Analyzing U.S. propane production, supply trends

This past week, we got an email from one of our clients expressing confusion about U.S. propane production. It did not make sense to him why, with oil and gas production lower, propane supply was running higher than last year.

On Wednesday, right after the Energy Information Administration (EIA) releases its Weekly Petroleum Status Report, we provide our daily readers with a summary of the EIA data. Last week, the EIA data showed U.S. propane production running 113,000 bpd higher than the same week last year at 2.197 million bpd. Knowing that oil and gas production was down, that just didn’t feel right to our client – and we certainly understood why.

Let’s make sure everyone is on the same page before sharing what we told our client. There is no such thing as a well that is drilled to produce propane. Propane is produced as part of an amalgamation of hydrocarbons that formed under the earth’s surface due to heat, pressure and time. Oil and gas production companies are in the business of finding hydrocarbons and bringing them to the surface so we can use the energy trapped in the chemical bonds of those hydrocarbons.

There are many different hydrocarbons that have a range of specific gravities or weights. Hydrocarbon production wells fall into two broad categories: crude and natural gas. A crude well produces predominantly heavier hydrocarbons, and natural gas wells produce primarily light hydrocarbons. Propane is on the lighter end of the hydrocarbon spectrum, so naturally a lot of propane is produced in natural gas wells. But crude wells also have lighter hydrocarbons in them, including propane. When crude wells are produced, the hydrocarbons are passed through a separator that provides a rough separation of the very lightest hydrocarbons from the heavier hydrocarbons. This lighter mix from the separator would be very similar to what is produced in a “natural gas” well. The light hydrocarbons from the rough separation are then usually combined with hydrocarbons from natural gas wells. The combination is then sent to natural gas processing plants that separates methane, the lightest hydrocarbon, from the group. The methane is then sold to natural gas utility companies.

The remaining hydrocarbons that include propane are then sent to storage locations. The combined hydrocarbons mix is called Y-grade. There are fractionation plants built around these storage facilities like Mont Belvieu and Conway. The fractionators separate the Y-grade into the fungible natural gas liquids composed mostly of ethane, propane, butanes and natural gasoline. The natural gas liquids remain under pressure during the process, keeping them in liquid form.

The ethane is used by petrochemical companies, and the propane is used by petrochemicals and end-use consumers. Butanes and natural gasolines are generally sold to refiners as blending agents in the manufacture of refined fuels. Some are used by petrochemicals. This entire natural gas liquids process yields 85 percent of U.S. propane supply.

After the rough separation in the field, the heavy hydrocarbons, or crude, is pumped to storage locations that have atmospheric tanks that hold it until it is sent through a refining process that yields fungible refined fuels such as gasoline, heating oil, kerosene and other products. Propane that was locked in the heavier crude is released during the refining process as a gas, captured, pressurized to return it to liquid form and usually put into local storage tanks at the refinery for sale into the immediate market. Some of it is shipped to storage locations. Fifteen percent of U.S. propane supply comes as a byproduct of the refining process.

In summary, propane supply comes as a result of crude and natural gas production. On Tuesday’s and Wednesday’s daily reports, we provide our readers with data on crude and natural gas production, drilling activity, refinery throughput, etc. Basically, any data point that could give an indication of domestic propane supply is covered. Now on to our client’s confusion.

Our client is seeing all of this data, which is down considerably. For example, U.S. crude production is running 1.2 million barrels below last year at this time and 2 million bpd below its peak. Refinery throughput of crude is 2.61 million bpd below where it was at this point last year. The most recent official natural gas production came in July, which showed production down 5.4 percent from the December peak. Yet we are reporting propane supply higher than last year, and our reader is wondering how this can be with all sources of propane lower than last year.

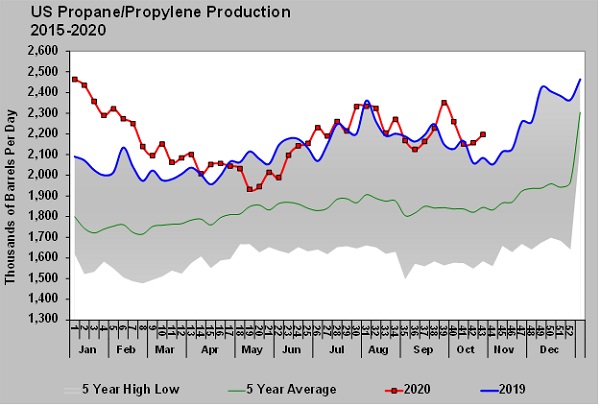

Chart: Cost Management Solutions. Click to expand.

The chart above helps explain. Note the blue line, which represents 2019, in November and December. Much of the growth in propane supply occurred toward the end of last year. There was also a dip in propane production during the fall of last year. If production continues along the current trend, in a few weeks, we will likely be reporting propane production lower than a year ago.

What is more important in terms of understanding the impact on propane supply from the reduction in crude and natural gas supply is to look at where propane production was at its peak. Propane production peaked during the first week of the year, setting an all-time high at 2.464 million bpd. Last week’s production was 267,000 bpd below that mark at 2.197 million barrels.

That is a tremendous amount of decrease in supply. On average this year, domestic propane demand is running 42,000 bpd higher than last year and exports are up 51,000 bpd – a 93,000-bpd increase in total demand. Production is up 70,000 bpd, but imports have been down 26,000 bpd. That is just an increase of 44,000 bpd in supply. Demand has outstripped supply by 49,000 bpd so far this year.

That has kept inventories from building as much as they could have. At the beginning of the year, inventory was 19 million barrels more than the previous year. Now, it is just 3.6 million barrels more than the previous year. These are weekly estimates; the official data lags by three months. But the result is somewhere between a 13- and 15-million-barrel decrease in the year-over-year inventory overhang.

Since propane is going into its higher demand period but crude demand is threatened by COVID-19 shutdowns, the market has been improving propane’s relative value to WTI crude. Mont Belvieu LST was at around 30 percent of WTI at the start of the year and is currently valued at 63 percent. That is simply a reflection, despite high current inventory, that market participants see propane fundamentals as more supportive than crude’s fundamentals.

Our client was right on the money questioning why current production is not below last year. Hopefully, this analysis shows that what he felt should be occurring is indeed actually happening. Propane supply has decreased from its peak more than propane demand has decreased this year. The result has been a slower build in inventory this summer that was indicated at the start of the year. That has reduced the inventory excess, resulting in more support for propane prices than the current inventory number might suggest.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026 -

Iran peace deal’s impact on propane markets

Jun 15, 2026 -

How the US-Iran war draws on propane inventory

Jun 8, 2026

About the Author: Kelly Limpert

Kelly Limpert was a digital media content producer at LP Gas.

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.