Speculative bulls contribute to crude selloff

Since Feb. 23, West Texas Intermediate crude has been in a downward price trend. The downtrend began because traders worried that the production-cut agreement among 24 producing nations might not be enough to clean up excess crude supplies around the world.

Though the countries have done a better-than-expected job in keeping their commitments under the agreement, there have been some troubles. In total, parties in the agreement committed to taking just under 1.8 million barrels per day (bpd) of crude production off the market. In January, the compliance rate for the agreement was about 90 percent, by most estimates.

The problem was that Saudi Arabia was cutting more than it pledged to compensate for other countries that were falling short. Further, U.S. crude production was growing at a faster pace than anticipated, offsetting some of the potential price-supporting impact of the other producers’ efforts. The U.S. Energy Information Administration (EIA) increased its expectations for growth in U.S. crude production this year from 100,000 bpd to 300,000 bpd.

Last week, reports noted that Russia did not cut its production in February, leaving it at 11.11 million bpd. Russia had committed to cutting 300,000 bpd from its production, but so far it has only cut 100,000 bpd. That news caused a fairly sharp drop in crude’s prices, but they recovered rather quickly. From Feb. 24 through March 7, the concerns above resulted in a downtrend that was fairly measured and controlled. However, on March 8, the bottom dropped out of crude prices.

Crude prices fell more than 5 percent on that day and 7.3 percent over two days. It is still possible there is more of a decline to come. Prices fell immediately after EIA reported a build in U.S. crude inventory. It was the ninth week in a row that crude inventory had built, so why did this particular report result in such a sharp pullback?

The inventory build wasn’t really the reason that prices dropped so sharply. Yes, it was a reason for crude prices to go lower, but there was nothing unique about this inventory build that would suggest prices should react so dramatically. Instead, background maneuvering by speculative traders caused the sharp drop.

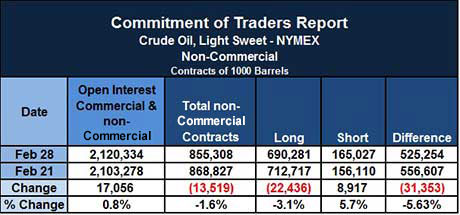

The table above shows the number of crude contracts (1,000 barrels per contract) held by non-commercial, or speculative, players during the weeks ending Feb. 21 and Feb. 28. On Feb. 28, 690,281 of the 855,308 contracts held by speculators were long positions betting on higher crude prices. Only 165,027 contracts were short positions, betting on lower prices.

Note that the net long position was already being reduced with traders cutting 22,436 long positions and adding 8,917 short positions from the Feb. 21 positions. So even before this selloff, there were chinks showing up in the belief in crude’s upside potential.

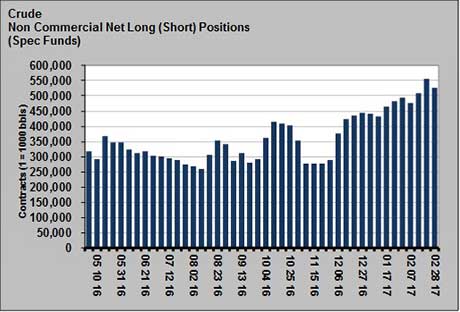

As the chart shows, traders had been steadily adding to the net long (more long positions than short positions) since December. In fact, they were holding a record net long position.

Imagine all of those long positions as a rubber band being stretched. It represents the potential downward velocity in the market. The more net long the market is, the more potential there is for a dramatic downward move in the market. When the market is as net long as it has been, traders are hypersensitive to any negative or bearish news.

Once the traders start selling to close their long positions, their activity begins to add downward weight to prices. This triggers more players to close their positions, generating more pressure to sell. The market becomes out of balance with many more sellers than buyers, and that results in the dramatic price declines, like those experienced over the last couple of days.

The inventory build may have been the catalyst that released the rubber band, but a market long on crude resulted in the high velocity of the downward move. Often, these selloffs will result in a market overcorrecting, which will eventually lead to opportunities for buyers to end the price decline. However, it is still undetermined if that price point has been reached. So far, buyers have stepped in when crude fell to its 200-day moving price average. The stability of that price point looks shaky at best.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Propane prices remain stable, relatively cheap

May 11, 2026 -

M&A momentum continues across the propane industry

May 11, 2026 -

Global demand increases for US propane exports

Apr 27, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.