No price relief despite good inventory report

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, addresses rising propane prices.

The short-term pricing strategies we presented in the past two Trader’s Corners remain in play as propane prices continue to rise. On Friday, Sept. 24, Mont Belvieu LST propane closed at 134 cents and Conway at 134.5 cents. Those two pricing points closed out September at 145 cents and 144 cents, respectively. The opening price for October was 147.375 cents Mont Belvieu LST and 147 cents Conway.

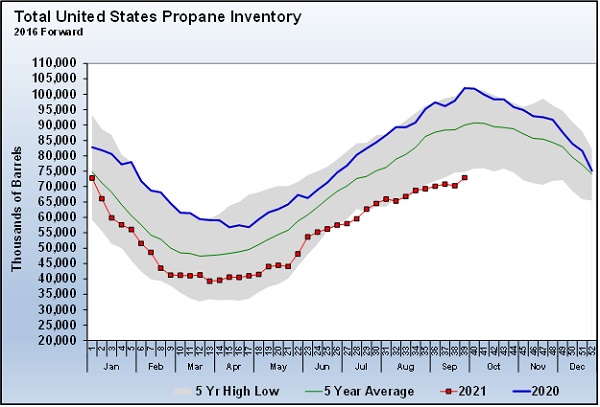

Chart 1: Cost Management Solutions

On Wednesday, Sept. 29, the U.S. Energy Information Administration (EIA) released its Weekly Petroleum Status Report for data collected on Sept. 24. The data was about as good as buyers could have hoped for at this point. U.S. propane inventory went up 2.642 million barrels. Industry analysts polled before the report showed an average expectation of just a 700,000-barrel build. Over the past five years, week 39 of the year had averaged an inventory increase of 1.516 million barrels.

The build beat expectations and the five-year average by good margins. However, as Chart 1 shows, inventory is still setting a five-year low for this time of year. And as you can see from last year and the five-year average, the inventory build period is running out. At 72.921 million barrels, inventory is 29.038 million barrels, or 28.5 percent, below last year and 19 percent below the five-year average for week 39 of the year.

The headline inventory build was certainly welcome even though the inventory shortfall remains significant and price supportive. Beyond the inventory build was a very welcome number on U.S. propane production.

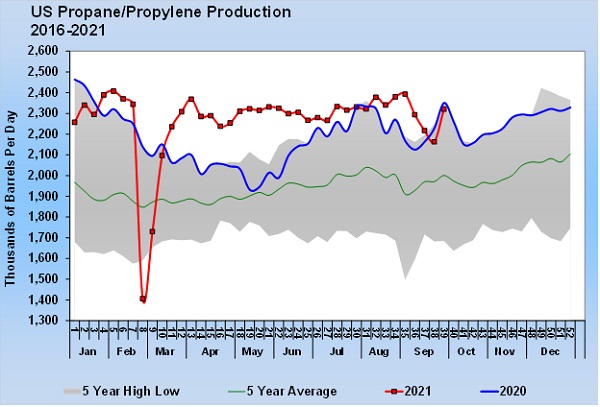

Chart 2: Cost Management Solutions

U.S. propane production jumped 158,000 barrels per day (bpd) to 2.321 million bpd. Over the previous four weeks, a disturbing downtrend had developed for production. During that period, propane production had dropped 217,000 bpd. Though this week’s increase in production didn’t recover all of the previous four-week decline, it broke the very troubling downtrend.

We do note production tends to dip around this time of year. Perhaps it is refinery maintenance, tropical storms or fractionator maintenance – or a combination of the three that could take place this time of year. Still, with inventory already low, declining production seemed to take on added significance this year.

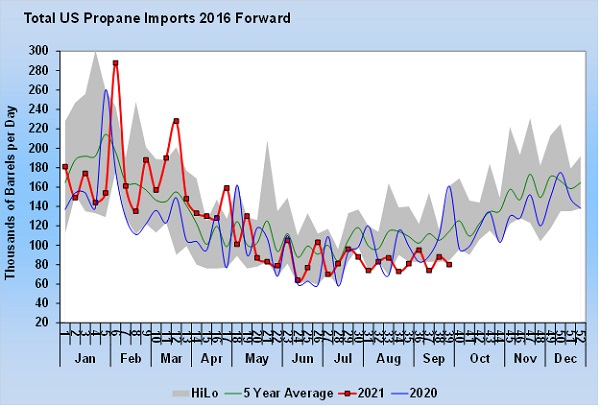

Obviously, the U.S. needs all of the domestic production it can get at this point. Imports from Canada were strong at the first of the year but slowed considerably over the summer.

In the first quarter of the year, the U.S. averaged 31,000 bpd more in imports from Canada than it did during the first quarter of 2020. However, since then, imports from Canada have averaged 3,000 bpd less than last year. The year-over-year import gain is now just averaging 8,000 bpd and trending in the wrong direction.

Chart 3: Cost Management Solutions

At one point last week, just after the EIA report and during a dive in crude’s price, propane at all three Mont Belvieu pricing points and Conway dipped to around 139 cents. But since then, propane prices have resumed their uptrend. Markets turned on a report that China’s energy minister told energy companies to acquire the supply they needed at all costs. This came as the country dealt with energy shortages that caused blackouts. Even before this report, Goldman Sachs had upped its crude price forecast by $10 per barrel, calling for $90 Brent crude by the end of the year.

There is a severe shortage of natural gas globally. U.S. natural gas prices are just under $6 per mmBtu, the highest since 2014. By comparison, natural gas in Europe has jumped to $32 per mmBtu and $30 per mmBtu in Asia. The high price has caused many users to look for alternative sources of energy. Propane will likely be among them.

We can hope that these bullish propane pricing conditions will resolve themselves this winter. However, as buyers hope, they probably need to take steps to prepare for the worst.

The short-term pricing strategies we presented over the previous two weeks won’t help consumers avoid the full impact of the price increases this winter. But, as we suggested, it helps retailers combat their tendency to delay price increases, especially in rapidly rising markets, that cause their margins to contract.

Also, remember our discussions on swaps. If a retailer decides to take longer-term price protection, say for the remainder of winter, rather than the short-term, one-month-at-a-time strategy, he can always shut down the positions by selling swaps for the same months and volumes.

Let’s say a retailer buys swaps to cover October through March of 100,000 gallons per month. Then, toward the end of December, the fundamental picture changes, and he believes prices could start falling again. He could then sell January through March swaps of 100,000 gallons per month. The two positions will offset themselves, locking in whatever price gain or price loss that had occurred to that point on the January to March positions.

The retailer would no longer have protection from higher prices in this event but would avoid watching position gains evaporate and be in the position to lower retail prices should prices indeed go lower.

Call Cost Management Solutions today for more information about how client services can enhance your business at 888-441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Unexpected rise in US propane inventories

Aug 3, 2026 -

Distillate prices becoming brutal

Jul 27, 2026 -

Aaron Huizenga on the power of self-awareness

Jul 19, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.