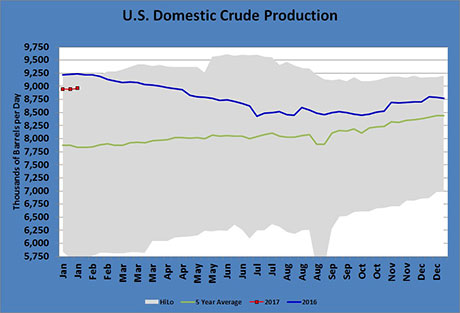

US crude production offsets other production cuts

In recent weeks, there has been a separation between propane and crude pricing. Propane prices have been stronger, with solid fundamental support in the form of above-average draws on propane inventory, causing propane’s price to move up faster than crude.

We often describe propane’s price as a rocket attached to the wing of a fighter jet. Occasionally, the rocket is fired off and sets its own direction, but most of the time the rocket stays attached to the wing of the fighter jet and goes where it goes. In our analogy, crude is the fighter jet. For propane retailers, if the price of the commodity they are buying is tied to another commodity, then it’s best to know where that other commodity is heading.

There has certainly been a lot going on in the world of crude. In late November, 24 producing/exporting nations agreed to curb production to try and eliminate an imbalance between crude supply and demand that caused West Texas Intermediate’s (WTI) crude price to plummet to $26.21 in February 2016. That was the lowest crude price since 2002 and a far cry from the high of $145.29 hit in July 2008.

The 24 producers agreed to cut nearly 1.8 million barrels per day (bpd) from their output during the first six months of 2017. Producers began implementing those cuts this month. A meeting to monitor compliance with the pledged cuts was the weekend of Jan. 21. The conclusion by the Organization of the Petroleum Exporting Countries (OPEC) compliance team was that 1.5 million bpd of cuts had been made already and that total cuts would hit 1.7 million bpd before the end of the month. The level of compliance was much higher than most expected and the news was supportive for crude prices. OPEC is responsible for 1.2 million bpd of the production cuts. An independent industry report says that OPEC cut just 900,000 bpd from its production during January.

WTI crude reached its recent high of $54.09 on December 12, 2016, right after the producers announced how much crude they planned to take off the market. However, prices drifted lower at the start of 2017 as traders feared producers might not adhere to their pledged cuts. The news on the strong compliance with the agreement turned crude prices slightly last week, but there remains a struggle for crude to gain upward momentum.

Producers fear that U.S. crude production is simply going to offset the cuts they make, preventing crude from gaining upward momentum.

United States crude production increased 17,000 bpd last week. That put total U.S. production at 8.961 million bpd.

There has been much talk recently of U.S. production offsetting the 1.8 million bpd in cuts made by 24 crude exporting nations. U.S. production is up 533,000 bpd since the July low of 8.428 million bpd.

Production remains considerably short of the 9.61 million bpd recent high set in late May 2015. Since beginning its rebound, U.S. crude production has averaged gaining a little over 18,000 barrels per week. Assuming it has already offset about 500,000 bpd of other producers’ 1.8 million bpd in cuts, U.S. production would need to increase another 1.3 million barrels to negate the total impact of the other producers’ cuts.

At the current rate of growth in production, it would take another 70 weeks, or around a year and four months, for U.S. production to fully offset what other producers have committed to cut. However, the gains in production should increase with many drilling rigs going back to work.

Other producers have only agreed to curb production for the first six months of this year. By July, crude markets could be right back to where they were before the production cut agreement was implemented, meaning those nations will begin increasing production to curb higher-cost U.S. production. But as we saw last year, it can take a while before U.S. production stops growing, much less begins to decline.

The market has already established that crude prices are going to struggle to get out of the $50 to $60 range even with the production cut agreement active through June. Crude is likely to stay in that range over the next five months as long as producers continue to adhere to the agreement. However, unless global crude demand greatly increases during that period when other producers start fighting back against U.S. supply, crude prices could be pushed below the $50 mark until U.S. production begins to fall, perhaps months later.

Right now, the odds favor a neutral to even bearish trending crude market as we head into next winter. That means propane is likely to be dependent on its own fundamentals to rocket higher coming out of the summer inventory build period. We have seen this year that good domestic demand and high imports can ignite the rocket, but the good news is that the jet fighter is unlikely to gain a lot of altitude before the rocket is released. For propane retailers, this brings hope that the upside for prices might not get unbearable even if strong propane fundamental support is present next winter.

If we are wrong on crude and it is moving higher, and propane fundamentals are supportive again, the air could get unbearably thin. Having witnessed solid gains in propane’s value this year, retailers are likely going to feel compelled to protect themselves from higher prices next winter.

However, it is probably not going to be as simple as buying a pre-buy or swap and forgetting about it. If retailers take long-term positions, they are going to need to manage the potential for falling prices in the interim. That means taking short-term positions after the long-term positions are entered to pocket cash and build up a nest egg in case crude is flat to lower and winter is weak again.

Managing the risks to lower prices of long-term positions with short-term strategies can have the additional benefit of improving margins during the lower-volume summer months. In any case, taking an active role in managing long-term positions with interim short-term risk management tools and strategies can give retailers confidence they will be in a good financial and competitive position next winter no matter how prices are trending.

Call Cost Management Solutions today for more information about how Client Services can enhance your business at (888) 441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026 -

Iran peace deal’s impact on propane markets

Jun 15, 2026 -

How the US-Iran war draws on propane inventory

Jun 8, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.