Gulf Coast propane inventory soars

In last week’s Trader’s Corner, we looked at the position of overall U.S. propane inventories. This week, we are going to drill down into the regional inventories to continue setting the stage for this year’s inventory-build period. Our focus will be on the two regions with the primary trading hubs: the Gulf Coast and the Midwest. Inventories in those regions are impactful on prices in other regions.

The inventory positions are going to reveal the pressure on producers to move production from the Midwest to the Gulf Coast. The Midwest is greatly oversupplied and landlocked, eliminating direct export options. It is also lacking in petrochemical demand compared to the Gulf Coast. The charts below show the results of moving product out of the Midwest to the Gulf Coast.

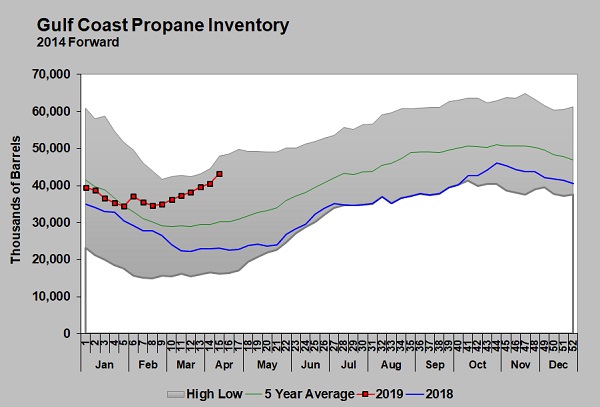

Click to enlarge. (Image: Cost Management Solutions)

As of the week ending April 12, Gulf Coast inventory stood at 43.181 million barrels. That is already 20.068 million barrels higher than this time last year.

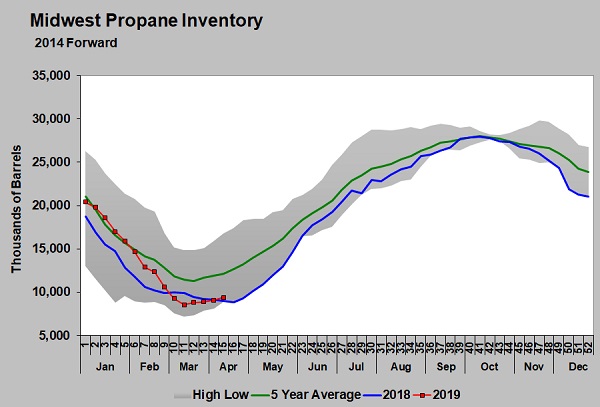

Click to enlarge. (Image: Cost Management Solutions)

Meanwhile, Midwest inventory is just 407,000 barrels higher than last year, at 8.973 million barrels. With so much production in the Midwest relative to demand potential, producers simply do not want to hold inventory there. The fact of the matter is that high production rates reduce the need for much of an inventory cushion.

Those buying supply related to Conway shouldn’t be too concerned about the current inventory level. Last winter had its high demand times in the Midwest that were navigated just fine with inventories near five-year lows. Conway trading 7.5 cents below Mont Belvieu despite the inventory discrepancy shows little worry about supply or inventory in the Midwest.

The relatively low values in the Midwest are reflecting the cost of moving production to the Gulf Coast. If producers believed there was a scenario where the supply would be needed in the Midwest, they would not be accepting 7.5 cents less for their propane.

It is our understanding that Canadian producers will continue to be aggressive in moving production into the U.S. Midwest in 2019. However, that could change in the coming years, which could raise Conway values relative to Mont Belvieu. Make no mistake, Canadian producers are looking for ways to improve netbacks on their propane over what they get when they send it to the U.S. Midwest. Some barrels are already going directly to the Gulf Coast and to Mexico. There has also been an export facility built on Canada’s west coast that is opening up Asian markets. Canadians are also keen on building up their own petrochemical industry to take advantage of the cheap feedstocks available. For now, it appears Canadian producers still need the U.S. Midwest market to manage their supply imbalance.

For U.S. producers, moving product from the Midwest directly to the U.S. East Coast for export out of Marcus Hook, Pennsylvania, has not lived up to its potential. The setbacks of the Mariner East system have been well documented. The Mariner East 2 expansion line finally became operational, at a reduced rate, after much delay. It is probably operating 100,000 barrels per day (bpd) below its 275,000-bpd capacity due to the necessity of using a smaller diameter section of existing line to address regulator issues.

Just as Mariner East 2 came online, the legacy 75,000-bpd Mariner East 1 line was shut after sinkholes developed near its route. This prompted the Pennsylvania Public Utilities Commission to require unprecedented levels of testing that could have the line down another three months at best. Some believe the line will never reopen since the Mariner East 2x is expected to be completed by the end of the year. The three-line system was expected to give producers in the Marcellus and Utica shale plays a much-needed option for moving ethane, propane and butane to the East Coast for export. So far, it just hasn’t panned out the way it was planned.

The battle for the hearts and minds of propane traders still looks to play out on the Gulf Coast. Right now, bears are on the offensive with inventories rising and already closing in on five-year highs. Production is simply overwhelming demand, leaving market bulls with little option but to pull back horns and give ground. U.S. producers continue to increase natural gas and crude production. Crude production brings with it associated natural gas and natural gas liquids. Of course, wells drilled specifically for the natural gas and natural gas liquids will provide the majority of the new supply. Expectations are for at least a 10 percent increase over last year.

This past week, the U.S. Energy Information Administration reported a propane export rate of 1.118 million bpd during the week ending April 12. It was the fourth week in a row, and the fifth out of the last six weeks, that exports have exceeded a million bpd, yet propane inventories on the Gulf Coast increased 2.664 million barrels. Over the last five years, Gulf Coast inventory had averaged an increase of just 639,000 barrels during week 15 of the year.

During the same six-week stretch last year, the United States exported 798,000 bpd of propane. The year-over-year increase was 247,000 bpd, yet inventory built at a pace that was more than four times the five-year average. Does that leave any doubt why propane bulls are on the defensive?

As we pointed out last week, there will be another 175,000 bpd of combined propane/butane export capacity completed on the U.S. Gulf Coast in Q3 of this year. Assuming the world wants the supply, and if and export economics remain as strong as they are right now, the inventory build should slow as a result of this capacity increase. But, by the time that capacity is up and running, having its full impact, winter will be upon us and the die may already be cast on the winter 2019-20 pricing environment.

The current pricing environment provides excellent values for hedging. Prices are low enough that consumers are likely to be happy with current offers on one-, two- and even three-year fixed-price deals. Propane retailers that aggressively push these deals will likely see good margins and happy customers regardless of how this year’s pricing environment ultimately plays out. However, it doesn’t appear to be a time to be aggressive on the speculative buying front. It is a dynamic market and situations may develop in the coming months where speculative buying of propane makes more sense. Modest amounts of speculative buying may still work to provide numbers to quote customers. But, being aggressive with speculative buying runs a lot of risk in this environment.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Aaron Huizenga on the power of self-awareness

Jul 19, 2026 -

Geopolitics send crude and propane prices higher

Jul 13, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.