back. Commercial players that borrowed from the reserve during the war will have to pay it back plus a premium. But they have limited time to return the barrels, so not only will they be supplying their ongoing commercial operations, they will be diverting any excess to the SPR. That is more potential upward pressure on prices.

While our $75 per barrel anchor price for WTI crude looks iffy right now, we still have reasonable confidence it will prove accurate given the supports mentioned above and others. If the $75 price until commercial inventories are restored and the subsequent $70 price until strategic reserves are refilled turns out to be too high, we will happily admit we were too pessimistic and rejoice, given the good it will do the global economy. Unfortunately, it is still too early to make that admission, though we still hope to be proven wrong.

Charts courtesy of Cost Management Solutions.

To subscribe to LP Gas’ weekly Trader’s Corner e-newsletter, click here.

You May Also Like

-

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026 -

Iran peace deal’s impact on propane markets

Jun 15, 2026 -

How the US-Iran war draws on propane inventory

Jun 8, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.