Part IV: How US energy has changed since Russia invaded Ukraine

Trader’s Corner, a weekly partnership with Cost Management Solutions, analyzes propane supply and pricing trends. This week, Mark Rachal, director of research and publications, continues his examination of why U.S. energy sources have changed since Russia invaded Ukraine and puts the focus on U.S. crude imports and exports.

It has been two months since Russia invaded Ukraine. In response to the invasion, the U.S. and its allies, especially those in Europe that were dependent on Russia for energy, have been saying they will reduce Russian energy imports as punishment for its actions. The U.S. has pledged to help Europe with its energy needs in an effort to supplant Russian energy. The purpose of this series has been to look at key U.S. data to see if the U.S. energy market is indeed responding in a way that helps the U.S. and its allies wean themselves off of Russian energy supplies. Frankly, the findings to this point have been very disappointing. We have covered refinery throughput, refinery capacity and utilization rate, crude inventory (both commercial and the Strategic Petroleum Reserve or SPR) and crude production.

Refinery throughput has increased, but not enough to offset the refined fuels that the U.S. was getting from Russia before the U.S. government put an embargo on those imports. U.S. refining capacity has been trending lower, and that has not changed. Refinery utilization is up slightly since the invasion of Ukraine by Russia, but it is as much a reflection of lost capacity as increased utilization. U.S. crude inventory is not in a healthy position. Commercial stocks are setting five-year lows and not building as they usually do before the summer driving season. Inventory in the SPR has been coming down at an alarming rate over the past two years, and that trend will continue over the next six months as the government makes 180 million barrels available to the commercial market. U.S. commercial inventory did jump by more than 8 million barrels last week, but it was said to be just a reflection of the inventory coming out of the SPR into commercial stocks.

Increases in U.S. crude production are necessary to drive most all of the factors we are looking at in a positive direction. However, crude production is struggling to recover from drops that occurred during the pandemic. U.S. production was stuck at 11.6 million barrels per day (bpd) during a seven-week stretch in February and March. Production finally started going up at the end of March, reaching 11.9 million bpd, where it plateaued. The Energy Information Administration estimated production at just 11.8 million bpd for the week ending May 6. It was a disappointing drop.

This week, we are going to focus on U.S. crude imports and exports. In the first step, the U.S. should be trying to reduce its crude imports so that more of what is coming here can go to Europe. Once production has increased enough to offset imports and cover additional refinery throughput (should it occur), then we should see more U.S. crude exports.

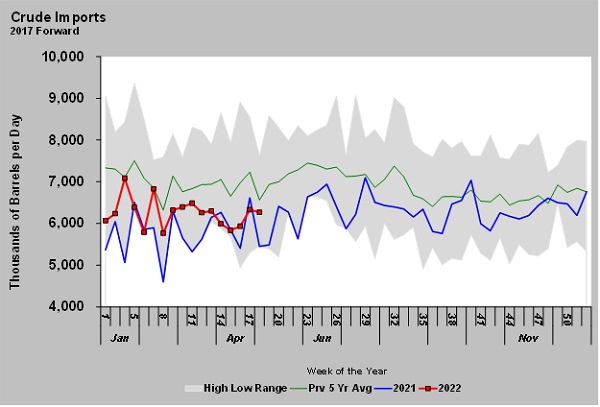

Prior to the pandemic, the U.S. was reducing its crude imports as it steadily increased its production to a record 13.1 million bpd. Crude imports averaged 7.849 million bpd in 2018 but had dropped to 5.875 million bpd by 2020. As we came out of the pandemic, the trend reversed to increasing imports as U.S. production remained well below peak production. In 2021, the U.S. imported 6.139 million bpd. So far this year, the import rate has been 6.277 million bpd.

During the first two months of the year, prior to Russia’s invasion of Ukraine, the U.S. imported 6.359 million bpd of crude. Since the invasion, the U.S. has imported 6.201 million bpd of crude. That is a drop of 158,000 bpd. Keep in mind, the U.S. was importing 199,000 bpd of crude from Russia before the government put an embargo on those imports in March. That means the U.S. has increased imports of crude from other sources by 41,000 bpd to partially offset the lost Russian imports. Theoretically, 158,000 bpd of crude has been made available to other consuming nations such as those in Europe.

