How and when to use call options to manage propane supply price risk

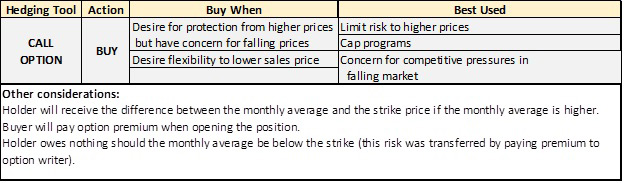

Today’s Trader’s Corner looks at one of the staples of managing propane supply price risk: call options. The table below is a quick reference tool retailers might find helpful in deciding if a call option is the right hedging tool to solve a propane supply risk issue.

If there was absolutely no doubt prices were going to rise, or if a retailer lived in a world where there were no competitors, there wouldn’t be much use for a call option. Instead, as propane supply price risk managers, propane retailers buy swaps and pre-buys to avoid paying the premium on options.

However, in the real world, there is always risk prices will fall. If prices are fixed to the customer based off of a pre-buy or swap buy, it doesn’t matter if prices fall. When propane consumers buy a fixed-price program, they are assuming the risk of falling prices. If prices fall, the retailer and the customer will not benefit because the swap buy or the pre-buy has a fixed supply cost. The customer will pay the agreed-upon price and the retailer will still make the same margin.

Some customers may not want to fix a price and give up the possible benefit of a falling market. They may want to cap a price instead. If retailers try to use pre-buys or swap buys to cover a cap program, they could get into real trouble if prices fall. They have promised to lower the customer’s price if prices fall, but their supply cost will remain the same based on the swap or the pre-buy.

A retailer can have upside price protection and transfer the risk of falling prices to a third party by buying a call option. A call option works just like a swap buy or a pre-buy in a rising market. In fact, if a retailer bought a call option or a swap, the strike price would be the same. Let’s say the strike for a Mont Belvieu call or swap is 53 cents for a December position. Then let’s say December comes and goes and the monthly average in Mont Belvieu was 60 cents. The retailer would receive the same 7-cent payment from a swap position or a call position.

It is when prices fall that the differences between a call option and a swap are realized. Let’s say the monthly average for December is 50 cents. In the case of a swap buy, a retailer must pay the 3-cent difference between the strike and the monthly average. In the case of the call, the retailer simply lets the option expire and owes no money.

The retailer has transferred the risk of falling prices to an option writer by paying a premium in advance to the option provider. Option premiums are not cheap, and their cost must be rolled into the price charged to a customer. So if a December call option premium is 10 cents, a cap program would be priced 10 cents higher than a fixed-price program that is backed up by a swap or pre-buy.

Call options are also useful as a speculative tool when there is a strong bias that prices are going higher but there remains a desire to be in the position to lower prices if prices fall instead.

A call option premium must be handled as a supply expense and rolled into a retailer’s supply cost, which will then be passed through to customers. A retailer that has used call options and has passed the cost through to customers can never be wrong about the market and will always make margin targets.

The issue is that the premium cost may make the retailer uncompetitive initially, making sales tough. A competitor not buying options could always be the cost of the option premium below a retailer that is using options to manage price risk. The competitor is assuming the risk to falling prices himself and not charging his customer to offset the risk. A competitor using swaps or pre-buys will be at a disadvantage in a sharply falling market and may need to take a hit to margin to remain competitive if sales prices have not been fixed.

Meanwhile, the option holder is able to lower sales prices and make the same margin because an option does not lock in the supply cost. The holder of an option is able to price based off of current market prices, which is a real advantage in a falling pricing environment. The option gives the holder the right to buy propane at a certain price. The holder will exercise that option if prices are higher than the strike price of the option. The holder will simply let the option expire without exercising it if market prices are below the strike.

In many cases, retailers that hold options find they make more money when they do not exercise the option since they tend to make more money overall in a falling price environment when they have not locked in supply costs.

For more Cost Management Solutions analysis of the energy market that helps propane retailers manage their supply sources and make informed purchasing decisions, visit www.lpgasmagazine.com/propane-price-insider/archives/.

You May Also Like

-

Crude still not out of the woods

Jun 29, 2026 -

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026 -

Iran peace deal’s impact on propane markets

Jun 15, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.