More propane production from refineries ahead

U.S. refiners are beginning to come out of seasonal maintenance work, which could mean more propane supply for an already oversupplied market. As we mentioned last week in our discussion of what makes propane a particularly tough commodity to trade, refiners do not consider the value of propane in determining at what rate they will run their units.

Gasoline and distillate values are the primary drivers of the refiner’s decision concerning throughput, and propane is simply a byproduct of a process that is focused on those fuels. That means the production of propane from refiners is essentially inelastic, and high propane supplies/inventories will not prevent refiners from increasing propane supplies.

=

The chart above shows the percentage of total available refining capacity that is in use. Through most of the year refiners were running at exceptionally high utilization rates to take advantage of cheap crude and great refining margins created by high refined products demand. But refineries can only go so long without doing maintenance work.

Each year as refiners get ready to transition from summer to winter operating preferences, they may take the refinery down for a period of maintenance. That maintenance work is generally performed in August and September. Because refineries were operating at such high rates this summer, there was a greater-than-normal reduction in capacity utilization and thus a greater potential change in propane output when maintenance work began.

In a typical year, refinery utilization maxes out between 92 and 93 percent. This year, utilization averaged more than 95 percent in July. Yet, by the second week of October, refinery utilization was down to 86 percent, just slightly above the five-year average for that week of the year of 85.34 percent.

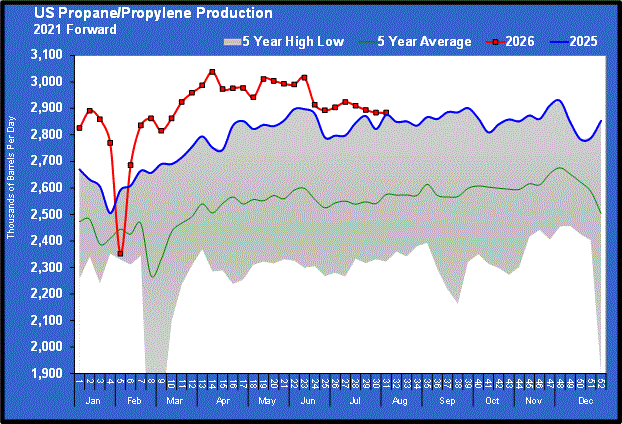

The chart above shows the decrease in propane/propylene production that occurred because of the heavy volume of maintenance work.

But, the first chart on utilization shows that refiners are beginning to come out of seasonal maintenance and the percentage of refinery capacity utilized is increasing. Last week’s propane production seems to already reflect the increased utilization rates with a 37,000-barrels-per-day (bpd) increase in propane production. Much of that increase appears to be from natural gas processing plants because the recent increase in refinery utilization would not generate that much propane. But we can assume propane supply from refineries contributed some to the increased propane supply. We can expect more propane supply from refiners before the end of the year.

In July, when capacity utilization was peaking, refineries were making 283,000 bpd of fuel-use propane and 298,000 bpd of propylene (only used by petrochemical companies). It is not inconceivable to see production rates near that point again by the end of the year. Over the last five years, fuel-use propane production from refineries in December has averaged 30,000 bpd higher than it did in October.

Propylene production is likely to increase by 24,000 bpd over the next two months as well, which could possibly lower the use of fuel-grade propane by petrochemicals. Even if we disregard the increase in propylene production, the uptick in fuel-use production alone will be enough to offset about a third of the 91,000-bpd increase in propane exports reported by the Energy Information Administration last week.

It appears propane markets found a lot of support in the increased exports reported last Wednesday, but we must remember there are a lot of moving parts in the propane supply/demand balance. It is often best not to overreact to a single input.

What we have to look for is significant and sustainable changes in the supply/demand balance, which will be necessary to pull down record-high inventory in propane. Changes that have the potential for doing that will change the propane pricing dynamic, thus changing a retailer’s supply risk management strategy.

Week in review

Crude prices made a surprising jump starting midweek, pulling propane prices along for the ride. Fundamentally, there seems to be little reason for the rally, and we would expect crude markets to calm down a bit after transitioning to the new month.

Propane is likely to stay fairly attached to the movement in crude prices with its value already relatively low compared to crude. However, domestic demand needs to pick up to help exports to deal with excessive inventory. We go into the week bearish on both crude and propane.

Last week’s highlights

- Monday: Conway propane led a retreat in propane prices as traders concerned themselves with light crop drying demand. Crude fell as Goldman Sachs warned that high refined products storage levels could put more downward price pressure on the energy complex.

- Tuesday: Weak fundamentals for both crude and propane had prices continuing in their downtrends. British Petroleum joined other oil majors in announcing more capital spending cuts, maintaining the bearish tone for crude markets.

- Wednesday: Recent losses in crude and propane values were swept away by a surprising surge in the price for both. Conway propane gained more than 9 percent in value despite the Energy Information Administration reporting a build in Midwest propane inventory and reports that the bulk of the U.S. corn crop has already been harvested. There was a major trade in crude that appeared to be computer driven and was the catalyst for the rally in crude. Propane was initially moving higher with crude, but Conway outgained crude on reports of short covering for Conway barrels.

- Thursday: Conway propane continued to outpace the general energy market in a continuation of Wednesday’s short covering. Conway propane gained more than 10 percent in two days despite bearish fundamentals. Crude managed a small gain despite a disappointing preliminary reading on U.S. third-quarter gross domestic product showing the economy grew at a lethargic 1.5 percent annualized rate.

- Friday: Propane prices continued to inch higher on the last trading day of the month. Crude was very volatile as it found enough technical buying support to keep prices from falling far, but weak fundamentals limited gains.

Cost Management Solutions LLC (CMS) is a firm dedicated to the analysis of the energy markets for the propane marketplace. Since we are not a supplier of propane, you can be assured our focus is to provide an unbiased analysis.

For more Cost Management Solutions analysis of the energy market that helps propane retailers manage their supply sources and make informed purchasing decisions, visit www.lpgasmagazine.com/propane-price-insider/archives/.

You May Also Like

-

Propane retains good value as demand declines

Aug 10, 2026 -

Unexpected rise in US propane inventories

Aug 3, 2026 -

Distillate prices becoming brutal

Jul 27, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.

{kind=link}

{kind=link}