Part II: Could the inventory trend change in 2023?

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, continues to review the change in propane inventory with the end of 2022.

Catch up on last week’s Trader’s Corner here: Could the inventory trend change in 2023?

Read the rest of this four-part series:

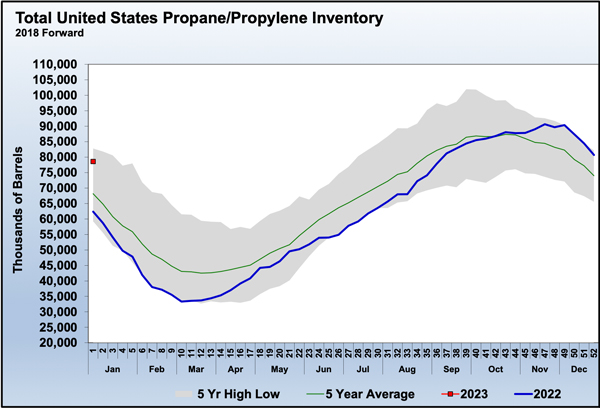

Chart 1: Cost Management Solutions Click to expand.

In last week’s Trader’s Corner, we looked at the flip in propane inventory over the course of 2022 – from setting five-year lows to setting five-year highs. Then we began a look at what could change that could flip the inventory trend in the other direction.

Chart 1 was updated with the latest data, which shows the starting position after the first week of this year. The blue line is last year’s inventory trend, showing how inventory started the year near five-year lows and, in some weeks, setting new five-year-low marks. Even in mid-summer, inventory was at five-year lows.

As late as mid-August 2022, the inventory position was very concerning with winter just ahead. But, at that point, the inventory situation began to turn in favor of buyers. At the core of the change was very high propane production driven by record-high natural gas production and improving crude production (which yields associated natural gas production). But, there were other factors that all seemed to come together at the same time to change the inventory trend and the tone of the market. Propane exports that had been increasing all year began to level off. Domestic propane demand that had been off all year continued to be lethargic. Crop drying was a nonevent, and beginning winter temperatures were mild.

Propane prices reflected the concern.

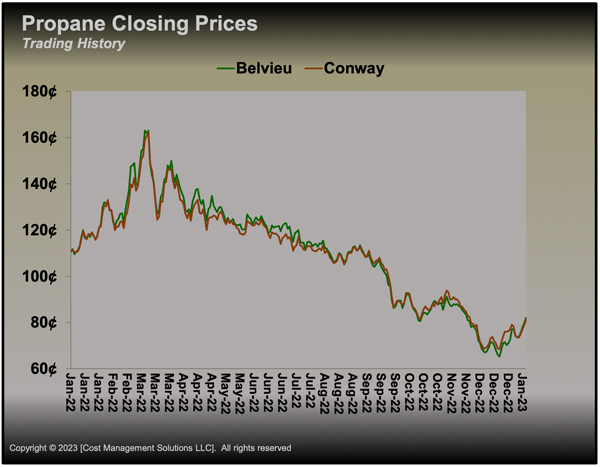

Chart 2: Cost Management Solutions Click to expand.

The low inventory position at the start of 2022 had prices at painfully high levels. As winter ended, prices fell through the summer. We feared the slow drift lower was lulling buyers into a false sense of security. In August, with inventory at five-year lows, we reminded everyone that we thought a propane price of a dollar would be a good buy. By mid-September, prices broke below that mark.

Even then, we were suggesting it best not to be looking a gift horse in the mouth. In other words, we liked the prices available for winter price protection. But it was at that point that the propane inventory trend parted from anything normal or typical. During a relative short period between mid-August to the end of November, propane inventory went from setting a five-year low to setting a five-year high with all the factors we mentioned above having a part to play. By mid-December, propane prices were nearly a dollar below their highs in early March. At the low point, Mont Belvieu propane hit 65.25 cents and Conway tumbled to 68.5 cents. That was 30 to 35 cents below what we thought would be a great price. It was very hard to imagine given the five-year low inventory position in mid-August.

We had this remarkable inventory build during winter. So, we can’t help but to wonder what could flip the inventory trend in a much less pleasant way from the perspective of propane buyers and consumers. Last week, we showed how refiners focused more on fuel-use propane at the expense of propylene production last year. That was a contributing factor in the increased propane supply. We showed that if refiners moved back to favoring propylene output it could drop as much as 3.65 million barrels from propane supply, which would represent an amount equal to 24 percent of the inventory gain over the course of last year.

