Winter is coming: A look at propane inventory going into peak demand season

The Thanksgiving holiday marked the last potential break for most propane retailers for the winter. With the holiday over on Monday, it is now generally nonstop action for most retailers until Mother Nature decides winter is over. December through February is considered the core winter months and the highest demand period for propane. That makes it an appropriate time to take a close look at propane inventory to see where it stands heading into peak demand time. The latest data from the Energy Information Administration (EIA) was released on Nov. 25, reflecting where inventory stood on Nov. 20.

Chart: Cost Management Solutions. Click to expand.

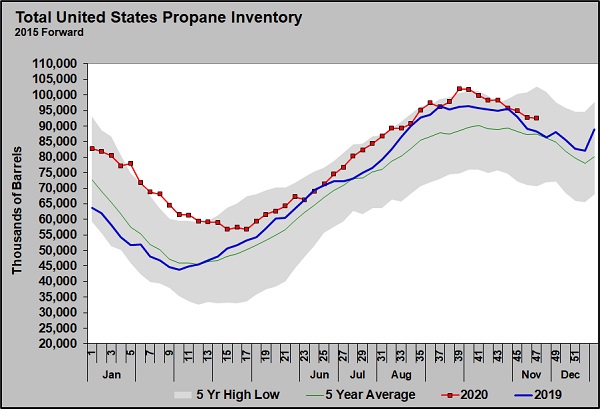

Total U.S. propane inventory stands at 92.562 million barrels. That is 4.241 million barrels, 4.8 percent, higher than last year and 6.1 percent higher than the five-year average. In its latest report, the EIA had inventory down just 325,000 barrels, much lighter than the 1.6 million barrels expected by industry analysts and well below the 954,000-barrel five-year average draw for week 46 of the year.

Inventory peaked at 101.842 million barrels in early October, falling 9.28 million barrels since then. The peak was about a million barrels under the 102.804 million-barrel record set in November 2015. At its current level, inventory is obviously in good shape ahead of the high-demand period, standing only below 2015 and 2016 inventory levels for this time of year – both of which were exceptionally high inventory years.

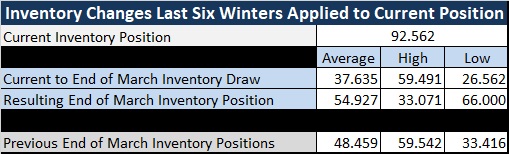

Propane exports were robust last week at 1.323 million bpd. If exports remain in that ballpark and domestic demand is strong through the rest of the winter, we could see an above-average draw on inventory. Since 2015, the average draw on inventory from now through the end of March has been 37.635 million barrels. The high has been 59.491 million barrels and the low 26.562 million barrels.

Chart: Cost Management Solutions. Click to expand.

The table to the right shows where inventory would stand at the end of March 2021 if inventory declines at its average, high and low posted case over the last six winters.

In the base (average) inventory draw case, it would be at 54.927 million barrels, comparing favorably to the average, high and low inventory positions set over the last six winters. We would think this would lend to a fairly stable pricing environment and likely keep propane averaging around 50 percent of West Texas Intermediate (WTI) crude.

In the bullish (high) inventory draw case, it would be at 33.071 million barrels, putting it below the low of the last six winters. In this case, we would expect propane’s relative value to WTI crude to rise.

In the bearish (low) inventory draw case, it would be at 66 million barrels, which is well above the high in the last six winters’ ending position. In this case, we would expect propane’s value relative to crude to drop.

Many traders are bullish crude for 2021, but most of the upward movement is expected in the second half of the year. We could see WTI crude stay under $50 per barrel through March since it will be beyond that date when COVID-19 vaccines will have the biggest impact on demand.

If we use $50 as the price of WTI crude through March, then the average inventory draw could keep Mont Belvieu LST propane capped around the 60-cents-per-gallon mark. If the bullish inventory draw case occurs and propane reaches 70 percent of crude, Mont Belvieu LST propane would yield around 83 cents per gallon. The bearish inventory case would likely drive propane’s value lower. At 40 percent of WTI crude, propane would be valued at around 47 cents.

These are not predictions, rather illustrations of plausible scenarios. There are plenty of other factors that could significantly change the price levels of both crude and propane.

The current bearish weather conditions and inventory levels make it feel like the only outcome is a bearish winter for propane prices. These illustrations, based on historical inventory changes, suggest there are scenarios still possible that could see a more bullish pricing environment. For that to occur, exports will have to remain robust and U.S. domestic demand will have to kick into high gear – and soon.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Propane retains good value as demand declines

Aug 10, 2026 -

Unexpected rise in US propane inventories

Aug 3, 2026 -

Distillate prices becoming brutal

Jul 27, 2026

About the Author: Kelly Limpert

Kelly Limpert was a digital media content producer at LP Gas.

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.