Buying propane for winter 2021-22 might be a good value

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, examines why buying propane for next winter might be a good value.

Front-month (February) propane prices are much higher than market participants are used to seeing. Last year at this time, Mont Belvieu (MB) LST was trading at 37.75 cents and Conway at 33 cents. Last Thursday’s closes were 46.5 and 54 cents higher, respectively. MB LST was up 3 cents and Conway up 2 cents as we wrote last Friday.

If we can pluck good news from propane prices, it would be that next winter’s prices are much lower than the current prices. From October 2021 through March 2022, propane is averaging 72 cents at MB LST. The same strip at Conway is around 74 cents. That puts next winter MB LST 15.188 cents below current February prices and Conway 15.208 cents lower.

Since Oct. 1, 2020, MB LST has averaged 65.74 cents and Conway 64.25 cents. Currently, next winter’s propane is averaging about 7 to 9 cents higher than this winter’s average so far. With current prices high, buyers who pay for next winter now might find the price comparable to this winter’s average when the season is over at the end of March.

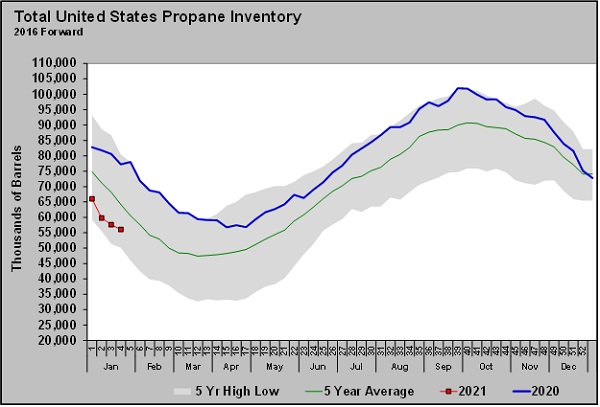

Chart: Cost Management Solutions

Given the changes in propane fundamentals, next winter’s price doesn’t feel out of line. Propane inventory is running at 21.923 million barrels, or 28.1 percent, lower than last year. Meanwhile, MB LST propane for next winter is only running 8 percent higher and Conway 12 percent higher than what they have averaged this winter.

The chart of U.S. propane inventory shows last year (blue line), the five-year average (green line) and this year (red line). Front-month propane prices are reflecting the lower inventory position this year, but so far, next winter’s prices have not responded as aggressively.

The chart below shows out-month propane prices from March 2021 through April 2022. MB LST March propane opened 2.25 cents below February last Friday morning, and the chart clearly shows the “backwardation” in prices through June. “Backwardation” is a term that traders use to describe a pricing environment where the current month is priced higher than the months that follow it. Prices then mostly flatten out through next January and then become “backwardated” again.

It is important to note that the out-month price table is not a prediction of where prices will trade in future months. It simply reflects where the market is valuing propane in those months currently. The buyer still must decide whether the fact that propane in the out months has not responded to the lower inventory position like the front month is a buy opportunity.

Chart 1: Cost Management Solutions

If a buyer believes the tighter inventory position is likely to persist into next winter, then next winter prices might look appealing. If a buyer disagrees with that view, then owning 72-cent propane for next winter probably doesn’t have much of an appeal. Sometimes, we don’t have any bias about where prices will be in the future. In that case, perhaps the best approach for a retailer is simply to consider if that price would likely put him in a competitive position.

If you ask a propane retailer where he believes propane prices at MB will be next winter, you might get an exasperated answer. But if you ask whether it would be competitive to own 72-cent propane at MB for next winter and build a retail price from there, he probably has a better idea. A retailer has a much better feel for what number worked in his market historically than where propane might trade at MB next winter.

Major commodities trading firms such as Goldman Sachs are predicting higher crude prices by next winter. Higher crude prices generally lead to higher values in the overall energy market.

Chart 2: Cost Management Solutions

Forty-one analysts responded to the latest survey for West Texas Intermediate (WTI) crude, yielding an average expected price of $51.42 for 2021. The survey was taken Jan. 29. WTI crude averaged $39.30 last year. That would be a year-over-year increase of 31 percent. In 2020, propane averaged 46.71 cents. If the forecasts on crude are correct and propane also gains 31 percent, it would yield an average propane price this year of 61.20 cents at MB.

Look at the 31 percent increase as just the base potential rise in energy prices this year. In addition, we must consider if propane fundamentals have changed. As we noted above, current propane inventory is 21.923 million barrels, or 28.1 percent, less than this time last year. Meanwhile, U.S. crude inventory is 40.650 million barrels, or 9.3 percent, more than this time last year. Using only the inventory metric, it is easy to see how changes in propane fundamentals between this year and last year could mean propane prices will continue to gain in relative value to WTI crude’s price.

In summary, the price of propane next winter is higher than we have come to expect recently. But the gain in next winter prices has been much less than front-month propane. Based on the expectation for higher crude prices and the tighter fundamentals expected for propane next winter, values do not appear out of line. If a retail price built around 72-cent MB or 74-cent Conway would historically work in your market, it might not be a bad idea to consider a first level of price protection for this coming winter. We would leave room to layer in more buys down the road since the summer doldrums are still ahead. It wouldn’t be unreasonable to expect front-month propane to fall as winter demand subsides, but if inventory remains comparatively low and crude prices are rising, that doesn’t necessarily mean winter values move lower with the front months.

Call Cost Management Solutions today for more information about how client services can enhance your business at 888-441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Unexpected rise in US propane inventories

Aug 3, 2026 -

Distillate prices becoming brutal

Jul 27, 2026 -

Aaron Huizenga on the power of self-awareness

Jul 19, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.