Bearish factors undermine propane’s value

Propane’s relative value to West Texas Intermediate (WTI) crude is already slightly below the low end of the range we expected for this summer.

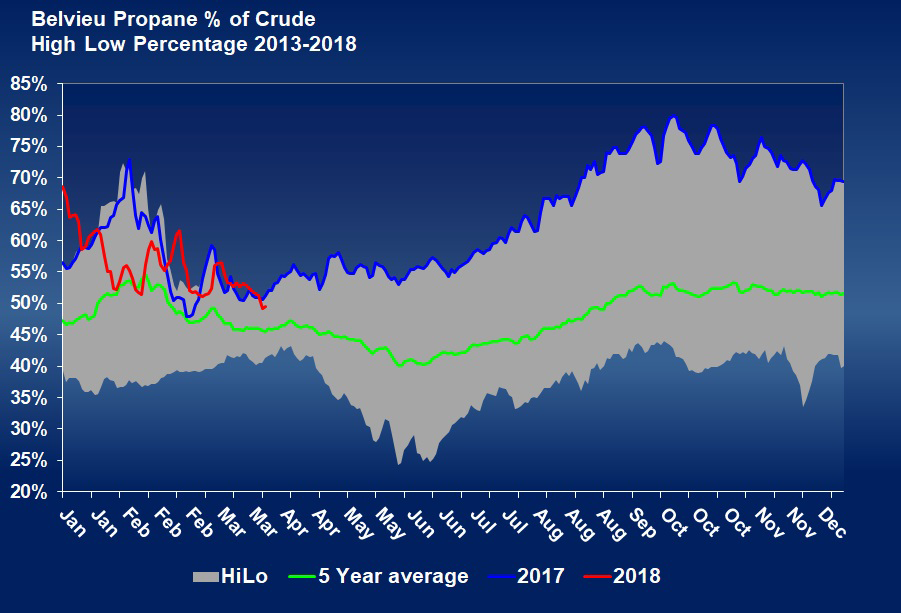

Click to enlarge.

This week, the value of Mont Belvieu LST propane fell to just 49 percent of WTI crude. Relative values have not been that low since February 2017. When those values bottomed out in 2017, there were around 50 million barrels of U.S. propane inventory on hand. Today, there are 36 million barrels of inventory available. Yet, Mont Belvieu propane is trading at slightly lower relative values than it was at this time last year.

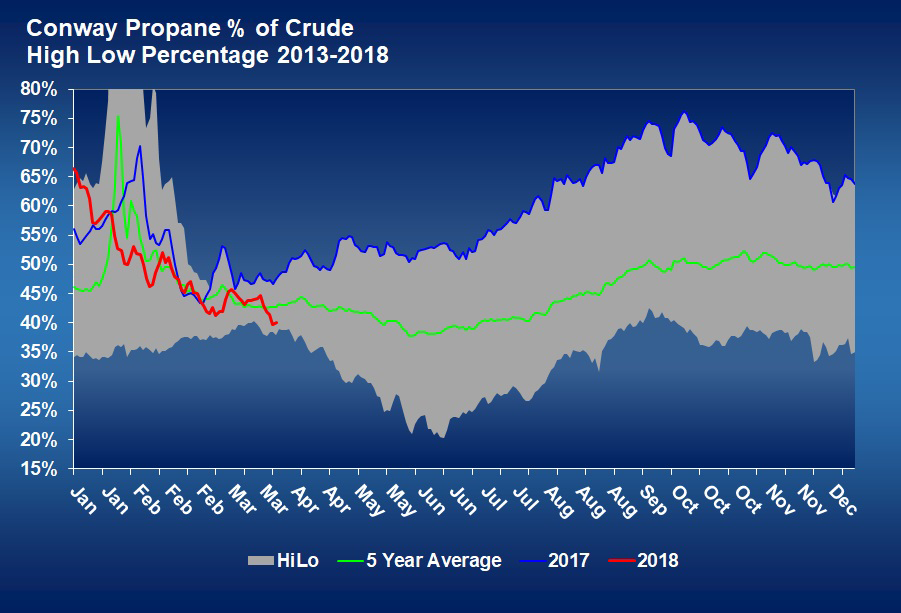

Relative values for Conway propane are well below where they were at this point last year.

Click to enlarge.

Conway is valued at just 40 percent of a barrel of WTI crude, putting it well below its five-year average and closing in on five-year lows. Conway has not been valued that low since early 2016.

The lower values are a significant change in the trend of the last two years, which saw propane’s relative value and actual value on an uptrend.

The change in the trend is the result of several factors. First, there was a significant surge in U.S. propane production at the end of last year that has carried into this year. The market has to absorb the new production.

Second, there was a drop off in export volume to close out 2017 that has continued into 2018. In the last few years, propane export capacity reached a level adequate to handle any excess U.S. propane production. Since then, there has been steady growth in U.S. exports during the winter months. Each winter month’s exports would be higher than the same month the previous year. But, from December 2017 through March 2018, exports were lower than the same months a year earlier. That trend change seems to indicate a general lack of demand for the new U.S. propane supplies resulting from a more balanced global supply-demand situation for natural gas liquids.

A third factor that could be depressing propane values is the delayed opening of the Mariner East 2 pipeline that will carry propane and ethane from the Marcellus and Utica shale plays to Marcus Hook, Pennsylvania, for export. We are confident the surge in supply was partly in expectation of this pipeline being available to the market. The line was supposed to be finished last year but has been delayed by regulatory issues.

The line is expected to be completed sometime this year, but the line’s owner is dealing with a regulatory delay. Additionally, the legacy Mariner East 1 pipeline has been down for a couple of weeks after sinkholes were found near the line’s path. The market just learned this week the line could be down another six weeks, as regulators are demanding even more testing.

Finally, the market is just learning that propane is on China’s list of imports that could receive a 25 percent tariff if China and the U.S. are not able to negotiate a trade agreement. So far, the tariffs have not been implemented and it may never come to that point. However, should they be implemented there could be downward pressure on propane prices as excess U.S. propane supply tries to access more costly markets.

The growth in propane supply should slow down this year. Exports could pick up if the global economy remains strong and a trade war doesn’t ensue. The Mariner East 1 pipeline will come back on line in six weeks and the pipeline expansions should be completed this year.

If some – or all – of that happens, propane could become well supported, causing nominal prices and relative values to start improving again. But, for now there appear to be numerous bearish factors at play that need to sort themselves out for propane values to improve significantly.

Graphs: Cost Management Solutions

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Aaron Huizenga on the power of self-awareness

Jul 19, 2026 -

Geopolitics send crude and propane prices higher

Jul 13, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.