Exports, domestic demand adding current-price pressure

Propane prices have recently been on a surge. However, those increases in price have been contained to the front month. During January, propane prices increased 12.5 cents in Mont Belvieu and 11.69 cents in Conway. Despite this, propane prices for February and beyond did not go up as much as they did in January, creating an unusual price difference between the current, or front, month and the upcoming month.

February has become the front month, or cash market, and gets the headlines. However, propane buyers aren’t just interested in the current month. At the beginning of the day on Friday, Feb. 3, March Mont Belvieu propane was trading 15 cents less than February. A major pullback in propane prices occurred on Feb. 3 with a 5.63-cent drop in Mont Belvieu and a 6.5-cent drop in Conway. Since there was already a big discount for March barrels, not all of the pullback was felt in the further-out months. At the close of trading on Feb. 3, March Mont Belvieu propane was trading 13 cents below February and Conway was trading 12 cents below. Typically, that spread would be around a penny.

Click to view the full-size image

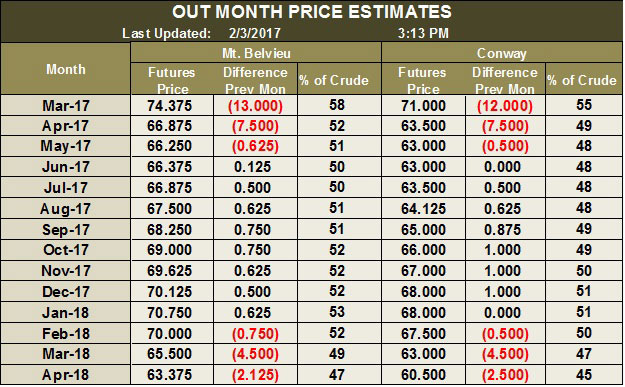

The table above shows the price of propane beyond February for both Mont Belvieu and Conway. The “Futures Price” column is an estimate of the price the market is valuing propane for a particular month. The “Difference Prev Mon” column is how much higher or lower that price is than the month that precedes it. The difference is called the spread, or the carrier.

If about a penny spread or less is normal, then why has such a huge spread developed between February and the further-out months? Strong exports and good domestic demand have been pulling propane inventory down sharply this winter. But traders see the price pressure being over soon. Sellers are using the current fundamental support to push the price of the February cash market higher. The perception that the supports will not last much longer and inventory draws will fall to normal or below normal is keeping prices beyond February in check, though we see some of the effects in the March price, as well.

Note the “% of Crude” column in the table. Beyond March, propane is trading at around 50 percent of the price of West Texas Intermediate (WTI) crude. Propane’s current fundamental support is not affecting prices that far out. The value of propane is simply being set relative to crude. All participants in the propane market say, based on all factors, propane should be valued around 50 percent of crude. The sum of the knowledge, beliefs and hunches of every propane buyer and seller results in that relative value being established for propane.

However, short-term fundamental tightness in the propane market is enabling sellers to currently get more for their propane than where the market is trying to set the longer-term value relationship between propane and crude.

Propane retailers are both short-term and long-term buyers. However, we often need to separate the evaluation of our purchases when tight propane fundamentals have caused the kinds of spreads currently being seen.

As long-term buyers, we are generally more focused on propane’s relative value to crude. The forward curve in the market, in its collective wisdom, says January 2018 Mont Belvieu propane is worth 53 percent of WTI crude. January 2017 propane traded around 60 percent. So, if we just look at where propane was trading in January 2017 or where it is now – around 68 percent – next January looks like a great deal. But we know that tight propane fundamentals pushed January 2017 and February 2017 up relative to crude.

If we go back to January 2015, when spreads were more normal, propane was trading at 48 percent of crude and January propane has averaged about 48 percent over the last five years. That comparison would make us think that January 2018 propane is not a good deal.

That is when we step back and ask ourselves if there is any reason propane should have gone up in value relative to crude between January 2016 and January 2018. We know the growth in propane supply has slowed and we know that the capacity to export propane has greatly increased. Those two reasons alone would be enough to justify why propane for January 2018 would be valued higher, relative to crude, than it was in January 2016.

Given the ability for the United States to now handle its propane supply through exports, a valuation of around 53 percent of crude is not bad. Before the shale gas revolution overwhelmed propane markets, propane routinely traded between 70 and 75 percent of crude. Propane is trading at a much higher relative value than it was back in 2015 when it fell to 25 percent.

When propane was trading at around 70 to 75 percent of crude, the United States was a net propane importer. When propane prices fell to 25 percent, it could not export enough propane. Now we have both abundant supply and the export capacity to balance the market. Propane is searching for a happy medium where the new normal should be. For now, the market has decided around 50 percent. This is a dynamic process, so to say “normal” is a bit misleading. Still, at this point, propane purchased for any out month at around 50 percent of WTI is probably a fair value.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Crude still not out of the woods

Jun 29, 2026 -

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026 -

Iran peace deal’s impact on propane markets

Jun 15, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.