Natural gas production slowing

Join Cost Management Solutions for a free 30-minute Virtual Hedging webinar on Wednesday, May 29 at 10 a.m. CT. Register here.

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, examines why natural gas production is slowing and how it will impact propane.

Catch up on last week’s Trader’s Corner here: Propane production recovers to near-record levels

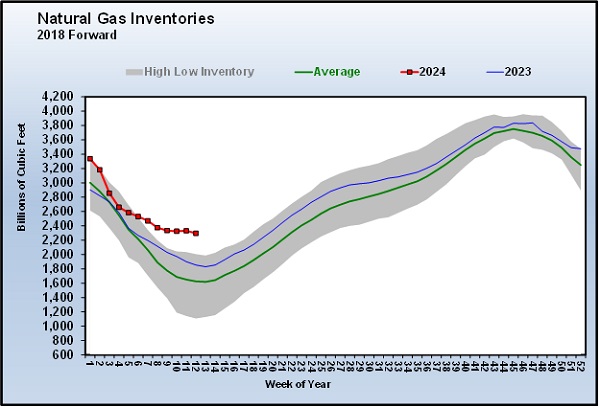

Chart 1: Natural Gas Inventories (2018 Forward)

U.S. natural gas prices have recently fallen to a 3.5-year low, causing some natural gas producers to shut in production or to delay completing newly drilled wells. The collapse in natural gas prices to under $2 per MMBtu has natural gas valued at the equivalent of 17 cents per gallon of propane. That is up from around 11 cents per Btu equivalent of propane a few weeks ago.

Natural gas prices have dropped about 23 percent since the first of the year. On an inflation-adjusted basis, natural gas prices are at 30-year lows. Some producers are responding. Chesapeake Energy and EQT have curtailed production, which has helped push natural gas prices off their lows. The cutbacks caused natural gas output to drop nearly 7 percent last month.

March natural gas production was around 98 billion cu. ft. per day (Bcf/d) from just over 104 Bcf/d in February. The production cuts caused natural gas prices to rise from $1.511 per MMBtu to $1.8350 per MMBtu.

So far, the production cuts have done little to impact a significant overhang in natural gas inventories. We did see a slight decrease in inventory last week, but overall they are setting significantly higher five-year highs for this time of year. In fact, they are about 41 percent higher than normal for this time of year. Producers have their work cut out for them to get inventories back in line. Obviously, the very weak winter demand was a huge factor in inventories surging.

If mild weather hasn’t been enough, the nation’s largest liquefied natural gas (LNG) export facility has reduced capacity due to maintenance work. In addition, more renewables used for electricity generation could cut into the demand for natural gas for that purpose.

The relationship between natural gas and propane is a two-edged sword. Natural gas is a competing energy source with propane. But, more importantly, propane supply is directly related to natural gas production. Natural gas has become so plentiful in the U.S. that propane has not been a competitive Btu with it for some time. Even when natural gas prices were much higher, propane struggled to compete. Part of the reason is that if natural gas supplies got too low, propane would be rejected at the natural gas processing plants. This would tighten up propane supply and push propane’s price higher.

Normally, at natural gas processing plants, as much of the propane as possible is removed from the methane that is sold to the natural gas companies. But if natural gas supplies get tight and prices go too high, some of the propane will be left with the methane. This is known as propane rejection. There are contractual limits as to how much propane can be rejected, but the practice has always ensured that propane prices could not go below natural gas prices. However, the need to reject propane has not been present for a very long time, given that natural gas prices are so much lower than crude/propane prices. Propane is valued in relation to crude, not natural gas.

The abundance of natural gas production in the U.S. has caused propane supplies to surge as well. The U.S. makes about 1.5 million barrels per day of propane more than it can consume. This abundance almost assures there will not be an overall supply shortage in the U.S. That doesn’t mean there can’t be local market shortages. Those are mostly related to logistical issues and not because of a shortage of supply nationwide.

Despite the recent drop in production, there are reasons to believe the cuts in natural gas output are unlikely to go deep enough to hurt propane supplies too much. First, the U.S. will double its LNG export capacity in the next few years from about 13 Bcf/d to around 26 Bcf/d. The U.S. is already the world’s largest LNG exporter, which increases natural gas demand and thus propane supply. The U.S. exported an average of 11.9 Bcf/d last year, but it was up to 13.6 Bcf/d in December. Most U.S. LNG exports are going to Europe as the region tries to reduce its dependence on Russia. Between 2021 and 2022, U.S. LNG exports to Europe were up 119 percent. They tacked on another 7 percent increase this year. The trend should continue as more capacity comes online.

Another area that will increase natural gas production, and thus propane production, is continued drilling for crude. At this point, crude production is expected to increase. When crude wells are drilled, associated natural gas and natural gas liquids are produced from those wells. In recent years, much of the growth in natural gas and NGL production has come associated with crude drilling and production. That should continue.

This increases the challenge of Chesapeake Energy and other large natural gas producers to check production by just shutting in natural gas wells. It should be interesting to see just how much of a hit to production and revenue they are willing to endure to support prices.

All charts courtesy of Cost Management Solutions

Call Cost Management Solutions today for more information about how client services can enhance your business at 888-441-3338 or drop us an email at info@propanecost.com.

Related content:

You May Also Like

-

Crude still not out of the woods

Jun 29, 2026 -

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.