Export demands have slowed, but US inventories lack growth

Propane prices have been falling since mid-April as weakening export economics worry traders. Certainly, a crash of crude prices has been a key part of the weakness in propane prices. However, worries about exports have been in the background, causing propane to sometimes outpace crude to the downside.

Reports of export cargo cancellation have been rampant during the downtrend, and this week the fundamental data finally confirmed the rhetoric.

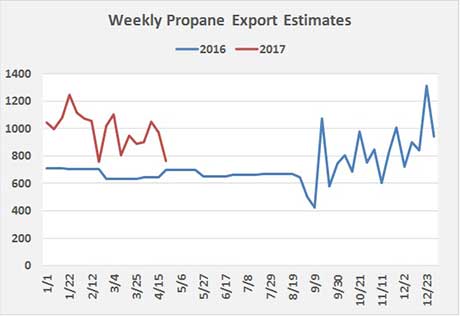

Note: EIA changed its method for collecting U.S. export volumes in September 2016, which is why there is more volatility revealed in the data than before that date.

In its Weekly Petroleum Status Report for the week ending April 28, the U.S. Energy Information Administration (EIA) estimated that the United States exported 764,000 barrels per day (bpd) of propane. This number was down 206,000 bpd from the previous week. In our outlooks, propane exports need to stay below the 775,000-bpd level for the remainder of the summer to have a good chance of building inventory to more than 80 million barrels by the start of next winter.

The decline in exports was certainly good news for the domestic propane market in the United States, but it didn’t do much for the inventory trend as domestic demand increased.

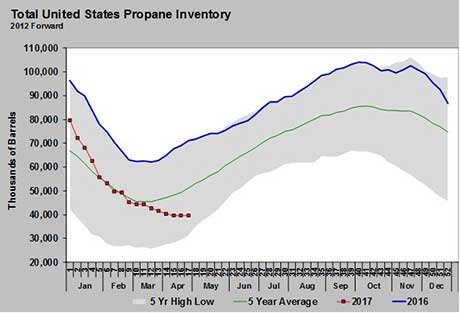

U.S. propane inventory built just 16,000 barrels last week, the 17th week of the year. Over the last five years, week 17 inventory has averaged a build of 1.894 million barrels. The light build puts that much more pressure in coming weeks to see well-above-average inventory builds if inventory is to reach comfortable levels for next winter.

Most estimates, including ours, have been for propane inventory to build to between 80 and 85 million barrels by the start of October. We are now seeing estimates of between 75 and 80 million barrels by that time. Keep in mind that inventories declined 64.357 million barrels between their peak in 2016 until they began building two weeks ago.

Inventory began the last two winters at well-above-average levels. Currently, fundamentals are on course to have inventory around the five-year average by the start of winter 2017-18. Unfortunately, that average does not reflect nearly the level of exports experienced over the last two years.

It is highly unlikely that the propane market will be comfortable with starting winter at 80 million barrels or less and maintaining price levels that would allow a 64-million-barrel drawdown in inventory, as that would put inventory well below anything seen in the last 12 years.

There seems to be only two possible scenarios, both with the same basis. Propane prices must increase this summer to push exports down even more so that inventory is at a more comfortable level at the beginning of the Northern Hemisphere winter. The second scenario is that prices will increase substantially during the winter to ration limited propane supplies between domestic and export demand.

Of the two scenarios, we would advocate the first as it has the best chance of keeping prices reasonable when U.S. markets will need the most propane supply. So far, we have been pleasantly surprised that propane prices have been able to fall and still result in export demand destruction. It would be fantastic for the domestic retail markets if that situation could be maintained.

However, we are skeptical that the pricing environment will remain so friendly as winter gets closer. U.S. inventory has built a grand total of 24,000 barrels since hitting its low three weeks ago. That is just not going to cut it. We need to see more, and we need to see it soon. U.S. domestic markets must hope the export demand destruction continues.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Crude still not out of the woods

Jun 29, 2026 -

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026 -

Iran peace deal’s impact on propane markets

Jun 15, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.