What back-to-back builds mean for propane inventories

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, examines inventory builds this year and what that might mean for the low inventory position.

After four weeks of trying to provide information and context for the impacts on energy resulting from Russia’s invasion of Ukraine, we are going to refocus our attention to the state of U.S. propane. Specifically in this Trader’s Corner, we are going to look at the status of U.S. propane inventories.

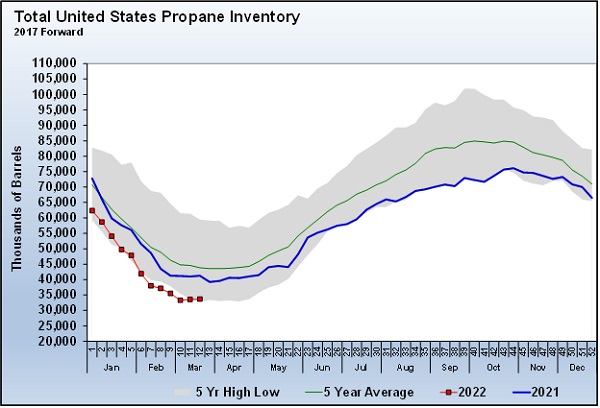

Chart 1: Cost Management Solutions

We wanted to take this measure of inventories after two weeks of small inventory builds. Historically, the low inventory positions for the year have been posted between the 10th and 17th weeks of the year, or about the first week of March through the last week of April. Just because there has been a couple of inventory builds already doesn’t mean the low inventory position has necessarily been printed for this year. There have been times when draws resumed for a few more weeks after late-season builds before the uninterrupted summer inventory build period got underway in earnest.

Still, there is hope that with inventories relatively low, the inventory builds will continue. The current high prices should be hurting demand, which should help end inventory drawdowns. And of course, the key reason for optimism on the inventory front is the near end of the heating season.

For the week ending March 25, the Energy Information Administration (EIA) reported U.S. propane inventory at 33.709 million barrels, up 145,000 barrels per day (bpd) from the previous week. The week prior, the EIA reported an inventory build of 256,000 barrels. These two builds put inventories just slightly above the five-year low for this time of year.

If these builds do indeed mark the end of the inventory drawdown, the low inventory position for this year would stand at 33.308 million barrels. It would be an early end to the drawdown period. However, that inventory would rank third lowest over the past 10 years. The low inventory in 2014 was 25.658 million barrels, and in 2018 it was 32.671 million barrels. In the other seven years of the last 10-year period, the low inventory position has ranged from 36.702 million barrels to 56.780 million barrels. The average low inventory position over the last 10 years has been 42.346 million barrels, making the current low for this year 9.128 million barrels, 21.51 percent, below average.

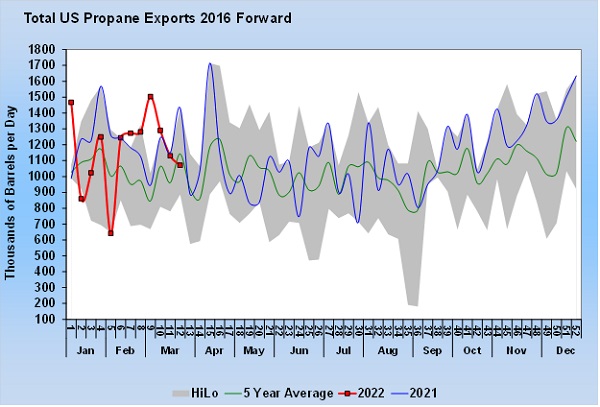

Chart 2: Cost Management Solutions

That kind of inventory deficit is price supportive for propane. Propane buyers are not only going to want to see the inventory builds that began two weeks ago continue uninterrupted, but they are also going to want to see above-average builds to eliminate the deficit, hopefully resulting in lower prices over the summer. What could work against above-average inventory builds would be strong propane exports throughout the summer.

So far this year, propane exports have averaged 10,000 bpd less than they did over the same period last year.

What concerns us, however, is the major push that is going to be coming from Europe to offset as much energy sourced from Russia as possible. That has the potential to increase demand for propane. The flexibility of propane gives it excellent potential to be chosen to offset Russian natural gas supplies. As we have mentioned, propane can be blended with methane in natural gas distribution systems to increase Btus. With natural gas prices in Europe 5.17 times higher than natural gas in the U.S., there is a lot of reason to consider propane. That makes natural gas in Europe the equivalent of $2.65 propane. That provides a lot of incentive to either blend propane with methane or flat out replace methane with propane.

Perhaps propane will fly under the radar of European buyers/consumers, and increases in crude refining and natural gas production in the U.S. will help propane production and erase the current inventory deficit before next winter. This is going to be a particularly difficult summer to navigate in terms of lining up supply and price protection for next winter. There is a lot that could happen geopolitically that could send energy prices sharply higher or lower in 2022. This will require buyers to build flexibility into their propane supply plans. Further, any speculative position needs to be monitored closely with an exit plan should market conditions significantly change.

Call Cost Management Solutions today for more information about how client services can enhance your business at 888-441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Unexpected rise in US propane inventories

Aug 3, 2026 -

Distillate prices becoming brutal

Jul 27, 2026 -

Aaron Huizenga on the power of self-awareness

Jul 19, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.