Propane traders aim for retail operation stability

Photo: iStock.com/ismagilov

If your vision of a propane trading office is one of people yelling, papers flying, money falling from the sky, well, that’s not exactly the picture The Redwood Group paints inside its headquarters in Mission, Kansas.

“I think that’s the furthest thing from the truth,” says Brandon Hanna, a risk manager for the group. “People come in the office and say it’s not what they expected.”

In fact, the energy desk at Redwood is composed of just two employees – Hanna, who oversees the company’s trading book and tracks the daily market, and Pete Rieg, who focuses on customer relationships and deal flow. The two work together to help their propane retailer clients meet their supply buying and hedging needs. Redwood’s other 17 employees, including back-office support, focus on other commodity markets, such as ethanol, biofuels, specialty food products and grains desks.

“We interact with our customers daily, weekly or every two or three months,” Hanna says. “Whatever they need to protect their businesses.”

Hanna and Rieg founded the natural gas liquids (NGL) desk at Redwood in early 2014, but they are hardly new to the propane industry. Hanna, a Kansas City, Missouri, native, formerly ran trading books for Ferrellgas and Inergy (now Crestwood). Rieg formerly ran the pricing/hedging desk for Inergy, in addition to stints at Williams Cos. on their gas, chemical and power desks.

“Every company typically has one central location where price risk is managed,” Hanna says.

A company could have hundreds of branch locations that are selling fixed-price products to their propane customers. It wouldn’t want each branch manager trying to watch the market. Few propane retailers actually try to “trade” the market, Hanna says. They are focused on locking in margin based on sales to their customers and not speculating on the market.

“I think [propane retailers] are fascinated by the concept of trading, but at the end of the day, trading comes down to knowing the supply and demand of the entire market, and I think retailers have a great handle on their physical supply and demand in their localized region and not the overall propane market,” Hanna says.

Reading the markets

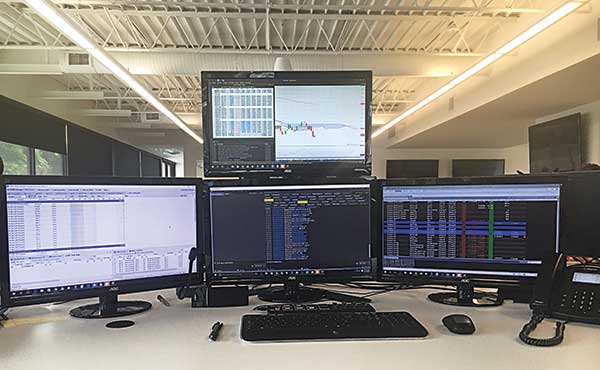

This photo showcases The Redwood Group’s trade floor in Mission, Kansas. Photo courtesy of The Redwood Group

Retailers might lose their handle on the market a bit when more global factors, such as propane imports and exports, come into play.

Traders like Redwood track LP gas vessels around the world, as well as chemical feedstock consumption for propane, historical propane demand by market sector and other factors like refinery outages to help determine a daily supply-and-demand balance, which goes into forecasting the Energy Information Administration’s weekly propane inventory number. These factors ultimately drive propane pricing and traders’ decisions.

“Our team devotes a significant amount of time to understanding the propane markets,” says Wes Osbourn, managing director of global commodities at Martin Energy Trading in Houston. “It is one of the fastest-changing markets in the energy space due to increased cracking capacity and increased export capacity. It has become increasingly important to understand all of the drivers around the world, and not just here in the U.S., to be an effective propane trader.”

Factors that can move the market are important for retailers to understand, as well. Each morning, Redwood sends a short summary to its customers detailing overnight events and economic reports. Retailers also receive pricing information that helps them establish pricing for their propane-buying customers.

“I can adjust my selling price to the customer based on daily information I get from Redwood,” says the CFO of a 200-employee mid-Atlantic propane retailer who runs his company’s consumer hedge program. “I’m adjusting my price to the customer based on the current cost from Redwood on propane hedges. The customer makes a decision to commit to [us], and we’ll turn around and lock in some gallons with Redwood.”

But while Redwood communicates with its customers about the propane market, it won’t advise them on what to do, Hanna says. It’s a liquidity provider that shares information so the customer can ultimately make its own decisions.

“We don’t say the market’s going higher or lower. We aren’t even big advocates that the customer should care if the market goes higher or lower,” Hanna says. “If you’ve reached your desired propane margin on this sale, hedge it, lock it in and move on to the next one. I guarantee you will make more money over the long run hedging your sales than trying to time purchases in the market.”

