Understanding the separation between crude and propane

Normally, there is a fairly close correlation between the price direction of propane and crude, but sometimes they can separate. As a propane buyer, it isn’t a bad idea to try and figure out why they separate since separations can be caused by fundamentals for propane either improving or getting worse.

Chart: Cost Management Solutions. Click to expand.

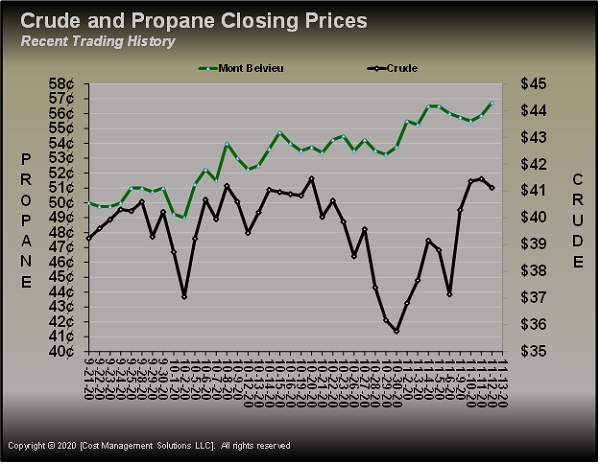

The chart to the right shows the price relationship between Mont Belvieu (MB) LST propane and West Texas Intermediate (WTI) crude. Note that from Sept. 21 until around Oct. 14, MB LST generally moved in the direction of crude.

From Oct. 15 through Oct. 30, WTI crude prices fell while MB LST resisted that fall, remaining in a very shallow uptrend. Rising COVID-19 cases, uncertainty about the U.S. election and a lack of progress by the U.S. Congress on a fiscal stimulus package to help offset the economic impacts of the COVID-19 shutdowns, among other factors, sent crude lower. Meanwhile, propane was supported by lower production, below-normal temperatures, crop drying and steady exports.

When crude prices finally bottomed out and started to rebound around the November election, propane initially started up with crude in the first week of November. However, over the last week, propane moved lower, even as crude posted a very strong run.

Chart: Cost Management Solutions. Click to expand.

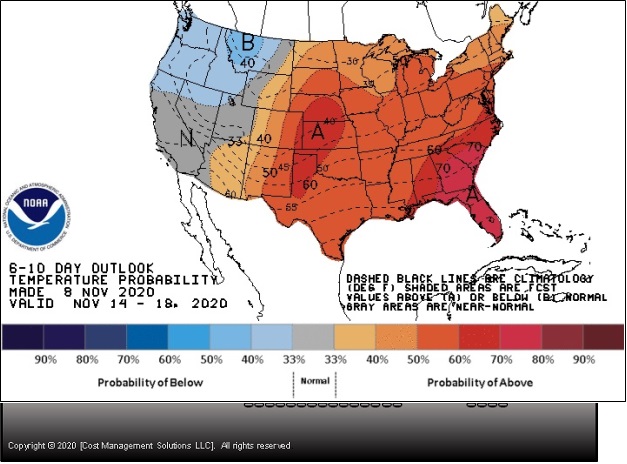

The lower propane prices can be attributed to a variety of factors. First, crop drying is finished, and temperature outlooks became much less supportive.

The chart to the right displays the temperature outlook from the National Oceanic and Atmospheric Administration (NOAA) on Nov. 8. The chart shows the probability that temperatures would be above or below normal from Nov. 14-18. Looking at the scale across the bottom reveals that the NOAA expected above-normal temperatures across most of the nation, especially the higher-consuming areas.

There was another, less obvious reason that propane prices softened up and did not follow crude at the beginning of the week. Traders were reporting a high degree of interest by propane producers to hedge their production. Propane retailers are familiar with hedging to protect against higher prices. It is done by buying prebuys or using financial tools like swaps or options. If propane retailers are really concerned about higher prices, their buying interest can drive propane prices higher. If the buying drives prices too high, the hedging interest eventually plays out and prices may flatten out or go lower for a period of time.

Producers have the opposite fear than propane retailers – that propane prices will fall, or they may simply be seeing an opportunity in the market. To hedge, they will sell their production at current prices, trying to avoid what they perceive as the potential for lower prices in the future or capture what they perceive is a good value for their production currently. If their selling interest is greater than buying interest, it can drive propane prices lower. If prices fall far enough, they will stop trying to aggressively sell their production. At that point, prices may flatten out or go up.

Chart: Cost Management Solutions. Click to expand.

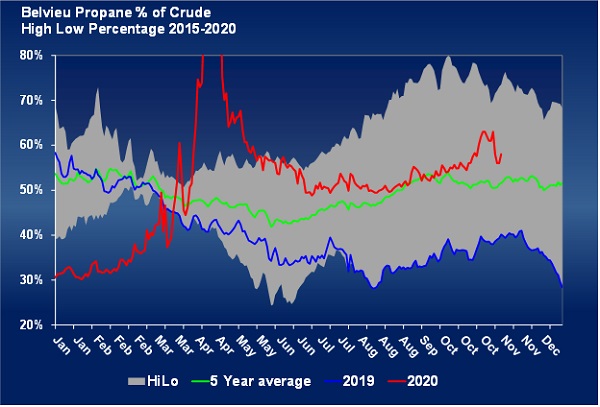

The important question is: Were producers seeing a major threat to propane prices in the future, or was some opportunity created? The chart will give us a clue.

The chart to the right plots MB LST propane’s relative value to WTI crude on a simple percentage basis. Note, we tightened the scale in the chart to eliminate an anomaly in April when crude price collapsed so the moves of the last few days would be easier to discern. On Oct. 20, MB LST was trading at 54 percent of the value of WTI crude. By Oct. 30, MB LST had surged to 63 percent of WTI as prices separated for the reasons mentioned above. A hydrocarbon producer looks at this improvement in propane’s relative value and sees an opportunity. Relative to other hydrocarbons, he may have to say propane’s value looks high. Producers wanted to capture this value, so they started to sell propane heavily. By Nov. 10, MB LST was back to 56 percent of WTI, producer hedging appeared to slow and propane prices moved higher even as crude prices slipped.

At this point, it appears that propane producers were interested sellers during a brief period because they saw an opportunity they wanted to capture. It appears less likely that it was because they saw a longer-term threat to propane prices.

The situation still should be monitored closely because, as we write, both propane and crude are moving lower, with propane outpacing crude to the downside. This could be an indication of more producer selling. If producer selling drives propane’s relative value to crude lower again – below 56 percent – it could mean they are seeing a greater potential for lower prices down the road. If that is the case, buyers need to take note. If producers are really eager to sell, it may be an indication to buyers that they should not be overly eager to buy.

There are threats to higher crude prices down the road that could drive propane prices higher. Right now, it looks like those threats become the greatest in the second half of next year. If the current eagerness to sell by producers drives propane prices down for next winter, it could be an opportunity for buyers. In summary, it is a time to be cautious about winter of 2020-21 buys, but look for opportunities that may be created for winter of 2021-22 buys if current selling pressure drives future months lower too.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Unexpected rise in US propane inventories

Aug 3, 2026 -

Distillate prices becoming brutal

Jul 27, 2026 -

Aaron Huizenga on the power of self-awareness

Jul 19, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.