Chart 3: Cost Management Solutions Click to expand.

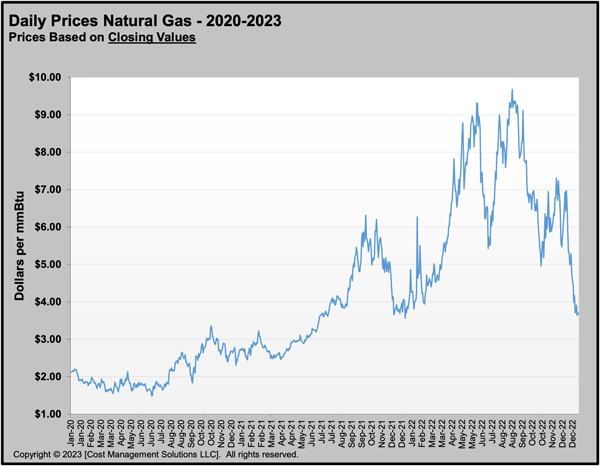

The potential biggest threat to propane supply would come from a change in natural gas production. Nearly 88 percent of propane supply comes from natural gas processing, with the balance coming from refining. The natural gas can come from wells that are drilled specifically for lighter hydrocarbons. The production includes methane, ethane, propane, butanes and natural gasoline. Then, there is natural gas that is produced in association with crude wells. Producers drill for the heavier hydrocarbons, but the wells also yield some volume of lighter hydrocarbons at the same time. In fact, for years, while natural gas (methane) prices collapsed, most of the new natural gas production was coming as associated natural gas. That is the key reason natural gas prices stayed suppressed for so long. We really didn’t need the natural gas, but it was being produced anyway as more and more crude wells were drilled.

By mid-2020, natural gas (methane) was valued at less than $1.50 per MMBtu. But less production of crude after the pandemic crushed energy demand, lowered associated natural gas production and began to lift methane prices. Then the war in Ukraine occurred, and U.S. natural gas prices rallied to a high not seen since before 2010. Methane hit a high of $9.68 per MMBtu, which was a tenth of what it reached in Europe, at $99.71 per MMBtu. Now, methane’s price is back to $3.695 per MMBtu.

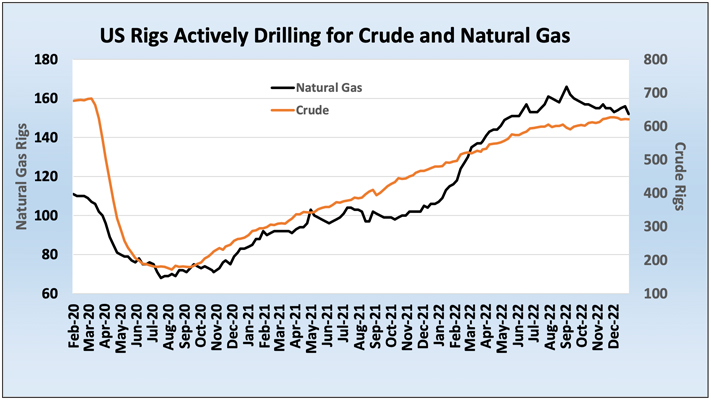

Chart 4: Cost Management Solutions Click to expand.

The lower price for crude and natural gas is impacting drilling activity already. Most of last year, the number of rigs actively drilling for natural gas (light hydrocarbons) was rising. But recently, there has been a slight tapering of those rigs. Last week, four rigs were idled. There are still 45 more than this time last year, but the growth has slowed for now.

On the crude drilling front, the number has been increasing since the collapse of activity after the pandemic. The active rig count never reached what it was before the pandemic, and it looks like it may have plateaued as well.

Even though active rigs may be plateaued, the current number of rigs would likely keep propane supply robust as it should yield plenty of natural gas and associated natural gas production. But if the supply side plateaus and the demand side begins to recover, there could be a tightening of supply and slower builds in inventory. All last year, the growth in propane supply kept largely offsetting robust exports. With the drop in domestic demand, the supply-demand balance was never strained once the winter of 2021-22 was over, allowing inventory to build. But for now, based on the recent trend in drilling activity, the supply-side growth could be slower in 2023.

Read the rest of this four-part series:

Call Cost Management Solutions today for more information about how client services can enhance your business at 888-441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Distillate prices becoming brutal

Jul 27, 2026 -

Aaron Huizenga on the power of self-awareness

Jul 19, 2026 -

Geopolitics send crude and propane prices higher

Jul 13, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.