Expectations for propane pricing relative to crude

Chart: Cost Management Solutions. Click to enlarge.

In today’s Trader’s Corner, we are going to look at the relationship between propane and crude. Then, we are going to explore what we should all be expecting concerning the price of crude. The value of crude sets the base value for the overall energy complex. From that base, propane values will move in relative value to crude based on its own fundamentals – things like propane supply and demand.

We often use the analogy that crude is like a fighter jet and propane a rocket under the wing of that jet. The fighter jet changes altitude, and since the rocket is attached under the wing, it moves up or down with the jet. If the jet climbs 10 percent, the rocket climbs 10 percent.

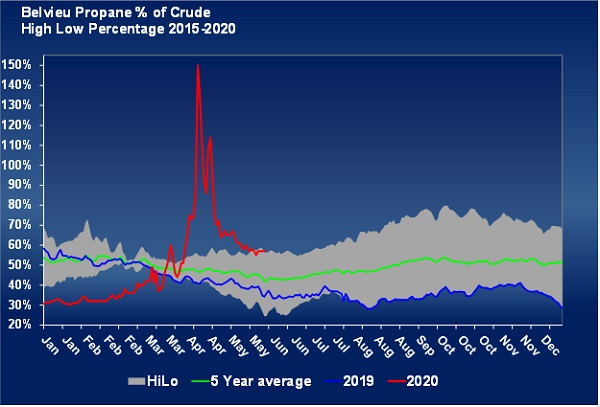

Sometimes the rocket is fired and uses its own propulsion to send it away from the jet. Sometimes the rocket climbs in elevation to the jet and sometimes it falls. Let’s look at a chart that we could say measures the altitude of the rocket relative to the jet.

The rocket has spent a lot of time detached from the jet recently. We see that at the beginning of the year, it was traveling at lower altitude and then climbed rapidly and has now fallen some but is still at a higher-than-average elevation to the jet.

At the beginning of the year, propane was setting new five-year lows in relative value to crude. Too much production and not enough demand pushed propane values down relative to crude. Then, propane’s fundamental picture improved, pushing it up some. When the impacts of COVID-19 hit, crude fell sharply, but propane held up based on its strong relative fundamentals, causing a spike in the relative value between propane and crude.

That massive separation is in the rearview mirror now, but propane is still near five-year high marks relative to West Texas Intermediate (WTI). As we have discussed ad nauseam in Trader’s Corner recently, declining natural gas and crude production has greatly slowed the rapid growth in propane supply that had been occurring over the last two years. In fact, over the last six weeks, domestic propane production has been less than it was during the same weeks last year.

Chart: Cost Management Solutions. Click to enlarge.

Propane inventory was 30 percent higher than 2019 when this year started, and now it is just 6.2 percent higher than 2019. Meanwhile, crude’s inventory is high, and its supply continues to outpace its demand. That is why propane is staying at a high value relative to crude; its current fundamentals are stronger than crude’s current fundamentals.

Still, the guidance system inside the jet is going to have some say in the rocket’s trajectory; crude’s value is still going to have some bearing on propane’s value. It behooves any propane retailer to consider the price direction of crude in order to get a better feel for the trajectory of propane prices.

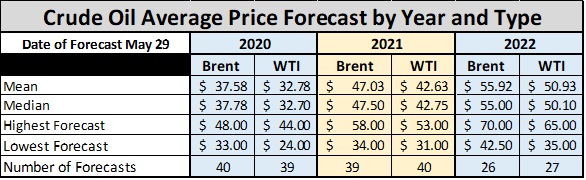

The table above shows the most recent price forecast from analysts at major trading companies for Brent and WTI for this year, 2021 and 2022. If we focus on WTI crude, it is already above expectations. In fact, even with the COVID-19 dip, WTI crude has averaged $36.51 this year. We expect these forecasts will be going up next month.

However, we believe the upside potential for WTI crude is limited in the near term. WTI crude dropped to negative $37.63 on April 20. It is now at $39.37. Even if we discount that one-day collapse as an anomaly, the price the day before was $18.27, and the day after was $10.01. There has already been remarkable gains in crude’s value. WTI is approaching $40 in the front month, and the November and forward crude contracts are already above that mark.

A group of producers called OPEC+ has cut 9.7 million barrels per day (bpd) from its baseline production to help support crude prices. U.S. producers have cut at least 1.9 million barrels from production. Other non-OPEC producers have cut production. Just the province of Alberta in Canada alone has cut about a million bpd. Some high-cost producers in the United States are already starting to open up production even before it reaches their breakeven because they need the cash.

There isn’t much OPEC+ can do to stop this production coming back on stream. As it does, it will limit the upside for crude’s price. However, at these prices it is unlikely that producers will start drilling again. OPEC+ is going to want to keep it that way. U.S. shale producers break even at between $40 and $46 crude. Prices will need to get above that level to prompt more drilling. OPEC+ is going to want to keep prices below that point until all of its shut production is back on. It doesn’t want the price to reach a point that prompts U.S. drilling until it is essentially producing all it can.

Demand is slowly ramping up from COVID-19. There is a lot of crude and refined fuel inventories that need to be used up. As inventories are used up and demand continues to rise, then OPEC+ will start putting more of its shut production into the market. We believe it is only when all of this production is back online that there is potential for a significant increase in crude’s price.

We believe WTI crude is going to be limited to flying in the mid-40s range for a while as the process unfolds. While there is a little more upside potential for crude, we believe the upward pressure that it applies to propane prices will be limited for a while. That means most of the upside pressure on propane is going to come from its own fundamentals.

You May Also Like

-

Unexpected rise in US propane inventories

Aug 3, 2026 -

Distillate prices becoming brutal

Jul 27, 2026 -

Aaron Huizenga on the power of self-awareness

Jul 19, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.