Reviewing the process

Propane retailers know the process: A customer completes a propane sale through a retailer’s program, and the retailer seeks to protect the customer’s price and the retail margin through a hedging program. That’s where traders – Hanna estimates 50 to 60 companies are trading daily – enter the picture.

The retailer will work with a trader directly or through a propane industry consultant to buy supply as part of a financial transaction. No physical gallons actually change hands, though.

“This is the hardest thing for most people in our industry to understand,” says Mark Rachal of propane industry consultant Cost Management Solutions (CMS), which works with traders on retailers’ behalf. “The physical side of the business is operating out there just like it always has. The financial side is totally independent of that.”

Hanna provides an example of “XYZ Propane” needing to hedge 100,000 gallons of propane. The retailer will get a skew of its volume – or a breakdown of how much it’s buying per month based on demand. Redwood will check the skew against its price curve to determine a price offering for the retailer.

“They’re buying this because they’ve sold a fixed price to their customers and they need to achieve margin,” Hanna says. “They’re coming in to lock in that margin so they can hit budget on a fixed-price program.”

On some days, Redwood might hear from 12 retailers, each requesting 100,000 gallons; on other days, it might hear from only one retailer. And the requested volumes vary. Redwood’s smallest deal has been 4,700 gallons spread over 16 months; its largest about 7 million gallons.

“We can go big or small; it doesn’t matter,” Hanna says. “You come to us with what you need and we’ll help you.”

Once a trader has assumed enough risk by combining its propane retailer deals, it will hit the market and go hedge its own risk. Redwood trades on the Chicago Mercantile Exchange and the Intercontinental Exchange. Hanna says the minimum contract size that can clear on either exchange is 10,000 barrels, or 420,000 gallons.

“Whenever we get enough to buy something in the market, we’ll do that to lay off our own risk,” Hanna says. “We don’t always buy exactly the months that the customer buys from us. That’s my job – a little more finesse [is involved]. We try to identify opportunities through trading the spreads between months and quarters.”

Balancing act

Computer monitors are positioned on risk manager Brandon Hanna’s desk. Photo courtesy of Brandon Hanna

Rachal says trading involves a lot of focus – so much so, in fact, that most of the communication between CMS and propane traders happens over instant messaging. They exchange price data, and an agreement is met with a simple “Done” message.

“Now our retailer has a firm price and he can give that firm price to the customer, and that business owner knows what propane will cost for the next 12 months,” Rachal says. “All of this really works together. To take unknowns and turn them into knowns, that’s very powerful for the propane retailer – when he has a known price in his marketplace without taking undue risk.”

Hanna spends most of his day monitoring the broker market – where he will execute his trades. He receives instant messages from about 10 people who are focused on potential propane deals.

He’s also well aware of price data. One of his screens produces the front few months, and maybe a quarter or two out, of all NGL prices. But he knows propane’s price from the current month into 2020, as he keeps an eye on the Mont Belvieu and Conway trading hubs.

“They’re seeing a batch of this, that or the other that needs to move around,” Rachal explains of commodity trading. “Traders are also playing all kinds of things in the background. They’re playing spreads against various things; they’re playing one product against another product. In its simplest form, these guys have relationships on either side of the equation, and they’re in the middle making transactions.”

To ensure timely communication in trading, parties will use an instant messaging system; a trading turret, which allows parties to communicate instantly by pushing a button and speaking into a microphone; or some other type of electronic trading platform. Telephone and email are also used.

“We have an open trade floor with no walls,” Osbourn says. “The typical trader has eight monitors and a turret, which acts as a speaker phone to talk to brokers.”

Before the concept of propane trading grew in sophistication, a retailer might buy a load of product from a supplier, mark up the price, sell it to a customer and call it a day. In doing so, the retailer would subject the company to market changes that ultimately would impact its bottom line.

“A buy-and-markup mentality is all we had as an industry,” Rachal says. “It put us at a real disadvantage to other energy sources.”

Now, having the ability to enter into a financial program protects retailers from those price fluctuations and helps level the playing field against energy competition.

“In 2008 when the market crashed, people were sitting on product that was way high compared to the market, and you’re exposed. That forever changed how we do business,” the CFO of the mid-Atlantic retailer says. “[Today] I will wait until I have a customer commitment, and then I’ll match it up with a hedge commitment.”

You May Also Like

About the Author: Brian Richesson

Brian Richesson is the editor in chief of LP Gas Magazine. Contact him at brichesson@northcoastmedia.net or 216-706-3748.

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.