Chart: Cost Management Solutions

U.S. production averaged 11.613 million bpd during the two months before the invasion and has averaged 11.760 million bpd since. That is an increase of 148,000 bpd. That means our own production increase has not even offset the decrease in imports. Further, our refinery throughput averaged 15.363 million bpd in the first two months of the year prior to Russia’s invasion. It has averaged 15.714 million bpd since. That is increased demand on crude of 351,000 bpd. Imports are down 158,000 bpd, refinery throughput is up 351,000 bpd and production is up only 148,000 bpd. That yields a 361,000-bpd draw on U.S. crude inventory. Obviously, under those circumstances we should not expect the U.S. would be increasing its crude exports.

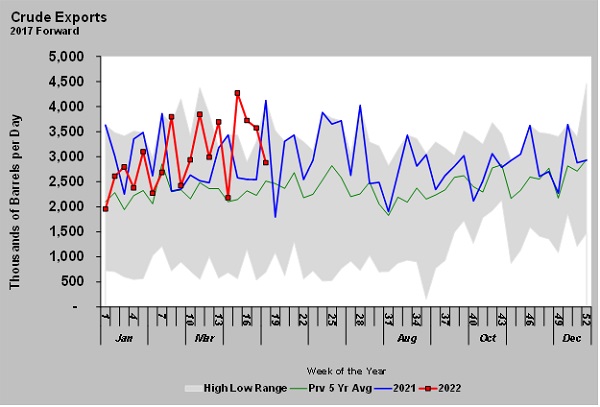

Yet that is not the case. Prior to the invasion, the U.S. exported an average of 2.668 million bpd and averaged exports of 3.343 million bpd since. That is an increase in crude exports of 675,000 bpd. Combined with the net inventory demand from our domestic operations, the U.S has averaged a draw of 1.036 million bpd on inventory since the Russian invasion began.

Chart: Cost Management Solutions

The government is releasing an average of a million bpd from the SPR. Obviously, those barrels are augmenting our own supplies in an effort to overcome our production deficit as well as help Europe. This should be incredibly alarming to everyone. Our crude supply system is operating on borrowed barrels, and there is nothing in the data that suggests we can sustain it once the SPR release has concluded. We have not even replaced, through increased crude production or refinery throughput, the crude and refined fuels that have been lost from Russia.

A key assumption of Europe weaning from dependency on Russia energy would be increased supply from other producing countries of which the U.S. should be a predominant player. There is no indication that either the government or industry has any urgency to sustain supply once the crude from the SPR has been used. In fact, we would say the opposite is occurring. Comments from industry executives are that they will continue to maintain capital discipline and do not have plans to increase production to the levels that would be required to significantly help offset Russian energy production. The government, just last week, restricted drilling more on federal lands in Alaska and the Gulf of Mexico, historically key production areas that already have infrastructure in place to deal with increases in production. There has not been one notable initiative by the government to encourage any additional hydrocarbon production. Europe is not announcing any initiatives to increase its hydrocarbon production and has simply looked for other import sources. If what is going on in the U.S. is any indication, we would suggest they will be no closer to being less dependent on Russian crude in September than they are now.

What this all appears to indicate is that no one really believes that Russian crude and natural gas will ever stop flowing to markets. There may be some swapping around of where barrels and Btus are going, but there is not going to be any real effort from an energy perspective to punish Russia for its invasion of Ukraine. At least consumers must hope that is true. If there is an honest-to-goodness effort to cut off Russian energy from the world without a lot more effort to replace it, the sky will be the limit for crude and natural gas prices.

Read the rest of the series here:

Call Cost Management Solutions today for more information about how client services can enhance your business at 888-441-3338 or drop us an email at info@propanecost.com.

You May Also Like

-

Crude still not out of the woods

Jun 29, 2026 -

Aaron Huizenga on the leadership power of curiosity

Jun 27, 2026 -

The US, Iran and propane: A retrospective

Jun 22, 2026

Subscribe to LP Gas

If you enjoyed this article, subscribe to LP Gas to receive more articles just like it.