How lower crude production affects US propane supply

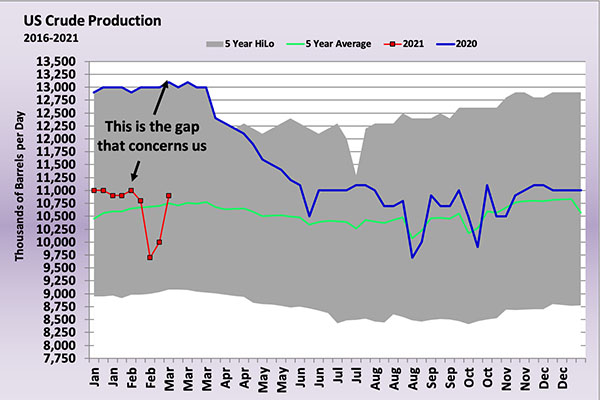

Trader’s Corner has been focused recently on the potential impacts of lower crude production on U.S. propane supply. U.S. crude production has been running 2 million barrels per day (bpd) less than this time last year when peak production of 13.1 million bpd was achieved.

Chart: Cost Management Solutions

Crude production plunged during the beginning of the COVID-19 pandemic when lockdowns started, negatively impacting refined fuels demand. Crude prices dropped during that time, but they have recovered and are higher than they were just before the pandemic. Yet, U.S. production is still running around 11 million bpd. It had dropped below that reduced rate during the recent winter storm but quickly recovered to the 11-million-bpd mark.

U.S. crude production companies are being forced to exercise capital discipline. Investors have been leaving the crude producers, especially those focused on shale formations, since before the pandemic. High capital spending requirements were not allowing them to give investors an adequate return.

Their lenders were also demanding they deleverage their balance sheets and pay down debt. When the pandemic hit and dropped crude prices, many companies went bankrupt, hurting lenders. At this point, there is little interest in investing in or lending to these producers. It is the need to maintain capital discipline by the players that survived the recent price collapse that is keeping U.S. crude production from recovering. Some believe U.S. crude production will never get back to 13.1 million bpd; others believe it will take many years.

Chart: Cost Management Solutions

Interestingly, the lower crude production should not impact the amount of propane coming from refineries. Last year, refineries provided just under 14 percent of U.S. propane supply. If the demand for refined fuels gets back to normal, refiners will simply import the crude needed to meet the demand, offsetting the loss in U.S. crude production. So crude production itself does not impact propane supplied by refiners. As long as refinery throughput returns to normal, U.S. propane supplied from refineries should return to normal as well.

Ironically, what gets impacted by lower domestic crude production is the amount of propane coming from natural gas processing. There are two types of hydrocarbon wells: crude and natural gas. Crude wells are drilled primarily to get heavier hydrocarbons that can be refined and turned into gasoline and distillates. But there are also natural gas and natural gas liquids (NGLs) that are produced with the heavier hydrocarbons. The lighter hydrocarbons produced in crude wells are known as associated production. The wells weren’t necessarily drilled for these lighter hydrocarbons, but they were produced alongside the production of the heavier hydrocarbons.

The associated natural gas and NGLs produced with crude wells is separated out and goes to natural gas processing. There, it may be combined with natural gas and NGLs that were produced in natural gas wells that are specifically drilled to get the lighter hydrocarbons. The combination of natural gas/NGL production associated with crude wells and that which comes from natural gas wells provides 86 percent of U.S. propane supply.

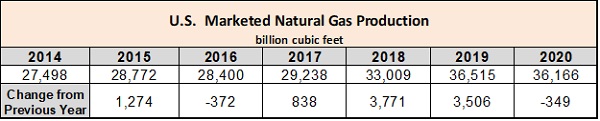

The table above shows how rapidly “natural gas” production increased in 2018 and 2019.

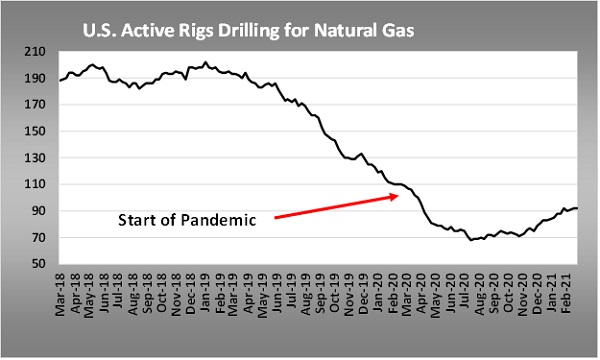

Now, take a close look at the chart below, as it is the crux of this analysis and our concern.

Chart: Cost Management Solutions

The chart shows the number of active rigs drilling specifically for lighter hydrocarbons. These are referred to as natural gas wells. Note how even before the pandemic the number of wells being drilled specifically for natural gas/NGLs was declining.

The reason was that so much natural gas and NGLs were being produced along with crude production that there was less need to drill specifically for lighter hydrocarbons. All of this associated production helped keep natural gas and NGL prices low.

If producers maintain capital discipline, thus reducing drilling for crude wells and keeping crude production lower, then natural gas and NGL production will be lower as well.

We believe very strongly that propane supply has overperformed natural gas and crude production over the past year because of a backlog of Y-grade or NGLs mix that accumulated in recent years. An expansion of fractionation capacity over the past couple of years has allowed more Y-grade to be processed, minimizing the impact of lost natural gas and crude production on NGL supplies.

Assuming this theory is correct, the backlog of Y-grade will eventually be eliminated. It will be at that point we will see the true impact of lower crude production on propane supply.

Propane retailers and their customers that benefit from keeping the upward pressure off propane prices need to be rooting for a couple of possibilities:

- Crude’s new higher price will allow crude producers to attract the investors and lenders needed to resume higher drilling activity and more crude production, which will yield the type of associated natural gas and NGL production seen before the pandemic.

- Producers drill for more wet (NGL-rich) “natural gas” wells to make up for the lost associated production from crude wells.

There are a couple of considerations with the second option:

- The same capital constraints may apply.

- The location of the production may shift away from the Southwest where much of the associated natural gas growth has occurred in recent years. The quest for NGL-rich natural gas wells may mean production shifts to other regions of the country, moving it away from where infrastructure exists to produce and process it.

There is little doubt that the economic and political environment is going to make it more difficult to return U.S. crude production to where it was before the pandemic. Consequently, it’s going to be equally difficult to maintain NGL production associated with crude production at current levels. This situation increases the potential for more upward pressure on U.S. propane prices.

Call Cost Management Solutions today for more information about how client services can enhance your business at 888-441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Aaron Huizenga on the power of self-awareness

Jul 19, 2026 -

Geopolitics send crude and propane prices higher

Jul 13, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.